Savvy investors know that some valuable stock sectors just don’t get the attention they deserve, and finding those underappreciated sectors is a vital skill for successful investing. Big Tech, for example, may have a reputation for taking up all the oxygen in the room, but it’s hardly the only game in town.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Agribusiness is one of the underappreciated sectors. The companies that work the land, produce the fertilizers, and deliver the farm equipment that support the world’s food supply bring with them one clear advantage – there will always be demand for their products.

A note from Barclays, the multinational banking institution, focuses on the fertilizer market, and notes that “there is now more upside than downside risk around the supply of [the] expected higher demand for potash…”

Potash is a vital ingredient in modern fertilizers and expounding on the issue, Barclays analyst Benjamin Theurer lays out a path for longer-term upside in the potash market. The 5-star analyst writes, “Global potash demand in 2022 reached just 60mn MT, down from over 70mn MT in 2020 and 2021. While for 2023 industry expectations call for a recovery of ~5mn MT to 65mn MT, we don’t expect to see a return to shipment levels pre-Russia/Ukraine conflict and Belarus sanctions until 2024.”

With the prospect of higher global Potash demand in 2024, Theurer has been revising his position on 2 agribusiness stocks that have high exposure to the potash market – updating the position to the tune of double upgrades on his stance and suggesting investors load up on these shares right now. So, let’s take a closer look and flesh out the details with data from the TipRanks platform. Here’s the lowdown, along with Theurer’s comments.

Don’t miss

- Billionaire Steve Cohen Goes Big on These 2 ‘Strong Buy’ Stocks — Here’s Why You Should Follow

- ‘Time to Hit Buy,’ Says Bank of America About These 2 Stocks

- Oppenheimer Expects the S&P 500’s Advance to Continue Into 2024 — Here’s Why These 2 Stocks Might Be Worth Buying

Nutrien, Ltd. (NTR)

Canada-based Nutrien, the first Barclays pick we’ll look at, formed 5 years ago through a merger between PotashCorp and Agrium. The company, which is headquartered in Saskatoon, Saskatchewan, is a major player in the global potash market – and also produces nitrogen fertilizers. In fact, Nutrien is the world’s largest producer of crop inputs, the fertilizers and soil nutrient additives that large scale crops require to thrive.

Getting into details, Nutrien can boast of 20 million tons of potash capacity from its six Saskatchewan mines, making it the world’s single largest soft-rock potash miner. The company’s nitrogen business is the world’s third largest, and is capable of producing 7 million tons of ammonia and 11 million tons of total nitrogen products. Nutrien’s phosphate portfolio is the second largest in North America, and is focused on high-quality phosphate rock; three-quarters of the company’s phosphate sales go to fertilizers.

Despite this value proposition, shares in Nutrien are down sharply this year, by 19%, and so are its revenues. In the 3Q23 report, released early this month, Nutrien reported $5.63 billion in sales. This was down from $11.7 billion seen in Q2, and was down 31% from the $8.2 billion reported in 3Q22. The 3Q23 revenue was also $110 million less than had been anticipated. We should note that Nutrien typically sees a strong seasonal effect on sales, with its best revenues in the second quarter of each year. At the bottom line, Nutrien’s adj. EPS came to $0.35, missing the forecast by 29 cents per share.

For Barclays’ Theurer, however, Nutrien’s current depressed financial results are most likely transitory, and he sees the company recovering going into next year. The analyst writes of this stock, “[We] see improving potash fundamentals as a core driver for our NTR upgrade. Additionally, NTR should continue to benefit from low-cost nitrogen production and solid demand in phosphate. While its retail business in 2024 is not expected to be back to full strength, we see meaningful recovery from low results in 2023. Combining a more favorable potash outlook with solid nitrogen and phosphate results, we assume fairly flat adj. EBITDA in 2024, compared to 2023.”

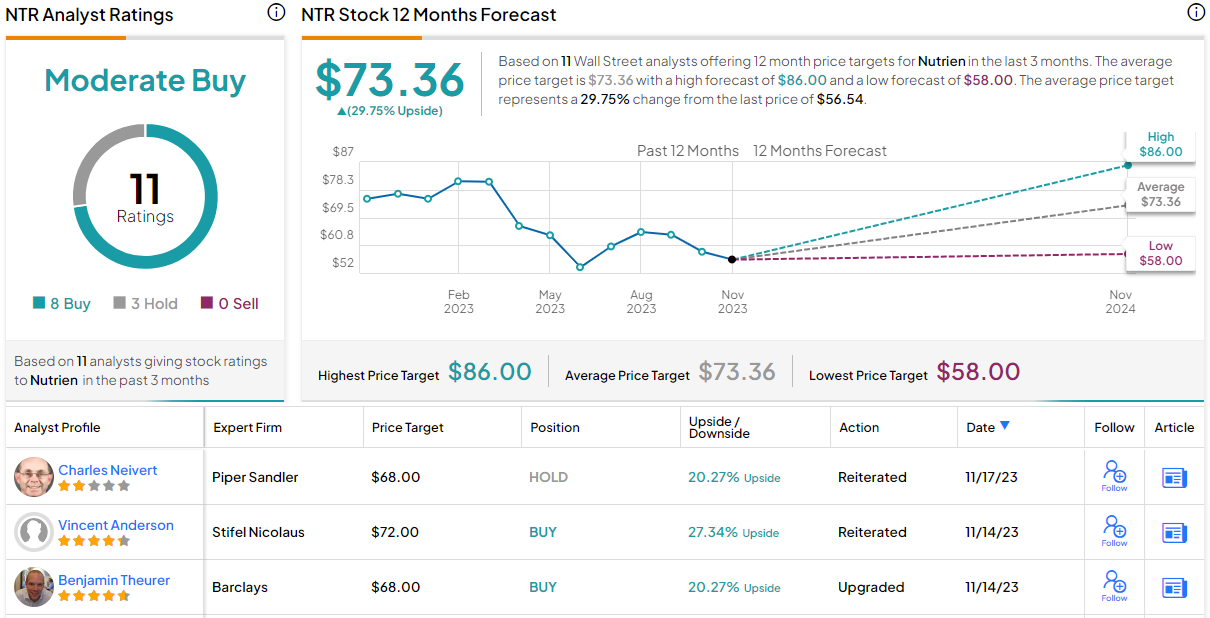

That upgrade Theurer mentions is from Underweight (i.e., Sell) to Overweight (Buy). The analyst puts a $68 price target here, indicating potential for a 20% gain going into next year. (To watch Theurer’s track record, click here.)

Overall, Nutrien has a Moderate Buy rating based on the consensus of the Street’s analysts. The 11 recent share reviews include 8 Buys to 3 Holds. The stock is trading for $56.54 and its $73.36 average price target points toward a one-year potential upside of 30%. (See Nutrien’s stock forecast.)

Mosaic Company (MOS)

The next Barclays-backed name we’ll look at is Mosaic, a Florida-based company that employs 13,000 people on 6 continents, working in the mining and distribution of phosphate and potash for the fertilizer industry. Mosaic is the largest US producer of these minerals, which are among the three most important plant nutrients.

Mosaic has customers in more than 40 countries around the world, and its mining and production operations have an extensive footprint. Notable among Mosaic’s operations are its seven potash and phosphate mines in Saskatchewan and Florida, and its additional five phosphate concentrate sites in Florida and Louisiana. In South America, Mosaic has potash and phosphate facilities in Peru, Brazil, and Paraguay. The company’s Brazilian operations include port and storage units, plus 6.6 million tons of blending capacity.

While agribusiness is essential, it is also subject to pricing and demand cycles, which affect the financials. Looking to the company’s earnings, we find that in recent quarters Mosaic has seen lower prices negatively impact its top and bottom lines. The company’s last reported quarter, 3Q23, showed this, as the firm’s total revenue was down 34% year-over-year to $3.5 billion – although this top line did beat the forecast by $280 million. Mosaic’s Q3 adjusted EPS was 68 cents per share; this was 7 cents below the average estimates.

The company’s EPS did, however, beat the Barclays estimate, and analyst Benjamin Theurer has an upbeat take here, writing of the company, “After a solid quarter with adj. EPS beating our estimates, coupled with positive commentary as to a normalization in its Brazilian operations and more favorable potash fundamentals, we believe MOS relative valuation offers attractive upside potential… While we only make minor adjustments to our 2024 model, especially on EBITDA, where we even slightly lower our assumptions, we believe beyond 2024 MOS holds a fairly favorable outlook in Brazil, while sentiment in the short term, and the company’s relevant potash exposure, both argue in favor of a relative OW rating.”

Theurer’s Overweight (Buy) rating here is an upgrade from Underweight, and his price target, now at $42, implies a 16% upside in the next 12 months.

This stock has a Moderate Buy consensus rating from Wall Street’s analysts, based on 14 recent reviews that include 5 Buys and 9 Holds. The stock is selling for $36.15 and its $41 average target price suggests it will gain 13.5% on the one-year horizon. (See Mosaic’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.