Markets have been highly volatile over the past few months, shifting rapidly between ups and downs. However, Bank of America strategist Savita Subramanian sees a strong ‘Buy’ signal that investors should note.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Subramanian is pointing out the Sell Side Indicator, a sentiment gauge with an accurate history of identifying shifts in sentiment on Wall Street. Currently, the indicator is three times closer to ‘Buy’ than ‘Sell,’ a position that suggests a bullish future for equities.”

“The SSI has been a reliable contrarian indicator – in other words, it has been a bullish signal when Wall Street was extremely bearish, and vice versa…” Subramanian wrote, and added, “While higher rates have weighed on equity sentiment, we believe corporates and consumers may hold up better than expected as they have time to adapt.”

According to Subramanian, the Sell Side indicator is pointing toward ~11% gain on the S&P 500 index in the year ahead. Given current levels, this implies that the index may reach a peak of 4,850.

A gain of that magnitude is certain to bring broad-based benefits for stock investors. The analysts at Bank of America are busy for now, looking for potential winners in a bullish stock environment. We’ve opened up the TipRanks database to find two stocks that the banking giant likes right now. Let’s take a closer look.

Don’t miss

- ‘Putting the Fun Back in Fundamentals’: Deutsche Bank Says These 3 Homebuilding Stocks Look Attractive Right Now

- Goldman Sachs Says Utilities and Consumer Staples Stocks Are Set to Outperform as the Presidential Election Approaches — Here Are 2 Names the Banking Giant Likes

- Bitcoin Could Hit $150,000 by 2025, According to Bernstein — Here Are 2 Top Bitcoin Miner Stocks to Bet on It

MongoDB, Inc. (MDB)

Up first is a stalwart of the data platform software industry: MongoDB. This company is well-known as a developer of high-end database systems. MongoDB’s flagship product, MongoDB Atlas, is designed to work with users, allowing customers to use data in their own ways, using their own preferred coding languages – with the best support available, adaptable to customers’ needs, and offering built-in security features.

By the numbers, it’s clear that MongoDB has seen a high level of success. Since releasing its products more than a decade ago, the company has seen them downloaded hundreds of millions of times and has watched its customer base expand to tens of thousands across 100 countries all over the globe. Moreover, from the standpoint of product expansion, the company has trained millions of database builders through its courses.

MongoDB shares are up 88% for the year so far. A significant part of that increase came in June when the tech darling’s stock spiked by 40% after a forecast-beating earnings report.

In its most recent quarterly results, reported this past August for fiscal 2Q24, the company once again exceeded expectations.

The success was built on strong customer growth, with 45,000 new customers as of July 31 this year. MongoDB Atlas revenue was up 38% year-over-year and made up 63% of the quarterly total. For the quarter, revenue reached $423.8 million, beating the forecast by almost $33 million and growing by 40% year-over-year. At the bottom line, the company achieved a non-GAAP EPS of $0.93, a figure that was 48 cents better than expected.

This all points toward a solid growth stock, and Bank of America analyst Brad Sillis builds on that, writing of the company, “We believe that MongoDB is well-positioned to capture share of the $108 billion database market. MongoDB commands formidable competitive advantages such as: 1) a large developer community (405 million downloads of the Community Server), 2) a proprietary document storage model, 3) support of 13 programming languages, and 4) a multi-channel self-serve and direct sales go-to-market. In addition, channel feedback suggests that Mongo (Atlas) is increasingly deployed as the database of choice to support growing AI applications. In our base case, we are modeling a 6-year revenue CAGR of 22% growth.”

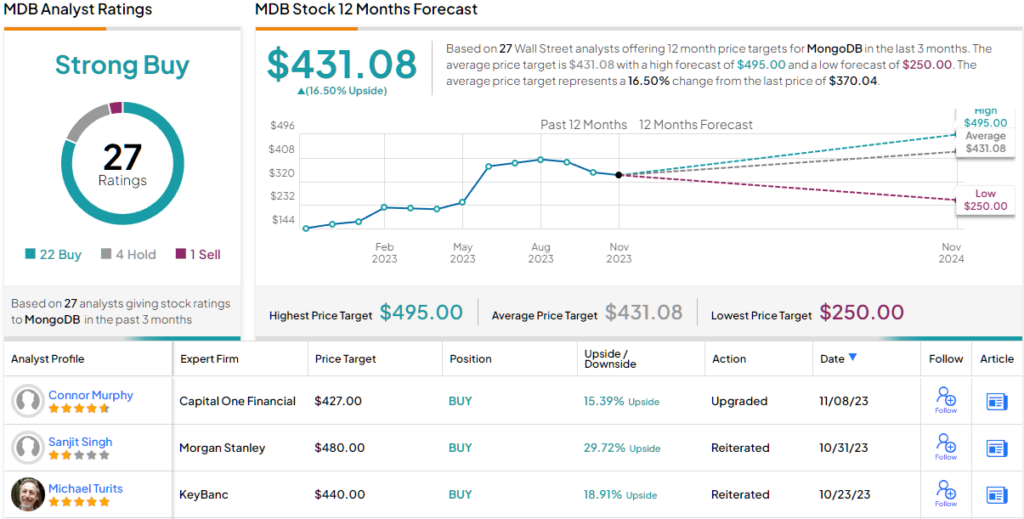

Looking ahead, Sillis sees room for a $450 price target, implying a one-year gain of ~22%, and rates the stock as a Buy. (To watch Sillis’ track record, click here)

Overall, this stock has 27 recent analyst reviews, including 22 Buys, 4 Holds, and 1 Sell, for a Strong Buy consensus rating. The shares are priced at $370, and their $431.24 average target price suggests a one-year upside potential of 16.5%.

Northern Trust (NTRS)

From high tech, we’ll shift to high finance. Northern Trust is a financial services company with a particular focus on wealthy institutions and individuals of high net worth. The company operates as a private bank and provides asset servicing, investment management, and wealth management services for its client base. As of September 30 this year, the company had $1.33 trillion in total assets under management.

Drilling down further, we find that Northern Trust offers a range of services, including alternative asset services, multi-asset solutions, liquidity strategies, and trust and estate services. The company has built a solid reputation based on long-term trust and success, tracing its history back more than 130 years. In recent years, it has become the world’s 19th largest global asset manager and the world’s 7th largest factor-based investor.

However, this year, the bank’s stock has fallen, losing around 20% in the face of serious industry headwinds. These challenges include higher inflation and rising interest rates, which have added complications to the wealth management industry.

This trend is reflected in the latest quarterly report for 3Q23. Northern reported $1.74 billion in total revenue, a 1.1% year-on-year decrease that missed expectations by $3.64 million. The firm’s bottom line, with an EPS of $1.49 per diluted share, also fell short of estimates by a penny.

Despite these challenges, Northern Trust has maintained its common share dividend payments. The company has a dividend history dating back to 1989 and has never missed a quarterly payment. The current dividend, declared at 75 cents per common share for a January 1 payment, annualizes to $3 per share and offers a 4.3% yield.

This stock caught the eye of Bank of America analyst Ebrahim Poonawala, who covers the stock with an upbeat outlook based in part on the current relatively low share pricing. Poonawala wrote, “We believe that the stock offers a compelling entry point to gain exposure to a hard to replicate wealth management franchise that caters to high-net and ultra-high-net worth clientele. While we acknowledge the downside risks to EPS/ROE due to deposit costs and equity/bond market volatility, we see these as reflected in the valuation and consider NTRS well positioned to navigate the cycle.”

These comments back up the analyst’s Buy rating, while his $85 price target points toward a share gain of ~23% in the coming months. (To watch Poonawala’s track record, click here)

The BofA analyst might be bullish – but Wall Street is not yet ready to commit on Northern Trust. The stock has 11 analyst reviews on file, with a 9 to 2 breakdown favoring Holds (i.e. Neutral) over Buys – for a consensus rating of Hold. The stock’s $69.35 trading price and $75.91 average price target combine to suggest ~9% upside in the next 12 months.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.