These are not the best of times for the electric vehicle (EV) sector. Against a frail economic backdrop, what not long ago seemed to be a fledgling industry on the cusp of mainstream adoption has struggled with demand cooling down. Additionally, operating in the current interest-high climate amidst an extremely competitive environment has become increasingly difficult for many of the companies trying to ride this secular trend.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

The malaise has spread across the board, and, of course, has also affected EV stocks. Shares of segment leader Tesla have suffered in recent months, but being the EV king, its pullback has been far less pronounced than the ones experienced by smaller companies vying for a piece of the action.

Companies like Rivian Automotive (NASDAQ:RIVN) and Lucid Group (NASDAQ:LCID), for instance, whose shares have taken a beating over the past 12 months and are down by a respective 53% and 69%. But with their share prices having retreated by such a substantial extent, might it be time to start loading up on companies like them?

Needham analyst Chris Pierce has been keeping a tab on these two and has recently been assessing their prospects, so we decided to find out what he makes of their chances. Additionally, we also used the TipRanks database to see how the rest of the Street expects the future to pan out for these names. Let’s check the results.

Don’t miss

- ‘A Sector at a Crossroads’: Wells Fargo Predicts at Least 60% Upside for These 2 Beaten-Down Fintech Stocks

- Bank of America Says This ‘Buy’ Signal Could Trigger an 11% Upswing in S&P 500 Next Year — Here Are 2 Stocks the Banking Giant Likes Right Now

- ‘Putting the Fun Back in Fundamentals’: Deutsche Bank Says These 3 Homebuilding Stocks Look Attractive Right Now

Rivian Automotive

Back in November 2021, Rivian made quite a bit of noise as it entered the public markets in a blockbuster IPO, with its credentials boosted by the backing of Amazon and Ford. The modus operandi was to become a dominant player in the EV industry, offering top-tier electric trucks and SUVs.

However, that proved more difficult than possibly expected at the outset. Ramping up its premium electric truck – the R1T – ran into serious issues, and the company experienced a wide range of production difficulties, including problems related to chip shortages, Covid-19-related disruptions, and the reorganization of vehicle assembly lines. These issues disrupted production and also had a negative impact on investor confidence.

But while investor sentiment might still be shaky, Rivian appears to have addressed many of the issues that initially plagued it, and the recently released Q3 report had enough positive aspects to suggest the company might be turning a corner.

Even against the backdrop of soft demand, the company delivered a record 15,564 vehicles in the quarter, exceeding the 14,900 expected on the Street. There were other positive results as well, with revenue increasing an impressive 150% year-over-year to $1.34 billion, surpassing analyst expectations by $30 million. Likewise, on the bottom line, adjusted EPS of -$1.19 performed much better than the -$1.34 consensus estimate. Looking ahead, Rivian raised its full-year production outlook from 52,000 units to 54,000, surpassing Wall Street’s forecast of 53,600.

Assessing these strong results, Needham’s Pierce calls Rivian a “safe harbor vs poor EV adoption sentiment” and sees plenty of reasons to back this EV player. “RIVN has order book visibility through ’24, is likely to see increasing ASPs as they introduce new variants (Max battery Pack) and burn through reservations made at lower prices, with improving margins as higher production drives increased fixed cost absorption and also seeing bill of material cost downs from suppliers helping per unit costs,” Pierce said. “We struggle to find an issue with the direction of the business and the financial model, with the interest rate backdrop and current low investor patience levels as factors outside of RIVN’s control.”

“We continue to see RIVN as deserving of both longer term view and a premium multiple as they increasingly look like a winner in the ICE to EV transition, with solid demand metrics, pricing power, and improving margins as peers struggle in all three categories,” Pierce went on to add.

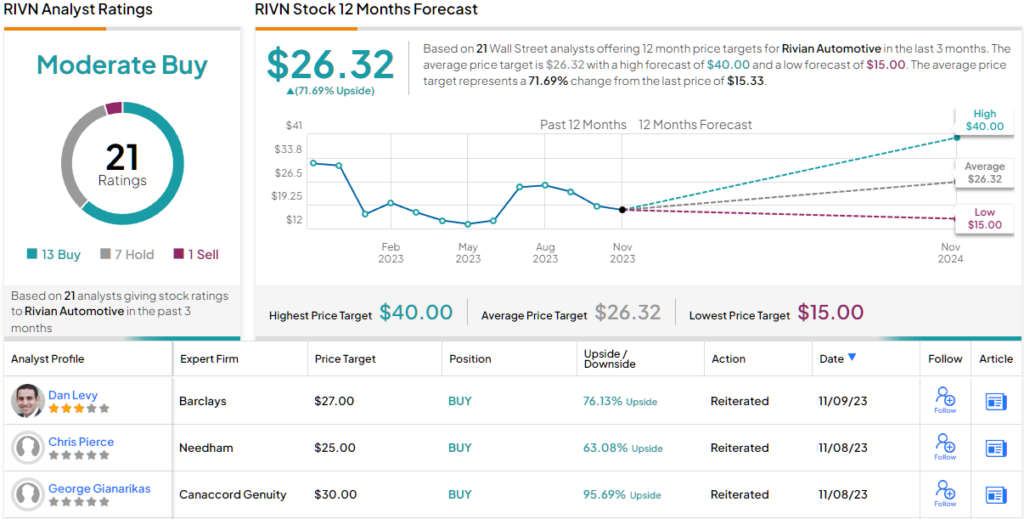

Accordingly, Pierce keeps RIVN on his Conviction List, reiterating a Buy rating along with a $25 price target. If correct, investors could be lining their pockets with a 63% gain.

That price target is a little lower than the Street’s average, which currently stands at $26.32, making room for 12-month returns of ~72%. All told, the stock claims a Moderate Buy consensus rating, based on 13 Buys, 7 Holds and a single Sell. (See Rivian stock forecast)

Lucid Group

The struggles of the EV industry and EV stocks, in particular, are well epitomized by Lucid Group. However, the company actually has several aces up its sleeve, one being CEO Peter Rawlinson, formerly of Tesla and the chief engineer of the Model S, and the other being its lauded Lucid Air, an award-winning electric sedan considered one of the best electric cars on the market.

Despite this impressive introduction, the company has been unable to overcome many of the issues that have hampered its progress. The rough macro conditions have hit Lucid particularly hard, leading the company to repeatedly lower its production expectations. This was the case again in the recently reported Q3 print. Lucid now anticipates producing between 8,000 and 8,500 vehicles this year, down from the previous forecast of 10,000 vehicles.

The company delivered 1,457 vehicles in the quarter, resulting in revenue of $137.8 million. This not only represented a 29.5% drop compared to the same period a year ago but also fell $57.4 million below expectations. That said, while the adjusted EBITDA loss widened from 3Q22’s -$552.9 million to -$624.1 million, this figure exceeded the Street’s forecast of -$701 million and is a testament to Lucid’s cost management efforts bearing fruit.

Meanwhile, investors have been losing faith in this name, with the shares down, as mentioned above, by nearly 70% over the past 12 months. Needham’s Pierce, however, remains on board for now. Nevertheless, he believes that it will be challenging for sentiment to turn positive again without concrete evidence to show that the business is on the right track.

Following the Q3 readout, Pierce wrote, “We continue to believe in LCID’s industry leading battery and drive train technology, and continue to see legacy OEMs struggle to make affordable EVs, with LCID a willing potential technology partner to drive down costs, particularly on the battery tech side, but we lower our estimates again on lower deliveries, driving lower margins, with potential upside pushed out a year in our model. LCID’s Gravity SUV launch is a potential soft catalyst, as are ramping units to fulfill a larger number of orders from Saudi Arabia, but hard evidence of better numbers is hard to spot currently.”

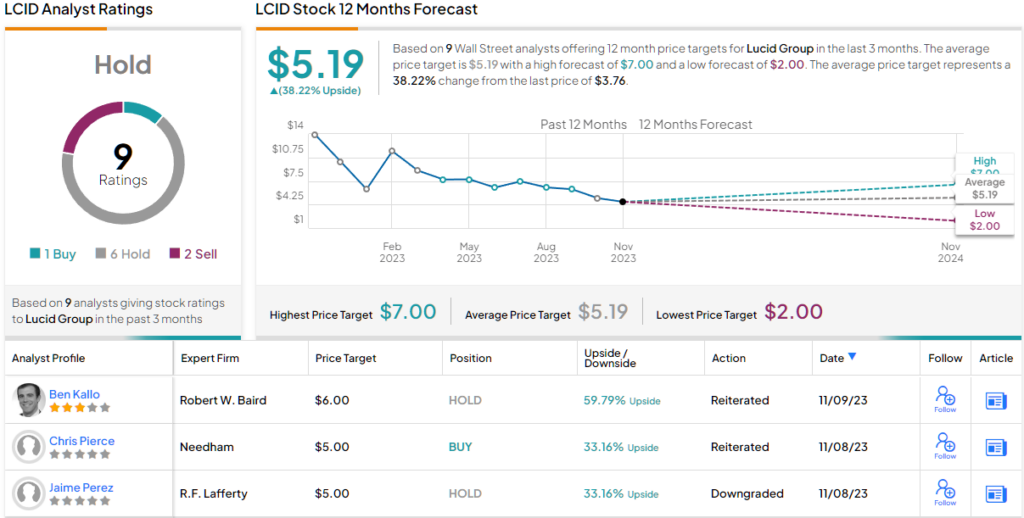

As such, Pierce keeps a Buy rating on LCID stock along with a $5 price target, which implies 33% upside from current levels.

Pierce, however, is currently the Street’s lone LCID bull. Elsewhere, the stock receives an additional 6 Holds and 2 Sells, for a Hold consensus rating. That said, most seem to think the shares are now somewhat undervalued; the $5.19 average target makes room for 12-month gains of 38%. (See Lucid Group stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.