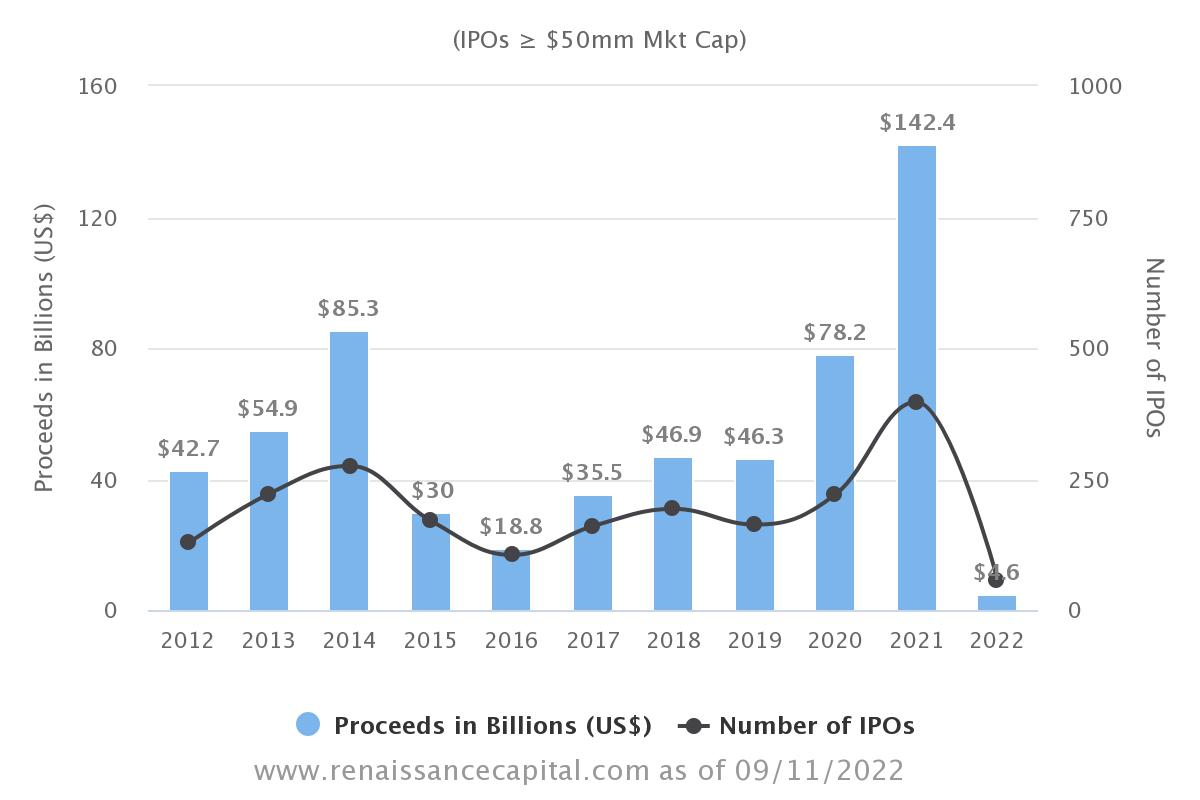

In the last few months, there has been a repeating theme in the headlines that mention “IPO drought.” According to Renaissance Capital, the number of U.S. IPOs is down 80% this year versus the same period in 2021. What’s more, the companies that went public in 2022 raised about 5% of the proceeds from the same date last year. Although forecasts speak of about 25 to 45 more IPOs to be carried out until year-end, 2022 is still expected to be the weakest in terms of IPO proceeds in more than 30 years.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

However, the decline in IPOs and numbers this year seem less striking, considering that 2021 was the busiest IPO year ever, by both the number of IPOs and the amounts raised.

Looking back, there’s no doubt that 2021’s IPO surge was nothing less than a bubble. With extraordinary liquidity sloshing around the markets following the Fed’s monetary easing in 2020, as well as with all the checks from the U.S. government, is it any wonder that much of this “free money” found its way into the stock market?

This year, IPOs have all but collapsed due to the economic downturn, the Fed’s tightening, and instability in the markets – but the heights they reached in 2021 make the downfall much more painful, bringing vivid reminiscence of the burst of the dot-com bubble. Also, it’s possible that a few years from now, we’ll talk about 2022 in terms of “the burst of the cash-injection bubble.”

The Four Most Dangerous Words in Investing: “This Time is Different”

Now, firms that were late to the party are paying the price as IPOs dry out. Companies are forced to either cancel their initial offerings or accept much lower valuations. On the other hand, many investors that bought the IPO buzz in 2020 and 2021 are now wishing they didn’t. The shoppers of these blockbuster IPOs are now saddled with big losses.

To tell the truth, the IPO bubble that has just burst in front of our eyes was long in the making; 2021 just took everything to extremes. In the 20th century and for a short while in the 21st, companies were expected to have a proven business model and show shrinking losses, if not profits, at their IPOs – but that expectation no longer exists.

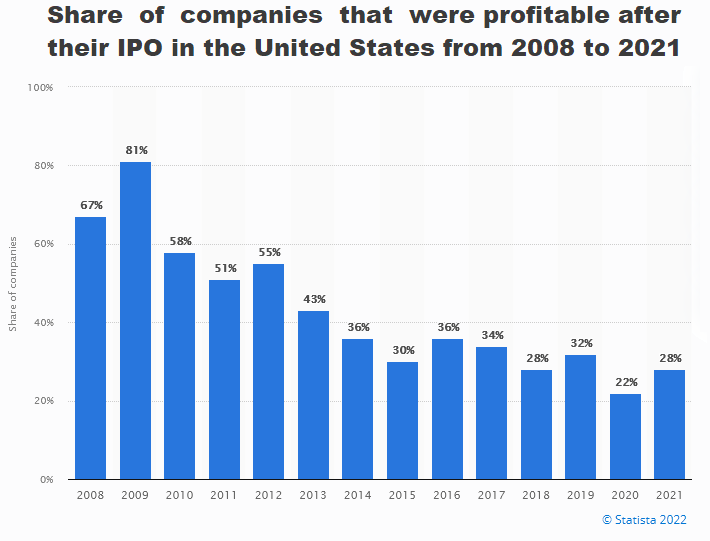

In the modern era, it’s perfectly normal for unprofitable companies to IPO based on their future earnings. However, the fact that the percentage of loss-making IPOs rose from 20% in 2009 to 70%-80% in 2020 and 2021 is somewhat unnerving. Even more disturbing is the colossal valuations at which unprofitable businesses go public.

Many money managers and analysts called for caution, in vain. “This time is different” used to be a warning, but in 2020, it became a common belief. The thinking was that unlike in 1999, this time, the tech companies going public do have great products and services that everyone uses; they aren’t just selling dreams. That might have been the case, but as we now see, the skyrocketing valuations at which these companies sold to the public were based on nothing but the low cost of capital, i.e., interest rates at zero.

Of course, investors should have been more careful; they shouldn’t have ditched common sense and should have looked into the companies’ fundamentals. However, most of the blame is on the preachers of the “this time is different” mantra. Countless articles, TV hosts, and financial pages informed investors that companies that go public these days are different from those in the past; and that investors should be patient with biotech or EV startups.

Investors were also told that “profitability is a choice” and that shareholders should sacrifice their current returns for aggressive expansion that will – someday – bring them huge profits.

The general public’s free money euphoria made retail investors easy prey for the professionals, who surely knew they were feeding the bubble with Main Street’s money. However, private investors’ greed was kindled by unrealistic promises of high future growth, enabling bankers and the companies going public to get even more greedy. At the end of the day, sky-high IPO valuations allowed everyone involved – the companies, the private investors, and the underwriting banks – to make much more money. It’s too bad that this money was made at the expense of private investors.

Case Study: Rivian Automotive’s IPO

Rivian (NASDAQ: RIVN), the world’s biggest initial public offering of last year and the sixth biggest in U.S. history, priced 153 million shares at $78 a share on November 9, 2021. After the listing, Rivian’s shares started trading to the general public at $106, giving the company a market value of more than $100 billion – more than the value of established automakers like General Motors (NYSE: GM) or Ford (NYSE: F). The shares even briefly climbed above $172 – and then declined and have done so ever since.

RIVN’s surge wasn’t backed by profits or even revenues, as the company had just started making sales and was having trouble keeping up with its production schedule. Why did investors agree to pay such a hefty price for a stock of a revenue-less company? In short, the answer is hype, fads, and easy money looking for a home.

EV companies have emerged as some of the hottest investments in the few years before the current sell-off. Together with other “green” themes, they were pushed to the public as the way to certain profits on the back of the climate agenda. Various Wall Street gurus preached a bright future for the “green” companies, leading many retail investors to believe that reading the companies’ financial reports is redundant. One of the biggest backers of Rivian at the time of its IPO was BlackRock (NYSE: BLK), now enmeshed in a scandal concerning another “green” theme, sustainable investing.

Now, RIVN trades at around $39, which means that investors who bought Rivian’s shares in the days after the IPO are saddled with large losses; those that gave in to the FOMO and bought at the top are now down almost 80%. To get back their losses, they’d need Rivian’s stock to rise over 360% from the current levels – which is, of course, possible but not really plausible.

The Biggest IPOs of 2020 and 2021: Where are They Now?

The biggest IPOs of 2020 included Airbnb (NASDAQ: ABNB), Snowflake (NYSE: SNOW), and others. Let’s have a quick look at their performance since then, concentrating on regular (non-SPAC) IPOs:

The 2020 IPO surge was just the beginning, as we now know. 2021 brought much more hype and out-of-this-world valuations. Many of these stocks started trading publicly at the high, losing value ever since, which hints that even at the time of their IPO, amid the bubble, investors realized that their share price was highly overvalued.

As a result, investors who bought into the 10 biggest IPOs of 2021 lost 43% of their money by now (average loss per stock). Meanwhile, those who were unwise enough to enter these stocks at their highs lost 65% on average:

It’s not something unheard of for a company going public to see a decline in their share prices after an IPO, however successful. Still, the sheer amount of losses and the huge percentage of losers in the 2021 IPO group tells us a lot about the psychotic state of the markets last year.

Of course, among 2020 and 2021 IPO graduates, there are companies with solid business models and a proven ability to generate revenues (if not profits). It’s just that when there’s a bubble, everyone gets sucked in. When the valuations are based on hype and greed instead of fundamentals and realistic assumptions, they reflect overblown growth expectations and lead to hefty losses.

The Near Future of IPOs Looks Much Bleaker

On top of stock market losses, this bubble burst will have long-lasting impacts on the IPO market and all the players involved. As the dot-com bubble burst burned a lot of investors and reduced the capital available for the IPOs in the following years, this time is not going to be different. In recent years, valuations have outrun the fundamentals by an outsized margin – and now it’s their time to run below the regression line in order to meet the laws of statistics (and common sense).

So, in the near future, companies that will have successful IPOs should be profitable and fairly large industry leaders. The “growth at all costs” era is over; it’s now “safety time.”