For investors seeking a bargain, this past week has presented some interesting developments – but it will require a bit of explanation.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

To start with, we saw a retreat in Treasury bond yields and mortgage rates during the first few days of November. The yield on the 10-year Treasury bond slipped to its lowest level since mid-October, and it now stands near 4.6%. Mortgage rates, which had climbed well above 8% in October, frequently move in tandem with the 10-year note, and the average 30-year mortgage rate is now back down below 8%.

These are good moves for stock investors. A decline in bond rates usually indicates a shift back toward equities, and more affordable mortgages will give a boost to homebuilder stocks. And those latter, according to Kenneth Zener, a 5-star analyst from Seaport, are currently trading at attractive prices compared to their book values, after a rough few months.

Zener isn’t the only bull on homebuilders, either. Covering the sector from Deutsche Bank, another 5-star sector expert, Joe Ahlersmeyer, has picked out three homebuilding stocks as particularly attractive right now. We’ve used the database at TipRanks to locate the latest details on Ahlersmeyer’s picks; here they are, along with his comments.

Don’t miss

- Bitcoin Could Hit $150,000 by 2025, According to Bernstein — Here Are 2 Top Bitcoin Miner Stocks to Bet on It

- Top Analyst Sees Opportunity Brewing in These 2 Credit Card Stocks

- TipRanks’ ‘Perfect 10’ List: There’s an Opportunity Brewing in These 2 Top-Rated Stocks

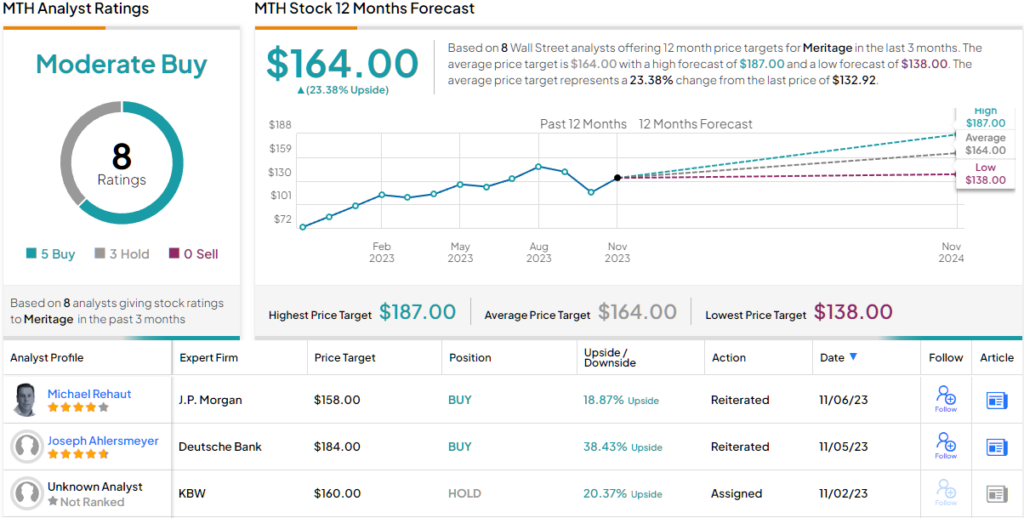

Meritage Homes (MTH)

We’ll start with one of the top US homebuilding companies, Meritage Homes. This company, based on home-closing data from 2022, is the fifth largest builder in the US housing market, and has delivered more than 175,000 homes since its founding in 1985. Meritage is an industry leader, not just in scale but also in the design and construction of energy-efficient homes, and has been recognized as such by the EPA no fewer than 10 times since 2013.

The company boasts a market cap of nearly $4.9 billion and saw its share value spike recently after a strong quarterly earnings report. For Q3 of 2023, Meritage reported a 50% year-over-year orders increase, with 3,474 home orders in the quarter compared to 2,310 in the year-ago period. At the top line, total revenue came to $1.61 billion, up 3% year-over-year and $50 million better than had been expected. At the company’s bottom line, the $5.98 EPS was 87 cents ahead of the forecast.

Drilling down a bit, we find that entry-level homes represented 88% of the sales mix in 3Q23. The average sale price on orders during the quarter was $430,000, for a 2% increase year-over-year. The modest price increase was attributed to the geographic mix of the company’s sales.

Turning to Deutsche Bank’s Ahlersmeyer, we find him upbeat on Meritage after the earnings release, and acknowledging the attractive valuation of the stock at the current time. The analyst writes, “Overall we were pleased with the strong results and favorable outlook in a tough environment for affordability. Management effectively communicated how they are orienting for growth in the coming year, while acknowledging the dynamics that will come into play for modeling purposes, particularly around community count and gross margin. The stock… still trades at approximately book value today, demonstrating why we reiterate MTH as a Top Pick within our Homebuilder coverage.”

These comments back up Ahlersmeyer’s Buy rating on MTH and his $184 price target (up from $180) implies a one-year gain of 38%. (To watch Ahlersmeyer’s track record, click here)

Overall, there is a Moderate Buy analyst consensus rating on MTH, based on 8 reviews with a 5-3 split between Buys and Holds. The shares are selling for $132.92, and their $164 average price target suggests an upside of 23% on the one-year horizon.

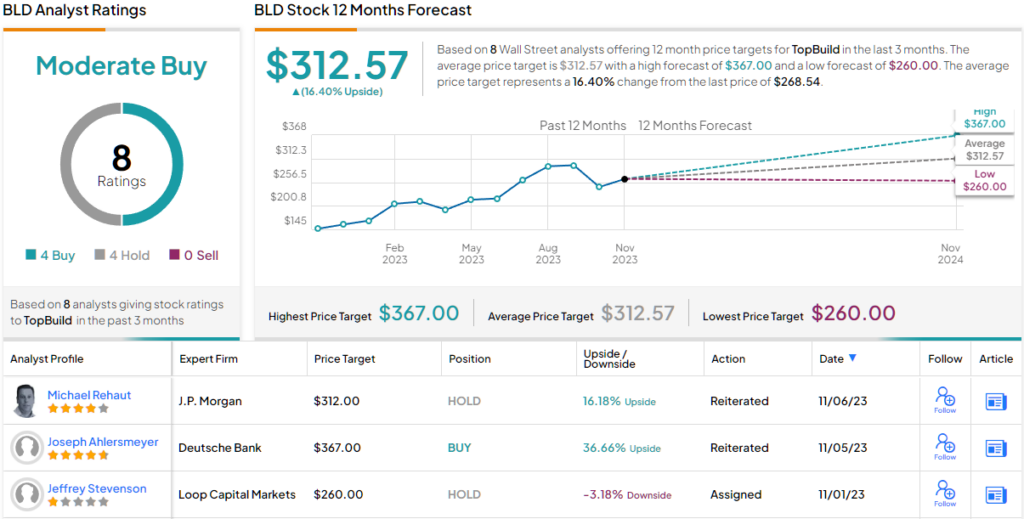

TopBuild Corporation (BLD)

Homebuilders offer an essential product, but they are also customers. TopBuild is a specialist in insulation and building materials for the residential, commercial, and industrial construction markets. The company’s business model includes installation and specialty distributions, and its work ethic is based on operational excellence and solid execution.

The company has set a course toward expansion through acquisition – and in July of this year entered into a $960 million all-cash deal to acquire Specialty Products and Insulation. The move will be funded through both cash-on-hand and loans, and due to the transaction. TopBuild will benefit from a $90 million tax asset.

Since its founding, TopBuild has built itself into an $8.5 billion giant of the construction industry. TopBuild’s revenues have reflected this success, and mostly show a pattern of quarter-over-quarter gains over the past several years. For the most recent quarter, 3Q23, TopBuild reported a top line of nearly $1.33 billion, for a 2.3% year-over-year increase – and beating the forecast by almost $40 million. The company’s EPS, $5.43 by non-GAAP measures, was 13% better than in the year-ago quarter and was 87 cents better than the estimates.

Ahlersmeyer takes a long-term upbeat view of BLD shares, based on a combination of forming tailwinds and sound product demand, writing in his recent note, “Single-family remains resilient and we continue to see tailwinds on the horizon from energy efficiency… Looking to next year, BLD naturally views early signs of solid single-family starts into ‘24 as an important driver of potential growth, and see demand in multi-family as solid partway into next year on still elevated backlogs, despite the slowdown in starts. The outlook for rates appears to have turned a corner in recent days, but even the company’s comments before the Fed meeting Thursday showed that BLD’s posture remains positive on demand, and oriented toward growth in the year ahead.”

The analyst goes to rate TopBuild as a stock to Buy, and while the price target is lowered from $372 to $367, it still points toward a 37% share price increase in the next 12 months.

Overall, BLD shares get a Moderate Buy consensus rating based on an even split of 4-4 between Buys and Holds among the analyst reviews. The shares are selling for $268.54 and their $312.57 average target price implies a 16% one-year upside potential.

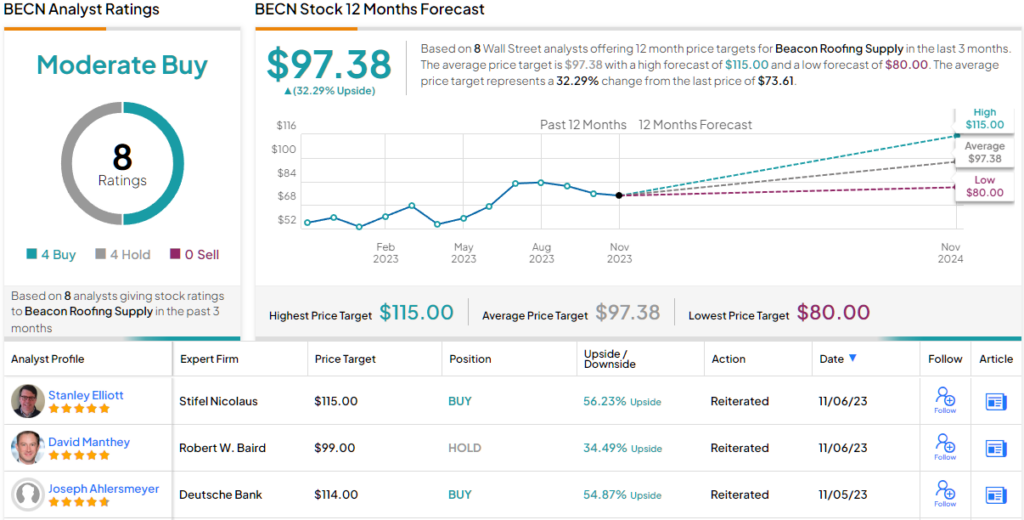

Beacon Roofing Supply (BECN)

What’s a home without a roof? The last Deutsche Bank pick is Beacon Roofing Supply, a major supplier of roofing materials to the home construction industry. The company offers a wide range of brands, including some of the industry’s best-known names, as well as roofing products of every sort. Builders can find asphalt shingles, tile and wood roofing, slate and other natural shingles, metal sheeting, and various roof rolling materials for the low-slope roofs commonly encountered in light industry and commercial projects.

While the company’s chief products are for roofing, Beacon also offers building materials of other sorts. Customers can find lumber and composite materials, plywood products, decking materials, skylights and window installations, even HVAC ducting and installations.

Beacon’s leading position in its field has pushed it to a $4.70 billion market cap, while the company’s revenues show a highly seasonal pattern. That pattern is simple – Beacon scores its highest quarterly revenue during the warm months of Q2 and Q3, when roofing work booms. Business slows down during the winter. In the last quarter reported, 3Q23, the company’s revenues came in at $2.58 billion, for a 6.6% increase from the previous year’s third quarter, roughly in-line with the Street’s $2.59 billion forecast. On earnings, the company’s adj. EPS came to $2.85, conclusively outpacing the $2.54 consensus estimate. Looking ahead, management raised its FY23 EBITDA guidance from the prior $850-890 million range to between $910-930 million, thereby implying 4Q EBITDA of $197-217 million, exceeding the $186 million the analysts were looking for.

Deutsche Bank’s Ahlersmeyer liked what he saw in the quarter and points out an anticipated investor-pleasing move. “The company again expects to do buybacks in ’23 after recently pausing them following the repurchase all of its outstanding preferred equity in July. No doubt, stronger FCF offers the opportunity to once again take advantage of the stock’s attractive valuation. We expect continued solid execution in the coming quarters,” he wrote.

All of this added up to a Buy rating for Ahlersmeyer, who increased his price target from $108 to $114, suggesting an upside of ~55% in the year ahead.

Once again, we’re looking at a stock with 8 recent analyst reviews and a Moderate Buy consensus rating based on 4 Buys and Holds, each. The stock is selling for $73.61 and its $97.38 average price target implies a 32% gain in the year ahead. (See Beacon stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.