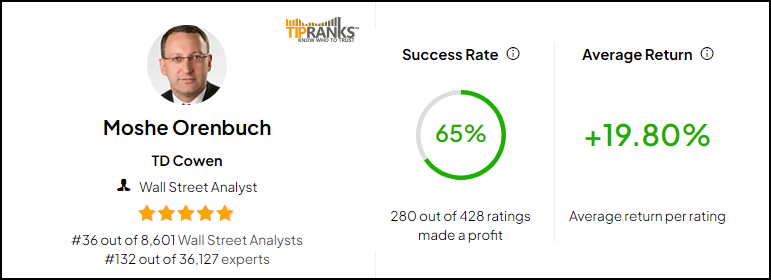

Consumer spending has long been a key driver of the US economy. But consumer credit is sometimes overlooked, and one of the Street’s top analysts, Moshe Orenbuch from TD Cowen, brings our attention to just that point in a note published late last month. For Orenbuch, consumer credit, particularly the credit card companies catering to it, presents a true opportunity for investors going forward.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Orenbuch, who is ranked in the top 1% of all of Wall Street’s analysts, notes some important factors that credit card investors should consider. First, consumer savings increased during the pandemic – but have been spent down in the last two years. Second, consumer spending remains strong, despite the spend-down in savings – and that is leading consumers to rely more on credit. This has created a strong environment for credit issuers.

Summing up the situation, the 5-star analyst writes, “Card balances have continued to grow rapidly, driven by resilient (though moderating) credit card spending and moderation in payment rate. Balances have exceeded 2019 levels, and should grow 8.5-9% this year. Credit has continued to normalize across the spectrum as expected, and should fully normalize by 4Q23, though issuers continue to see good opportunities for originations. NII (net interest income) has outperformed on non-interest income this year as consumers’ excess liquidity has been used up.”

So, let’s take a moment to look more closely at two credit card companies which Orenbuch has tagged. He sees a real opportunity brewing in these two credit card stocks; we’ll draw the latest details from the TipRanks database, combine it with Orenbuch’s comments, and find out why.

Don’t miss

- TipRanks’ ‘Perfect 10’ List: There’s an Opportunity Brewing in These 2 Top-Rated Stocks

- Morgan Stanley Says There’s a Buying Opportunity in Theme Park Stocks — Here Are 2 Names the Banking Giant Likes

- ‘The Stage Is Set for a Rally’: Canaccord Sees up to 290% Upside for These 3 Stocks

Discover Financial Services (DFS)

We’ll start with Discover Financial Services, the company that stands behind the Discover card. This card is best known for offering one of the first cash-back customer reward programs in the credit card industry, a small percentage return to card users based on their total charges. The program put some meat behind their early ad slogan, ‘It pays to Discover,’ and helped the company, which was founded in 1985, expand to become a serious competitor for established card companies such as Mastercard and Visa.

In its current incarnation, the company offers a wide range of consumer financial and banking services – starting with several versions of the Discover card, but also including checking, savings, and retirement accounts, and personal, student, and home loans. Discover Financial Services is an almost $22 billion company with a global footprint, and its Discover card is accepted worldwide.

This company reported its 3Q23 earnings last month, and the results were somewhat mixed. On the one hand, revenue was up; DFS showed a top line of $4.04 billion, for a 16% year-over-year increase – and it beat the forecast by over $80 million. Importantly, the loan business was up strongly year-over-year. Discover recorded $122.7 billion in total loans for the third quarter, for a y/y increase of 17%. At the bottom line, however, the company’s EPS of $2.59 was down 27% from the prior year, and came in 59 cents per share below the estimates.

In addition to paying back card users, Discover also pays a dividend to shareholders. The company’s latest dividend, declared for a December 7 payout, is set at 70 cents per common share. This annualizes to $2.80, and gives a forward yield of 3.2%.

Turning to Orenbuch’s outlook, he believes investors have an opportunity to get in while sentiment is unjustifiably low and writes of the stock, “DFS is our top pick among the credit card issuers because of lower acquisition cost, strong loan growth and favorable customer base (primarily prime revolver). DFS’s current valuation is below historical average, a result of overhang from recent compliance lapses. We believe this represents an attractive entry point as these issues will eventually come to pass. Most importantly, they do not affect the way DFS interacts with its customers in any material way, plus the company has a great brand. DFS’s delinquency formation will also likely slow down in 1Q24.”

These comments support Orenbuch’s Outperform (Buy) rating, while his $100 price target points toward a 15% gain for the next year. (To watch Orenbuch’s track record, click here)

Overall, Discover gets a Moderate Buy rating from the Street’s analyst consensus, based on 17 recent reviews that include 7 Buys and 10 Holds. The shares are trading for $87.18 and their $102.24 average target price suggests a one-year upside potential of 17%. (See Discover’s stock forecast.)

Synchrony Financial (SYF)

The next stock on our list is based in Stamford, Connecticut. Synchrony Financial offers a set of consumer finance products, including credit, installment lending, loyalty programs and other promotional financing, and consumer savings products. These services, particularly the savings options, are backed by the FDIC, and are offered by the company’s wholly-owned subsidiary, the online bank, Synchrony Bank.

Synchrony is a leader in the online consumer credit and financial service sector, and has worked that angle to build itself into a $12.5 billion firm. The company has been traded publicly since 2014, and has substantial exposure to the credit card segment. Synchrony offers a wide range of retail cards, including Sam’s Club, QVC, and Lowe’s, as well as its own network of Synchrony-branded credit cards.

In the recently reported 3Q23 earnings, Synchrony’s card business generated nearly $92.1 million in volume. At the bottom line, Synchrony reported an EPS of $1.48 for the quarter, 6 cents per share better than had been anticipated. The company’s sound earnings fully covered the common share dividend, which was declared for 25 cents per common share. This payment’s $1 annualized rate gives a yield of 3.3%, enough to provide a measure of protection against the current rate of consumer price inflation. Synchrony’s total capital return to shareholders was $254 million in the quarter, including both dividends and share buybacks.

Orenbuch likes this banking company’s brand partnerships, as well as its growth profile. He writes, “As SYF partners with leading brands in fast-growing areas (e.g., e-commerce) or with huge customer bases, it can benefit from the partners’ secular growth or increased penetration of its cards in the partners’ sales. Hence, we believe SYF should be able to achieve industry-leading growth going forward like it has historically. Unlike most peers, SYF’s earnings are partially protected from adverse conditions (e.g., rising losses, regulatory changes) due to its retailer sharing agreement with partners (RSA). This will be an advantage for the company if the economy worsens from here.”

Quantifying this stance, Orenbuch rates the shares as Outperform (Buy), with a $34 price target that implies one-year share appreciation of 13%.

Taking a macro-view of Synchrony’s position, we find the Street giving these shares a Moderate Buy consensus view. This is based on 15 reviews, including a 7-7 split between Buys and Holds, and 1 Sell. The shares are trading for $30.15 and have an average price target of $36.29, suggesting an upside of 20% on the one-year time frame. (See Synchrony stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.