November has a been a good month for the markets, with solid gains on the S&P 500 of 8.5%, bringing the year-to-date haul to ~19%. The question now is, where do we go from here?

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Don’t go anywhere, rather, stay in the stock market, appears to be the recommendation of JPMorgan’s global investment strategist Madison Faller, who points to three factors that should be supportive going forward. First, the US economy is cooling a bit, enough to ease the threat of overheating; second, the rate of inflation continues to ease, and price increases are slowing down; and finally, it looks like the Federal Reserve has finished raising rates, and may start cutting early in the coming year. “Is it mission accomplished? Asks Faller. “No, there’s still more progress to be made (core inflation at 4% is still double the Fed’s target), but it’s notable that things really seem to be moving along in the right direction.”

With those positives driving the narrative, the stock analysts at JPM are running with a bullish thesis. The JPM experts recommend in particular 2 stocks that are showing significant upside potential for the next 12 months. Each has earned a ‘Strong Buy’ consensus rating from the Wall Street analysts, and each shows potential to gain 60% or more on the one-year time frame. We’ve used the TipRanks platform to look up their details – here they are, presented with the JPM commentaries.

Don’t miss

- ‘Bright Spots’ Could Lift These 2 Hotel REIT Stocks Higher, Says Oppenheimer

- There’s an Opportunity Brewing in These 3 Stocks, Says Goldman Sachs

- Buy These 2 Beaten-Down Stocks Before They Rebound, Says UBS

Lexeo Therapeutics (LXEO)

The first stock we’re looking at here, Lexeo Therapeutics, is a biotech researcher at the early clinical stage. The company is working with gene therapy techniques to develop new therapeutic agents in the treatment of ‘genetically defined cardiovascular and central nervous system (CNS) diseases.’ The company uses adeno-associated viruses (AAVs) as transfer agents, to move therapeutic genes directly into the patients’ cells.

Lexeo’s research pipeline currently features seven tracks organized into two broad categories: four tracks under the cardiac programs, and three under the CNS programs. Most of these are at the pre-clinical stage of development, but the company does have two research programs that have advanced to the human trial clinic.

The first of these, LX2006, is a proposed gene therapy candidate designed to deliver FXN, or functional frataxin, a gene useful in the treatment of FA cardiomyopathy. This drug candidate has received both Orphan Drug and Rare Pediatric Disease designations from the FDA, and is currently under investigation in the SUNRISE-FA trial, an open-label, ascending dose Phase 1/2 clinical study.

The second clinical-phase drug candidate, LX1001, is a potential treatment for Alzheimer’s disease, based on the APOE4 gene. The drug candidate has a potential patient base some 900,000 strong and is currently being evaluated in its own open-label, ascending dose Phase 1/2 clinical trial, dubbed LEAD. LX1001 has been granted Fast Track status by the FDA.

This stock is new to the public markets, having held its IPO in November of this year. The shares started trading on November 3, priced at $11 per share, and opened at $9.50. After nearly a month of trading, these shares are currently up by 24% from their first day’s closing price, and the company raised approximately $100 million in gross proceeds from the offering.

For JPM’s Tessa Romero, this biotech offers the advantage of a sound research program with achievable targets; she writes, “We see Lexeo’s platform of gene therapy candidates offering a differentiated approach to genetic diseases with limited treatment options and significant unmet need. The company’s lead cardiac therapeutic candidate LX2006, an AAV-based gene therapy is being investigated for the treatment of Friedreich’s ataxia (FA) cardiomyopathy for which there remains an unmet need for curative therapies that prevent disease progression and address the non-neurological components of the disease. Lexeo is also evaluating additional cardiac candidates, including LX2020 – an AAV-based gene therapy being investigated in PKP2-ACM – to enter the clinic next year.”

Looking ahead, Romero lays out some clear reasons for investors to buy into this stock: “Net-net, with continued de-risking of the candidates/approach expected over the next ~6-12 months, and with its market cap in the ~$250-300M range, we see the potential for upside to LXEO’s current valuation.”

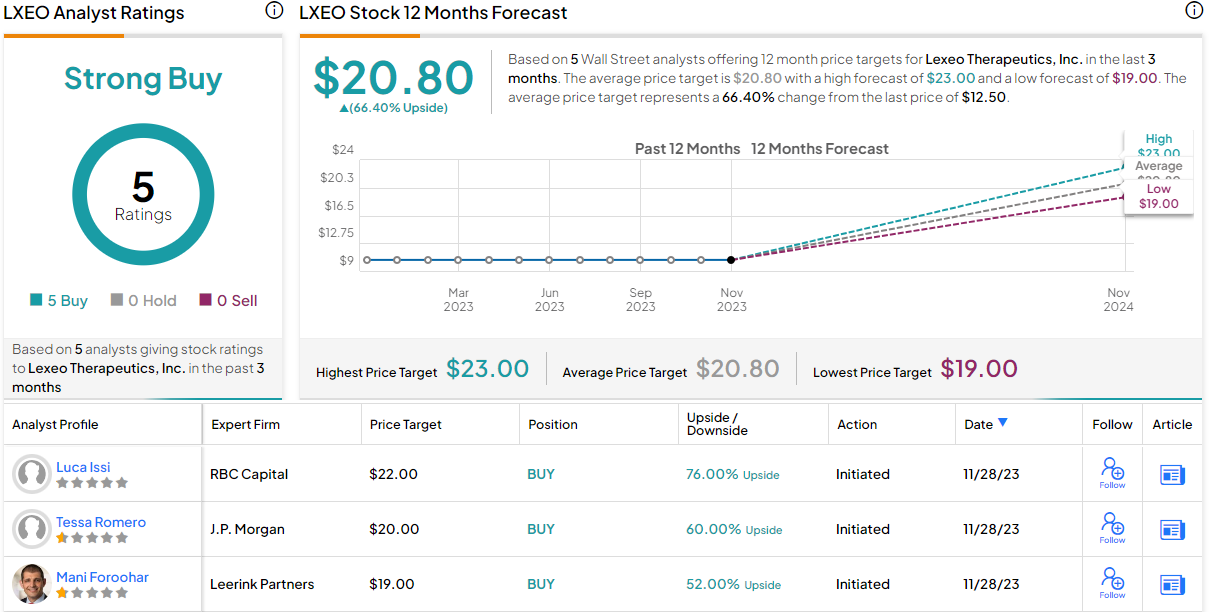

Taken together, these comments support Romero’s initiation of coverage with an Overweight (Buy) rating, while her $20 price target points toward a one-year upside potential of 60%. (To watch Romero’s track record, click here.)

Lexeo may be a new stock on the market, but it already has a Strong Buy consensus rating – based on 5 unanimously positive analyst reviews. The shares are trading for $12.50, and the average target price of $20.80 implies a 66% upside on the one-year horizon. (See Lexeo’s stock forecast.)

BioCryst Pharmaceuticals (BCRX)

The next stock on our list is BioCryst Pharmaceuticals, another biotech research company – but one that has managed to grab the brass ring. BioCryst has two approved drugs on the market, each with a solid patient base and revenue potential. The company, based in Durham, North Carolina, is currently focused on the treatment of rare diseases, although its first approved drug, rapivab, is an emergency-room influenza treatment.

Currently, the company’s chief focus is on the ongoing launch and commercialization activities for orladeyo, a treatment for hereditary angioedema (HAE). This is a potentially dangerous inherited disorder, characterized by accumulations of fluids in the patient’s body tissues, outside of the circulatory system, with attendant swelling that can become severe or even life-threatening. Orladeyo, which was first approved in late 2020, is a plasma kallikrein inhibitor designed as a preventative treatment for acute attacks of HAE in patients over the age of 12.

The drug is on the market in capsule form, and the company is working to expand its regulatory and commercialization efforts. BioCryst is investigating orladeyo in a late-stage clinical trial for pediatric patients between the ages of 2 and 12, and is pursuing regulatory approvals outside of the US.

Commercialization efforts this year have been successful, and BioCryst expects to bring in approximately $320 million in total product revenue from the drug. Q3 orladeyo product revenues reached $85.7 million, up almost 30% y/y. BioCryst estimates that it can achieve $1 billion in peak revenue from the drug.

A successful launch, especially one with billion-dollar potential, will always attract analyst attention – and in this case, the potential of orladeyo caught the eye of Jessica Fye. In her note on BioCryst for JPM, Fye outlines her expectations for near-term success, with a focus on the ongoing commercialization efforts: “Orladeyo, which has had a healthy launch, is on track to meet guidance of no less than $320mm in its third year on the market. We expect Orladeyo will continue to ramp and see net revenue growing >20% YoY to nearly $400mm in 2024. We also see longer term value driven by the company’s relatively early but broad pipeline, though we acknowledge it could take time and data for this to come into the stock. Big picture, with what we see as a sustainable financial footing and Orladeyo poised to continue to grow in the coming years, we see a nice entry point in the stock at current levels especially as the interesting, but early, pipeline unveiled during the company’s recent R&D event starts to show de-risking data.”

Fye’s stance fully supports her Overweight (Buy) rating here, and her $10 price target implies an upside, for the next 12 months, of 84%. (To watch Fye’s track record, click here.)

That JPM take is bullish – but Wall Street generally is even more so. The 10 recent reviews include 9 Buys to 1 Hold, for a Strong Buy consensus rating, and the stock has an average price target of $14.50 – suggesting a robust 167% gain from the current share price of $5.43. (See BioCryst’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.