In almost any circumstance, the idea of precision bearings and products doesn’t exactly attract much excitement. Certainly, amid fears of a global recession and rising concerns that the Federal Reserve may inadvertently spark an economic downturn with its aggressive rate hikes, RBC Bearings (NYSE:RBC) probably won’t represent the first choice among market participants. However, investors ignore RBC stock to their own detriment.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

For one thing, RBC Bearings plays pivotal roles across several industries. True, as a stagehand and not the main attraction, RBC doesn’t necessarily command the spotlight. However, any successful Broadway show will feature several workers behind the scenes operating at full blast to ensure the production goes off without a hitch. Essentially, then, RBC represents the unsung hero of the economy.

On a scientific level, bearings help reduce friction between two moving elements, allowing for smoother rotation. In turn, this facilitation enables a reduction in the amount of energy consumption. Moreover, bearings help reduce wear and tear on critical components, enabling longer and more reliable service life for the products which said components undergird.

Specific to RBC stock, the underlying enterprise has been delivering the goods financially. For its most recent Fiscal Q1-2023 earnings report, RBC Bearings generated net sales of $354.1 million, representing a year-over-year lift of 126.7%. Also, organic net sales increased by 13.1%. On the bottom line, Q1 GAAP diluted earnings per share hit $1.09. On an adjusted basis, EPS hit $1.19.

“We are pleased to report, revenues were strong across the majority of our end markets in both the industrial and aerospace sectors,” said RBC chairman and CEO Dr. Michael J. Hartnett. “Matching this strength in demand was excellent execution at the plant level and exceptional margin performance. Our outlook for the balance of the fiscal year remains on this positive track.”

Broader Fundamentals Support RBC Stock

Of course, expectations call for corporate executives to frame discussions of their underlying businesses as positively as possible. However, RBC stock enjoys the benefit of outside fundamentals organically bolstering the enterprise.

While recession fears do dominate recent headlines, it’s also important to recognize that advanced economies don’t slow down merely because of expressed concerns. For instance, though the painful rise of prices for key consumer goods hurt sentiment, several sectors have so far enjoyed resilient demand. One of them is the travel industry.

After two years of pandemic-related lockdowns and mitigation efforts, consumer interest in real experiences skyrocketed. Therefore, when government agencies loosened restrictions on personal mobility, the concept of revenge travel took over. More planes flying the friendly skies drive increased demand for RBC stock.

Further, while the Fed’s interest rate hikes pose challenges and ambiguities about future economic conditions, the relative rise in strength of the U.S. dollar also provides benefits for the precision-engineered products industry. With American tourists taking advantage of the stronger greenback, international flights may increase. Naturally, this dynamic should aid RBC stock.

Finally, the political machinery in Washington smiles at the bearings specialist. With the passing of the Build Back Better bill, President Biden seeks to reinvigorate large sections of the U.S. economy. This, too, may be a net win for RBC stock.

Is RBC Bearings a Good Stock to Buy?

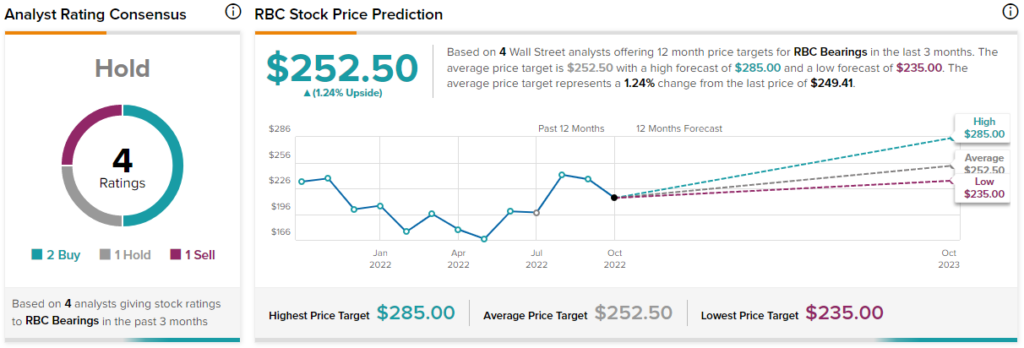

Turning to Wall Street, RBC stock has a Hold consensus rating based on two Buys, one Hold, and one Sell rating. The average RBC price target is $252.50, implying 1.2% upside potential.

Conclusion: Quantitative Metrics Show RBC’s Strengths

So far, RBC stock is firing on all cylinders. On a year-to-date basis, shares gained about 23%. Over the trailing half-year period, it’s up around 41%. Still, investors will want to check the quantitative data before making their final decision.

Here, the situation presents a mix of both positives and certain challenges. From the optimists’ angle, RBC’s three-year revenue growth rate (on a per-share basis) stands at 6.7%. In contrast, the median level for the industrial products sector is only 3.6%. This translates to RBC beating 61% of its competitors.

Also, over the same three-year period, the company’s growth rate based on free cash flow and book value hit 26.6% and 28.2%, respectively. Both figures rank better than at least 71% of the underlying industry. On the bottom line, RBC’s operating margin is 18%, ranked better than nearly 90% of the competition.

However, investors do pay a premium for this exciting business. Currently, shares trade at 119 times trailing-12-month earnings, which is very much on the high side of the industrial products sector. As well, the company could use some shoring up of its balance sheet, particularly with its lowly cash-to-debt ratio.

Nevertheless, because RBC commands relevance across the industries that literally move us, investors may be able to overlook certain flaws. If anything, RBC stock at least warrants serious consideration in your portfolio.