While few, if any, investors appreciate watching their portfolios plunge into redness amid market volatility, the downfall creates contrarian opportunities. Essentially, the silver lining centers on acquiring relevant securities at steep discounts. Arguably, gig economy stocks represent one of the most attractive sectors to consider. Four tickers – INTU, UPWK, FVRR, and ROVR – offer intrepid market participants substantial potential for upside.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Let’s set up the broader framework. When the COVID-19 crisis initially capsized the global economy, the labor force suddenly found itself staring at a predominant theme: telecommuting or working from home (WFH). Naturally, companies that facilitated remote operations benefited handsomely during the early phase of the new normal.

However, as TipRanks contributor Joey Frenette noted, some of the biggest WFH securities lost over 80% of their equity value from peak to trough. However, the argument for gig economy stocks is that the underlying companies can pick up where WFH specialists left off. Essentially, the gig economy – a catch-all term to describe how independent contractors earn a living – represents a burgeoning market.

According to data from Statista, the projected gross volume of the gig economy is expected to reach $455.2 billion. Further, it’s possible that with many employees reluctant to go back to the office, the subsequent battles between management and workers may result in a greater-than-anticipated expansion of independent contractors. Theoretically, this should bode very well for gig economy stocks.

To be fair, brewing concerns about a global recession may tamp down on some worker bee bravado. Nevertheless, having tasted the independence that goes along with the gig workers’ lifestyle, at least some corporate employees will take the plunge.

In anticipation of this trend, investors should consider the following gig economy stocks to buy.

Intuit (NASDAQ: INTU)

Although seemingly not a relevant name among gig economy stocks, accounting and business software specialist Intuit will likely be crucial for newfound independent contractors. Essentially, one of the distinguishing factors between the corporate and gig economy professions is tax-filing requirements.

Put simply, employees file W-2 forms with the Internal Revenue Service, while independent contractors file 1099 forms. All other things being equal, W-2s are easy to file since the underlying hiring companies provide relevant tax data to the IRS. On the other hand, 1099 filers receive the same tax treatment as businesses. Rather than earning a salary, gig workers generate income, which involves various disclosures and deductions.

Almost immediately, first-time gig workers encounter a culture shock regarding taxation. However, Intuit’s tax software can help ease the blow. Having lost about 40% of market value on a year-to-date basis, INTU represents one of the gig economy stocks to pick up on the cheap.

Is INTU Stock a Buy, According to Analysts?

Turning to Wall Street, INTU stock has a Strong Buy consensus rating based on 17 Buys, one Hold, and zero Sell ratings. The average INTU price target is $539.41, implying 28.1% upside potential.

Upwork (NASDAQ: UPWK)

Offering a marketplace for freelancers to find contract assignments, Upwork presents a more direct exposure to gig economy stocks. Essentially, the company provides a platform that helps connect professional talent with enterprises looking to fill a specific need. In this manner, the companies receive critical services while the independent contractors receive payment for services rendered. It’s a win-win.

To be fair, investors must take on additional risks should they move forward with UPWK stock. Fundamentally, the underlying company is mostly geared toward a growth narrative. For instance, in the second quarter, Upwork generated revenue of $156.9 million, up over 26% against the year-ago period.

That’s great. However, its net losses continued to expand. Currently, its retained earnings line item features a loss of $300 million. For comparison, in 2016, this metric was a loss of $119.5 million.

Still, with shares down over 63% year-to-date and enjoying fundamental relevance, UPWK is one of the gig economy stocks to consider for speculators.

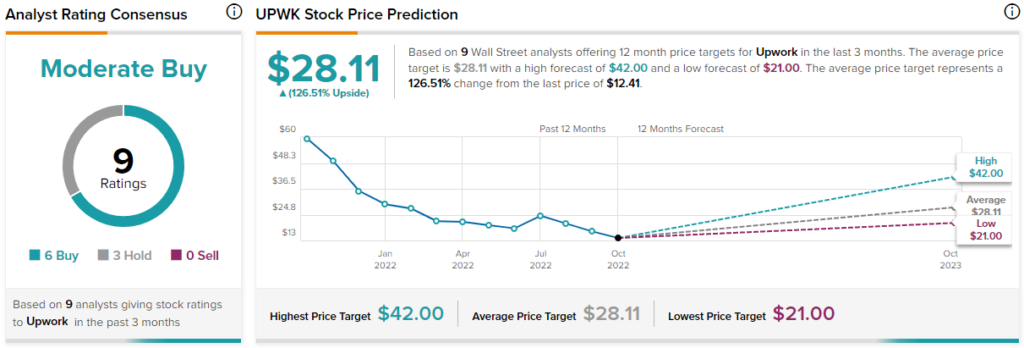

Is UPWK Stock a Buy, According to Analysts?

Turning to Wall Street, UPWK stock has a Moderate Buy consensus rating based on six Buys, three Holds, and zero Sell ratings. The average UPWK price target is $28.11, implying 126.5% upside potential.

Fiverr (NYSE: FVRR)

For those that want to take even greater risks for possibly greater rewards among gig economy stocks, they should target Fiverr. Another marketplace for freelancers, one of the immediate differences between FVRR and UPWK centers on chart performance. The former is down nearly 76% year-to-date, reflecting severe volatility.

As with its direct rival, Fiverr is geared toward growth, just much more heavily. For instance, the company’s three-year revenue growth rate stands at 41.1%, rating better than nearly 86% of the broader interactive media industry. However, it rates very poorly in terms of profitability. Its net margin is -28.5%, which comes in worse than nearly 72% of its peers.

Given its close proximity to UPWK, FVRR presents significant risks. It may be possible that only one wins out in this battle of gig economy stocks. Nevertheless, if you want to hedge your bets, Fiverr may be intriguing.

Is FVRR Stock a Buy, According to Analysts?

Turning to Wall Street, FVRR stock has a Moderate Buy consensus rating based on three Buys, two Holds, and zero Sell ratings. The average FVRR price target is $44.00, implying 54.4% upside potential.

Rover Group (NASDAQ:ROVR)

One of the most intriguing angles among gig economy stocks to buy, Rover Group also provides a freelancer platform. As with Upwork and Fiverr, the idea here is to connect service providers with service seekers. However, the main difference centers on purposes. Rather than benefiting business ecosystems, Rover is all about a man’s best friend.

From pet sitting, dog boarding, and dog walking, among other services, pet owners now enjoy a wide canvas for fulfilling their needs. Fundamentally, Rover enjoys two major catalysts. First, the pet industry in the U.S. represents a massive and still-burgeoning sector. From 2018 to 2021, this segment increased from $90.5 billion in total revenue to $123.6 billion.

Second, if fears of a brewing recession cause some employees to capitulate and return to the office, their newfound freedom will evaporate. However, since millennials show a penchant for pet ownership, many of those returnees will probably need pet-care services. That’s where Rover could become exceptionally relevant.

Is ROVR Stock a Buy, According to Analysts?

Turning to Wall Street, ROVR stock has a Moderate Buy consensus rating based on two Buys, two Holds, and zero Sell ratings. The average ROVR price target is $5.50, implying 34.8% upside potential.

Conclusion: Several Gig Economy Stocks to Suit Your Style

Even before the COVID-19 crisis, the gig economy represented a viable subsegment of broader commercial activities. However, with the post-pandemic new normal, more people are attuned to the benefits of the gig workers’ lifestyle. Better yet, investors can approach this sector with several options to choose from, ranging from more conservative ideas like INTU to riskier ones like FVRR.