Continued market volatility could make it difficult for investors to pick the right stocks. It is better to ignore short-term disruptions and focus on secular trends that could drive long-term growth. One such trend is the shift to digital payments, which is expected to drive growth for fintech companies. Using TipRanks’ Stock Comparison Tool, we placed Upstart (NASDAQ:UPST), PayPal (NASDAQ:PYPL), and SoFi (NASDAQ:SOFI) against each other to find Wall Street’s most attractive fintech stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Upstart (NASDAQ:UPST)

Shares of artificial intelligence (AI)-based lending platform Upstart have surged since the company announced its first-quarter results earlier this month. Q1 revenue declined 67% to $103 million and the company slipped into an adjusted loss per share of $0.47 from EPS of $0.61 in the prior-year quarter. However, both metrics were better than analysts’ expectations.

But what really impressed investors was management’s commentary about the company securing multiple long-term funding agreements that are expected to deliver over $2 billion to the Upstart platform over the next 12 months. Rising interest rates have increased the risk of potential defaults and have also impacted the demand for consumer loans. However, Upstart’s outlook about the road ahead improved investor sentiment about the stock.

Moreover, last week the stock jumped after the company signed a deal to sell up to $4 billion of consumer installment loans to global investment management company Castlelake.

What is the Target Price for UPST?

Last week, Wedbush analyst David J. Chiaverini maintained a Sell rating on Upstart stock, stating that the economics of the new long-term funding partners remain unclear and credit quality continues to be weak.

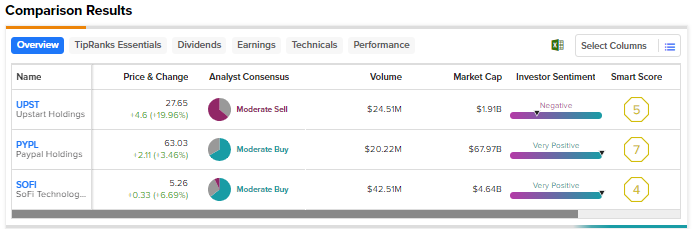

Wall Street has a Moderate Sell rating on Upstart based on one Buy, three Holds, and seven Sells. The average price target of $14.45 implies downside of 47.7% from current levels. Shares have rallied more than 109% year-to-date.

PayPal (NASDAQ:PYPL)

PayPal’s Q1 revenue and adjusted EPS grew over 8% and 33%, respectively, with both the top and bottom lines surpassing analysts’ estimates. The company raised its full-year earnings guidance to reflect the momentum seen in Q1 and cost-efficiency efforts.

However, the stock fell following the Q1 print, as the company cautioned that it expects the adjusted operating margin to expand by 100 basis points in 2023 compared to the previous estimate of 125 basis points. The rapid growth of Braintree, PayPal’s unbranded payment-processing business, which carries a lower margin than the branded business, was responsible for the revised margin guidance.

Macro pressures and rising competition have been impacting the company’s branded business. Nonetheless, several analysts remain optimistic about PayPal’s long-term prospects.

Is Paypal a Buy, Sell, or Hold?

Following the results, UBS analyst Rayna Kumar reiterated a Buy rating on PayPal but lowered his price target to $118 from $129 due to the tighter margin forecast.

Kumar thinks that although PayPal’s unbranded volume is creating a negative mix shift, it is driving share gains. Kumar believes that PayPal shares are undervalued, as he expects the fintech giant to deliver 20% EPS growth in 2023 and in the mid-teens thereafter. He views any pullback in the stock as an attractive buying opportunity.

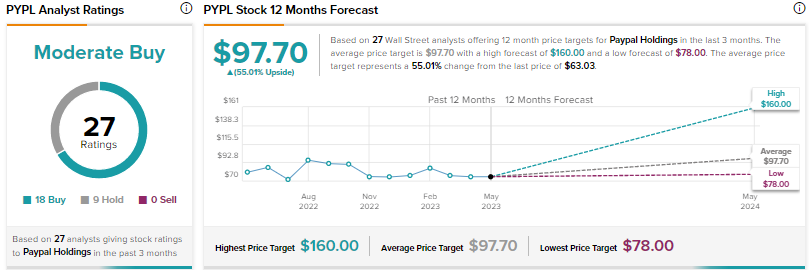

Overall, Wall Street is cautiously optimistic on PayPal stock, with a Moderate Buy consensus rating based on 18 Buys and nine Holds. The average price target of $97.70 suggests 55% upside potential. Shares have declined 11.5% since the start of the year.

SoFi Technologies (NASDAQ:SOFI)

Digital financial services company SoFi’s Q1 revenue grew 43% year-over-year to $472 million. The company narrowed its loss per share to $0.05 from $0.14 in the prior-year quarter. The company gained from continued demand for personal loans, which helped in offsetting the weakness in home loan originations due to rising interest rates and a fall in student loan origination volumes due to the moratorium on federal student loans.

Despite an improved outlook, the stock fell as investors were disappointed with the full-year guidance upgrade not being on par with the extent to which the company surpassed Q1 expectations.

Is SOFI Stock a Good Buy?

On May 15, Wedbush’s Chiaverini downgraded his rating on SoFi to Hold from Buy and slashed the price target to $2.5 from $5. The analyst cited several reasons, including concerns that the fintech’s capital levels could be overstated using fair value accounting and the company might look to raise capital this year to support its growth.

Note that SoFi’s loans are fair value marked every month on the basis of current company-specific and macro factors to reflect an expected sale price.

Last week, Piper Sandler analyst Kevin Barker also lowered the firm’s price target on SoFi Technologies to $6.50 from $8, noting that the company’s sizable adjusted EBITDA beat in Q1 was the result of larger-than-expected positive fair value marks on the personal and student loans.

Barker added that the fair value marks could create an incremental headwind to earnings due to premium amortization in the absence of sizable portfolio sales. That said, the analyst maintained his Buy rating on the stock, as he continues to see value in SoFi shares.

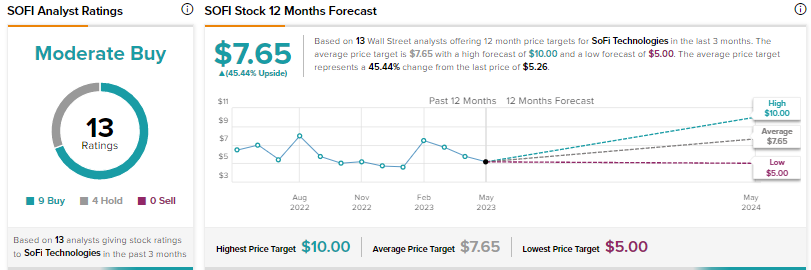

Wall Street’s Moderate Buy consensus rating on SOFI stock is based on nine Buys and four Holds. The average price target of $7.65 suggests 45.4% upside. Shares have risen 14% year-to-date.

Conclusion

While Wall Street analysts are cautiously optimistic on PayPal and SoFi, they are bearish on Upstart due to a lot of uncertainty and lack of clarity around its business. Analysts see higher upside in PayPal than the other two stocks, with the pullback in the shares offering an attractive buying opportunity to gain exposure to a fintech stock with solid long-term growth potential.