After a pullback period that began midway through the summer, over the past month, the market has been showing signs it is gathering momentum once again with the S&P 500 up by 7% over the period. The question on investors’ minds is whether the turnaround indicates the bull market is about to resume in earnest rather than it just being a relief rally before another leg down.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Keeping a tab on proceedings, Oppenheimer’s Head of Technical Analysis, Ari Wald, believes the former scenario is the more likely one.

“Our analysis indicates the Q3’23 mid-cycle correction has run its course and the S&P 500’s advance should continue into H1’24,” Wald recently said. “We see enough market capitalization pointed in the right direction to outweigh questionable participation readings that are, at least, oversold. Sentiment has also reached opportunistic levels of pessimism, inter-market trends are stabilizing in a supportive manner, and leadership ratios generally argue against owning safety. The key will be the quality of the next leg higher.”

So, if that is the case, which stocks should investors be loading up on to ride the upward trend? The analysts at Oppenheimer have been looking into this and have homed in on two names they think investors should consider buying right now. We ran these tickers through the TipRanks database to see whether the rest of the Street agrees with these choices. Let’s check the details.

Don’t miss

- Insiders Load Up on These 2 ‘Strong Buy’ Stocks — Here’s Why You Should Pay Attention

- Morgan Stanley Says China’s Education Industry Looks Appealing Right Now — Here Are 2 Stocks to Bet on It

- Goldman Sachs Says These 2 Healthcare Stocks Look Attractive — Here’s What Makes Them Each a ‘Buy’ Right Now

Ormat Technologies (ORA)

We’ll start in the renewable energy space with Ormat Technologies, a specialist in geothermal and recovered energy power generation. Founded in 1965, the company has established itself as a pioneer in the development and implementation of innovative technologies that harness clean and sustainable energy from natural resources. Ormat’s core expertise lies in geothermal energy, where it has developed advanced technologies to tap into the Earth’s heat to generate electricity.

The Reno, Nevada-based firm operates on a global scale with a diverse portfolio of projects spanning across North and South America, Europe, Asia, and Africa. In addition to geothermal power, Ormat is actively involved in recovered energy projects, utilizing waste heat from various industrial processes to produce electricity.

The company’s operations are split into three main segments – Electricity, Product, and Energy Storage – all of which exhibited year-over-year growth in the recently reported Q3 print. The end result was a total revenue increase of 18.3% compared to the same period a year ago, with the top-line reaching $208.1 million, albeit falling short of Street expectations by $0.29 million.

That said, adjusted EBITDA reached $118.3 million, comparing well with the consensus estimate of $114.2 million, while at the bottom-line, adjusted EPS of $0.47 outpaced the analysts’ forecast by $0.09. Looking ahead, for the full year, Ormat’s guidance includes total revenues between $825 million and $838 million, with the midpoint exceeding consensus expectations of $829.42 million.

Scanning these results, Oppenheimer analyst Noah Kaye finds plenty to bolster the bull case.

“Improving trends appear broad-based and in our view reflect business resiliency amid a challenging operating environment,” the 5-star analyst said. “Within Electricity, increasing output for existing assets (Puna/Olkaria), mostly intact organic growth timetables, strong PPA pricing, and the pending acquisition of Enel assets set up favorable multi-year growth dynamics. Products backlog increased 60% q/q and should support healthy revenue and margin uplift in coming quarters. Leverage remains healthy with ORA having visibility on financing for the Enel assets and ITC/PTC benefits reducing capital needs.”

These comments underpin Kaye’s Outperform (i.e., Buy) rating, while his $84 price target makes room for one-year returns of 42%. (To watch Kaye’s track record, click here)

Looking at the consensus breakdown, opinions are split almost evenly. 2 Buys and 3 Holds add up to a Moderate Buy consensus rating. The average target currently stands at $80, suggesting shares will climb 35% higher over the one-year timeframe. (See ORA stock forecast)

Blueprint Medicines (BPMC)

For the next Oppenheimer-backed stock, we’ll pivot to the pharmaceutical sector. Blueprint Medicines specializes in precision medicine and is dedicated to creating innovative therapies for the treatment of cancer and specific hematologic malignancies.

The holy grail for any drug-developing company is to get its products to market, a feat already achieved by Blueprint.

Since June 2021, Ayvakit has been approved by the FDA to treat advanced systemic mastocytosis (SM), a rare hematologic disorder. More recently, in May, the drug became the first and only FDA-approved medication indicated to treat adult ISM (indolent systemic mastocytosis) patients.

In Q3, the first full quarter following the launch of the ISM indication, Ayvakit’s net revenue increased by 90% from the same period a year ago, reaching $54.2 million. $49.1 million of that haul was generated in the U.S., and the total figure comprehensively beat the Street’s forecast of ~$45 million.

While total revenue fell by 14.2% year-over-year to $56.57 million, the significant Ayvakit gains helped the top-line figure come in $5.92 million above expectations. Likewise, EPS of -$2.20 beat the analysts’ forecast by $0.18.

Strong Ayvakit sales and the prospect of further building on that performance underpin Oppenheimer analyst Matthew Biegler’s bullish outlook.

“What impressed us more wasn’t necessarily the increase in scripts, but where those scripts were coming from,” Biegler explained. “By our estimates, new prescribers are meaningfully adding to the prescriber mix. One of the main bear theses ahead of the launch was whether AYVAKIT could penetrate into communities and outside of centers of excellence. While still early, that looks to be the case—and substantially increases the addressable market. We are increasing our peak sales estimates (from $650M to $1,050M).”

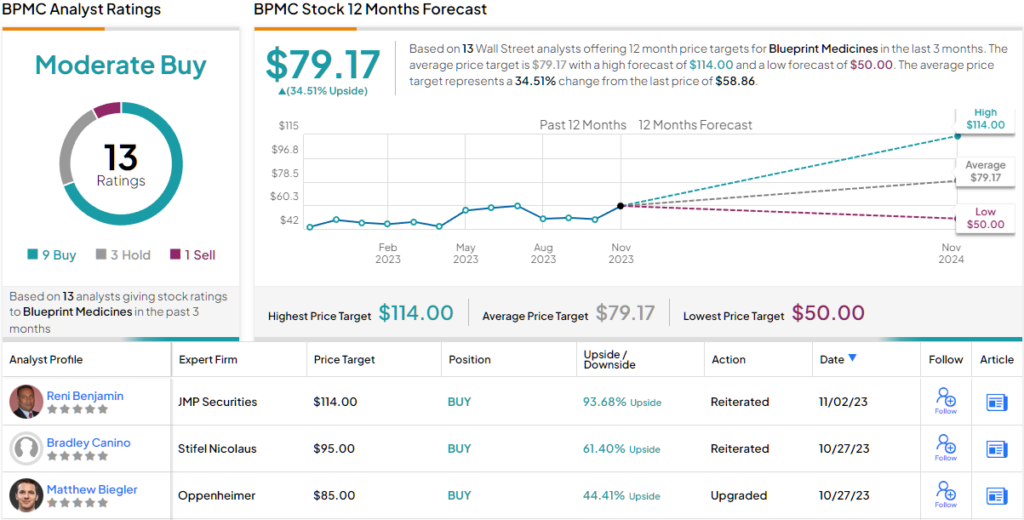

Accordingly, Biegler rates BPMC shares an Outperform (i.e., Buy), backing that up with an $85 price target. Investors could be sitting on gains of 44%, should Biegler’s forecast play out over the coming months. (To watch Biegler’s track record, click here)

What does the rest of the Street have to say? 9 Buys, 3 Holds, and 1 Sell have been issued in the last three months, so the consensus rating is a Moderate Buy. Going by the $79.17 average price target, a year from now, shares are expected to deliver returns of 34.5%. (See BMPC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.