For those looking to revitalize their portfolios following a tumultuous period last year, tax preparation and accounting software firm Intuit (NASDAQ: INTU) doesn’t appear as a logical starting point. According to an August 2019 report by the Pew Research Center, roughly 16 million Americans were self-employed. In other words, most U.S. workers file relatively uncomplicated tax forms. However, a coming transition could change the framework bullishly for INTU stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Fundamentally, all employees of a business enterprise fill out a Form W-2 (wage and tax statement). Outside of unusual circumstances – such as workers investing heavily in master limited partnerships – the tax forms are intuitive and straightforward. However, it’s up to the individual taxpayer if they want to tack on complex transactions to their W-2s. Otherwise, the form itself is essentially child’s play.

Not surprisingly, INTU stock doesn’t benefit from simple W-2s. Indeed, Intuit’s website offers free filings for such “customers.” No, the company gains relevance as tax complexities rise. Therefore, the burgeoning gig economy may represent a windfall for the tax-prep software giant.

Unlike employees, gig workers (technically known as independent contractors) are in business for themselves. Thus, the Form 1099s that these professionals fill out feature greater complexities. Through this form and the myriad accompanying documents, the Internal Revenue Service can not only determine how much gig workers made but the underlying fiscal value chain: gross sales, cost of goods sold, legal deductions, and net profits (or loss).

It can be a nightmare for the unaccustomed. On the other hand, the circumstance bodes very well for INTU stock.

Corporate Standoffs Cynically Boost INTU Stock

To be sure, INTU stock doesn’t natively appear as a resoundingly bullish opportunity. In the trailing year, shares tumbled nearly 34%. In addition, the U.S. Bureau of Labor Statistics reports that the self-employment rate trended down between 1994 through 2015. However, the standoff between corporate employees and the request to return back to the office may lift Intuit long term.

Back during the onset of the COVID-19 pandemic, both employers and their workers shared a common goal: to maintain operations so that their businesses could run and provide paychecks. Therefore, the pivot to work from home made sense. However, with the common enemy in the form of the SARS-CoV-2 virus fading, remote work becomes more of a liability.

Sure, one could make the argument that enterprises can downsize their physical footprint, saving on real estate expenses. However, as a recent Reuters article pointed out, several drawbacks to a permanent shift to working from home exist. For starters, there’s the issue of lost productivity.

While worker bees swear that they’re being more productive, such a response is akin to men measuring their height or women self-reporting their weight. Unless one is completely and hopelessly naïve, some fudging of numbers is to be expected.

On a much more serious note, remote settings expose companies to a greater risk of cyberattacks. Using industry lexicon, corporations that allow a work-from-anywhere policy become vulnerable to expanded attack surfaces.

Put together, companies will be less receptive to the idea of remote employees. Should a recession materialize, they won’t have to be at all. This backdrop then supports INTU stock as people abandon their employers with the aim of working under their own terms.

Of course, these new gig workers must then file 1099s, bolstering the case for INTU stock.

Is INTU Stock a Buy?

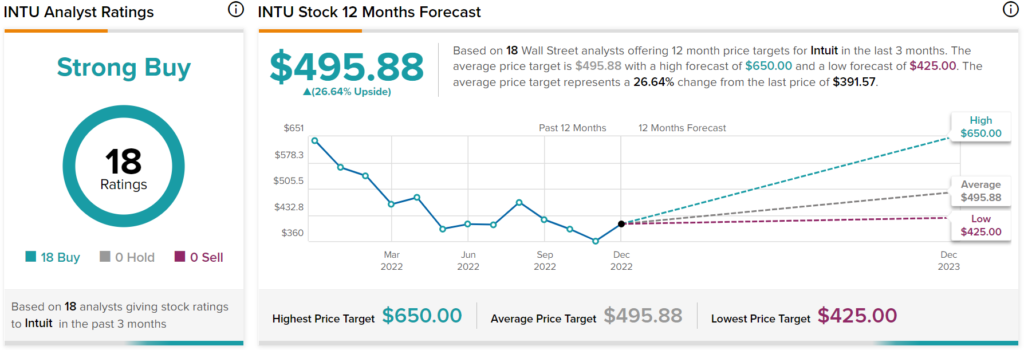

Turning to Wall Street, INTU stock has a Strong Buy consensus rating based on 18 Buys assigned in the past three months. The average INTU price target is $495.88, implying 26.64% upside potential.

Positive Fiscal Momentum May Lift Intuit Stock in 2023

While Intuit doesn’t always attract retail investors’ attention, market participants should note that presently, INTU stock carries a consensus strong buy rating. Part of the reason may center on its earnings performance. Since the company’s fiscal third quarter of 2022 (results posted May 23, 2022), Intuit beat its per-share profitability target.

To be fair, one drawback is that against traditional metrics, INTU stock appears overvalued. For instance, the market prices Intuit at 28.71 times forward earnings. However, the sector median value is only 23.84 times.

Still, it’s difficult to overlook the positives. For instance, Intuit features a gross margin of 80%, affording the business pricing flexibility of its services. In addition, it commands a return on equity of 12.55%. This ranks above the sector median value of 2.61%, thus reflecting a superior capacity to convert equity financing into profits.

Finally, Intuit posted an Altman Z-Score of 7.49, reflecting low bankruptcy risk. With so many uncertainties plaguing the global economy, Intuit’s fiscal stability – along with its fundamental relevance – could spark upside for INTU stock.