Netflix stock (NASDAQ: NFLX) has rallied over 75% since its low in May. Many investors missed out on this opportunity as they had written Netflix off in their heads as an overvalued stock. To be fair, I felt the same way too. Well, in retrospect, Netflix indeed appeared quite cheap at just over $160. But, of course, in retrospect, everything appears to be quite clear.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The question that arises now, however, is whether Netflix stock is still worth buying following its extended rally, and that depends largely on what your desired margin of safety looks like. Because while Netflix shows strong profitability growth potential, I still find it hard to buy the stock at its current valuation multiples. I remain neutral on NFLX stock.

What Does Sustainable Profitability Mean for Netflix Stock?

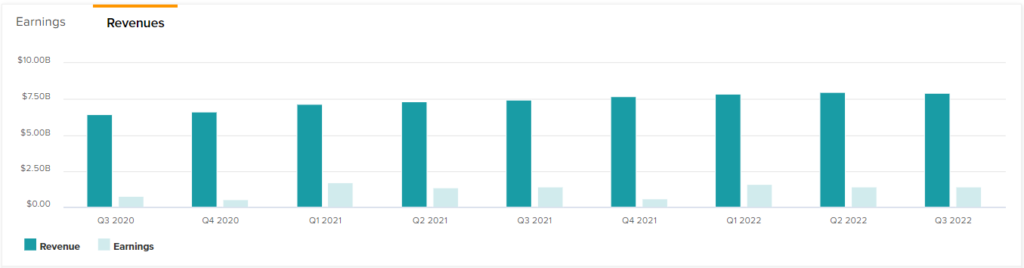

Netflix has firmly established that it can generate sustainable profits. This is important as it validates management’s prowess in the streaming space while allowing the company to gradually grow shareholder value.

See, everybody has wanted a piece of the streaming SVOD market over the past few years. Disney (NYSE: DIS), AT&T (NYSE: T), and Amazon (NASDAQ: AMZN) have been running their own services, namely Disney+, HBO Max, and Prime Video, saturating the industry. Yet, only Netflix has managed to grow profitably. Virtually all of its competitors are losing money.

Why? Because Netflix has bred the SVOD space. They know how to leverage their brand to maximize their return on investment with a lean CapEx structure. They know that the most successful shows are those that can impact millions of viewers by being culturally relevant and not necessarily by impressing audiences through expensive productions.

Take Amazon Prime’s Lord of The Rings: The Rings of Power series, for instance. The show is considered the most expensive television production in history, with the first season budget alone hovering close to $1 billion. Yet, fans of the franchise pretty much hated it. Now think of Netflix’s Squid Game, which reportedly cost the company just $21.4 million and went viral on a worldwide scale.

That’s not to say that Netflix doesn’t produce tasteless shows here and there, but they certainly understand that you can’t just buy your way into every living room on earth just because you have the cash to burn. This works for shareholders as well since it means that the company’s disciplined spending can actually result in shareholder value creation.

What are Netflix’s Earnings Growth Drivers?

Netflix’s major earnings growth drivers incorporate the company’s recently launched ad-supported model and improving economies of scale.

Netflix’s lower-priced ad-supported plan went live in 12 countries last month, just six months following its announcement. So far, subscription revenues have been Netflix’s only stream of cash flow. In future earnings reports, Netflix will be reporting revenues from two separate segments, with the other being its ad-related revenues. However, is Netflix’s ad-supported plan going to be accretive to earnings? I believe that it most certainly will, and here’s why.

Basically, Netflix will now begin producing supplemental revenues from a new user base, which, up until now, has refused to spend any money on the platform. The basic ads plan displays just ~5 minutes of ads per hour. Accordingly, viewers won’t be bombarded with irritating program breaks. At the same time, advertisers should find the platform to be a favorable habitat as they are able to deliver premium ad content that is based on useful user data. In turn, Netflix can charge above-average ad rates, therefore forming a new, highly-profitable segment. In other words, Netflix’s ad-supported plan is a win-win for all parties involved.

It’s important to emphasize here that Netflix will be showing shows from its current catalog. No material expenses will surface to fund the ad-supported model, and so a great chunk of its ad-related cash flows should end up in Netflix’s bottom line.

Is NFLX Stock a Buy, According to Analysts?

Despite Netflix stock’s rally, Wall Street analysts continue to be somewhat bullish on the stock. The stock has attracted a Moderate Buy consensus rating based on 15 Buys, 13 Holds, and three Sells assigned in the past three months. At $302.76, the average Netflix stock forecast implies just 5.6% upside potential.

The Takeaway

Netflix has come a long way over the past decade, and due to its first-mover advantage, management has mastered the route of profitable growth in the SVOD space. The company has started implementing ads in what appears to be the perfect moment. With its net subscriber additions likely to slow down in the coming years, the high-margin ad cash flows should be a fresh earning growth driver.

That said, are you willing to buy the stock at a forward P/E ratio of 28x, based on Fiscal 2022 estimates? Assuming ads help Netflix earnings in the double-digits moving forward, this may not be a crazy multiple considering the company’s ascertained moat in the industry. Nevertheless, buying Netflix today doesn’t seem like you are getting the stock at a decent discount, either.