The prospect of a looming recession has been in the background for a while now. Financial prognosticators have generally agreed that one will hit eventually, although its timing and magnitude remain open to debate. But for those concerned about a recession’s impact on the economy and the markets, one legendary Wall Street name has a reassuring take on the matter.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Billionaire Steve Cohen, who runs hedge fund Point72 Asset Management, a firm with $31.4 billion of assets under management, expects a recession will come into play before the end of the year. The good news is that it is “only going to be short-term in nature.”

In fact, once it is out of the way, Cohen anticipates growth will be back on the menu, and he keeps a “pretty positive” stance on the economy.

Cohen, who made his $19.6 billion fortune by favoring high-risk and high-reward trading strategies, is putting his money where his mouth is, and in the meantime has been loading up on the equities he evidently sees as primed to succeed in such an environment. During Q3, he went in big on a couple of names, and it looks like he’s not the only one with a confident take here.

Running these tickers through the TipRanks database, we find that both are rated Strong Buys by the analyst consensus. Let’s see what makes them so.

Don’t miss

- Oppenheimer Says These Are the Best Value Stocks in the P&C Insurance Industry — and They Could Outperform the Market

- ‘Time to Hit Buy,’ Says Bank of America About These 2 Stocks

- Oppenheimer Expects the S&P 500’s Advance to Continue Into 2024 — Here’s Why These 2 Stocks Might Be Worth Buying

Crinetics Pharmaceuticals (CRNX)

For someone with a penchant for high-risk/high-reward plays, then the biotech sector will often be the go-to address, so it’s only natural for Cohen to seek out names in the space. That brings us to Crinetics Pharmaceuticals, a firm dedicated to identifying, creating, and bringing innovative treatments for endocrine diseases and tumors associated with the endocrine system to market.

With biotechs it is all about the pipeline and attendant catalysts and Crinetics has both had some good news on the drug development front and the prospect of more to come.

In September, the company released positive data from the Phase 3 PATHFNDR-1 study of its lead candidate – orally administered paltusotine – indicated to treat individuals with acromegaly, a hormonal imbalance that occurs in adulthood when the pituitary gland produces an excess of growth hormone.

The drug met the primary endpoint in the study, demonstrating strong effectiveness as 83% of acromegaly patients who switched to paltusotine maintained biochemical control of their disease, in contrast to just 4% observed with the placebo. The also drug met all secondary endpoints.

There’s also a second acromegaly trial taking place (for treatment-naïve patients), the aptly titled PATHFNDR-2, with a data readout anticipated in 1Q24. Thatshould help an NDA (new drug application) submission for a broad acromegaly label next year.

Cohen must like what’s on offer here, as during Q3, he opened a new position in CRNX, purchasing 4,225,300 shares. These are currently worth ~$122 million.

Mirroring Cohen’s stance, JMP analyst Jonathan Wolleben reckons paltusotine’s chances of success are high while he also notes the strong prospects of rest of the pipeline and the catalysts ahead.

“We continue to be impressed with management’s execution and believe the PATHFNDR-1 data are sufficient for approval in acromegaly (90% POS),” Wolleben said. “The PATHFNDR-2 data in 1Q24 are key though for a broad label and maximizing paltusotine’s commercial potential. Positively, the PATHFNDR-1 population is identical to the Stratum 2 population in PATHFNDR-2 and demonstrating efficacy in that Stratum is sufficient for success. Thus, we think PATHFNDR-2 is substantially derisked.”

“We are also optimistic for the upcoming Phase 2 carcinoid syndrome data (preliminary data in December, full data 1H24) for paltusotine as injectable SSAs have shown success in acromegaly can translate to the larger carcinoid opportunity,” the analyst further added. “We also remind investors that the first proof-of-concept data for ACTH antagonist CRN04894 in both Cushing’s and congenital adrenal hyperplasia are coming in 2H24, which provide a nice flow of data catalysts through 2024.”

These comments underpin Wolleben’s Market Outperform (i.e., Buy) rating while his $56 price target suggests shares have robust upside of ~98% for the coming year. (To watch Wolleben’s track record, click here)

Wolleben’s take gets the unanimous backing of his colleagues. Based on Buys only – 10, in total – the stock claims a Strong Buy consensus rating. Going by the $48 average target, a year from now, shares will be changing hands for a 69% premium. (See CRNX stock forecast)

Inspire Medical Systems (INSP)

We’ll stay in the healthcare space for our next Cohen-endorsed name but pivot to a different segment. Inspire Medical Systems specializes in developing medical devices designed to address obstructive sleep apnea, or OSA. This is a sleep disorder characterized by repetitive episodes of complete or partial upper airway obstruction during sleep, leading to disrupted breathing and often accompanied by loud snoring and daytime fatigue. The company has developed the world’s first fully implanted neurostimulation device to receive the FDA’s nod of approval for the treatment of the condition.

It’s a value proposition that generated revenue of $153.3 million in Q3, amounting to a 40.4% year-over-year increase yet falling shy of expectations by $1.24 million. Investors did not like that miss, sending shares down in the aftermath. That has been a regular occurrence in recent months with the stock now down by 55% since the year’s July peak. The slide has partly been down to the rise of weight-loss drugs known as GLP-1s, as there is known to be a link between obesity and obstructive sleep apnea. Evidently investors are anticipating a future where fewer individuals experience the onset of OSA.

Meanwhile, Cohen hasn’t flinched. In fact, during Q3, he upped his INSP stake considerably. With the purchase of 653,742 shares, Cohen increased his holdings by 285%. He now owns a total of 883,362 shares, with these commanding a market worth of more than $128.7 million.

Addressing the stock’s pullback, Truist analyst Richard Newitter thinks the recent sell-off “creates an attractive opportunity for investors with a +6-12-month view as INSP continues to penetrate the large/undertreated opportunity.”

“While GLP-1 concerns remain and the relatively in-line Q3 likely was below buyside expectations, INSP is on track to deliver +50% FY23 growth, and +30% next year (at least),” the 5-star analyst went on to say. “At ~4.5x 2024E sales (implied open), GLP-1 downside risks appear priced in, and we see INSP regaining its premium multiple given its superior growth outlook…”

Conveying his confidence, Newitter rates INSP shares a Buy backed by a $240 price target. That figure represents upside of 65% from current levels. (To watch Newitter’s track record, click here)

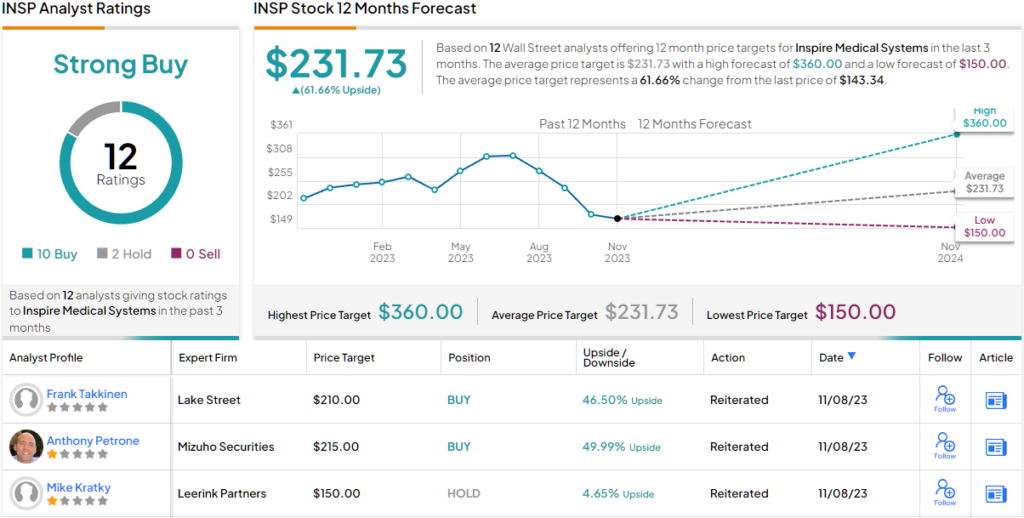

The rest of the Street is hardly less effusive. Based on a mix of 10 Buys against 2 Holds, the stock claims a Strong Buy consensus rating. The forecast calls for one-year returns of ~62%, considering the average target stands at $231.73. (See INSP stock forecas)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.