Undeniably, the once-vibrant and promising EV sector faces serious challenges. However, EV sector bulls who still want to participate in the possible opportunity may fare better with charging station operator EVgo (NASDAQ:EVGO). That’s because, thanks to its infrastructural focus, it doesn’t necessarily matter to the company which vehicle manufacturing brand wins out. However, it’s a tricky narrative. Therefore, I’m neutral on EVGO stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

EVGO’s Strong Q3 Performance

Fundamentally, stakeholders of EVGO stock aim for the broader integration of electric mobility platforms. In other words, they’re betting on the attendance stats of the big game rather than which team will win it. And that’s an enviable position to be in right now. With sector giant Tesla (NASDAQ:TSLA) posting disappointing results for the third quarter, that opened the door for EVgo to deliver. It took full advantage.

According to TipRanks reporter Kailas Salunkhe, the charging station operator rang up sales of $35.1 million, representing a leap of 234.3% against the year-ago quarter. Even better, analysts anticipated that the company would hit $29.8 million in revenue. On the bottom line, EVgo posted a loss of $0.09 per share. While obviously not the most ideal situation, this figure beat Wall Street’s consensus estimate by $0.11.

Further, Salunkhe pointed out that during Q3, “EVgo’s network throughput increased by 208% over the prior year to 37 gigawatt-hours. The company added more than 106,000 new customer accounts, taking the overall customer count to over 785,000.”

Additionally, the company had nearly 3,400 charging stalls in operation or under construction at the end of the quarter. Notably, EVgo’s PlugShare – a mobile and web application for charging station locations and information – now commands more than 4.1 million registered users.

To be sure, EV companies are at each other’s throats. For example, Tesla continues to introduce price cuts to its popular models, forcing other EV makers to respond. Subsequently, the price war has become one of attrition. It wouldn’t be surprising to hear about individual EV startup failures.

However, so long as consumers are buying EVs, infrastructure providers should theoretically benefit. That’s a major plus for EVGO stock.

Recurring Revenue Model is a Key Driver

Of course, the dilemma for individual EV brands is to convince consumers that their company is superior to the competition. While the rewards involved in dominating the field can be robust, so are the risks. Naturally, the broader automotive industry imposes a capital-intensive profile. However, every EV needs to “charge” up. In many ways, then, EVgo enjoys the easier pathway forward.

It comes down to the business model. EV manufacturers mostly depend on a transactional model; that is, sell a car to a customer and hope that the driver will come back in a few years’ time to buy another one. Do that at scale, and a company could be sitting pretty. However, with fierce competition in place, succeeding in the EV manufacturing space represents a tall order.

In contrast, EVgo and other infrastructure players depend on a recurring revenue model. Essentially, every EV will need to charge up to stay roadworthy. And with such a binary proposition – keep moving or stay stuck – infrastructure companies should enjoy predictable revenues.

After all, while consumers may spend days, weeks, and even months figuring out which car to buy, they don’t usually go through consternation about which infrastructure brand to use. Gas is gas or in the case of EVs, electrons are electrons.

Risky Business

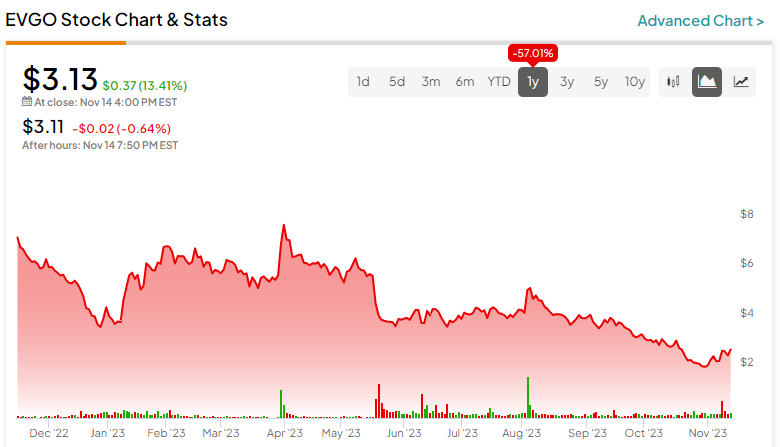

Nevertheless, EVGO stock isn’t devoid of risk. Even with the impressive Q3 performance, shares lost a worrying amount of value over the trailing 52-week period. As circumstances stand now, EVgo must climb a treacherous credibility wall.

On a broader view, while EV integration continues to march higher, a risk also exists regarding the low-hanging fruit theory. Stated differently, it’s possible that all EV brands have already converted willing high-income households into customers. Attracting the middle-income crowd will likely be a tougher task.

As I pointed out on October 16, not even high gasoline prices have lifted TSLA, even though elevated gas prices are a major catalyst for EV makers. As of this writing, this statement still rings true.

Is EVGO Stock a Buy, According to Analysts?

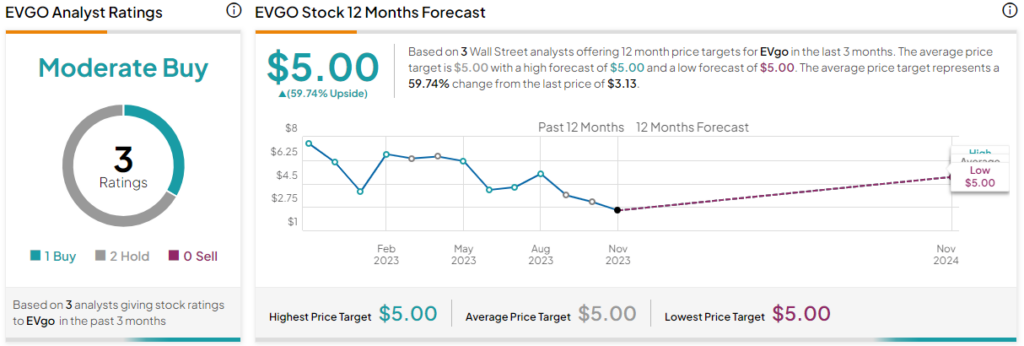

Turning to Wall Street, EVGO stock has a Moderate Buy consensus rating based on one Buy, two Holds, and zero Sell ratings. The average EVGO stock price target is $5.00, implying 59.7% upside potential.

The Takeaway: EVGO Stock Offers a Relatively Sensible Approach

Relatively speaking, EVGO stock offers a sensible approach to the EV opportunity. With individual brands engaged in a bitter price war, it’s difficult to determine who will win. However, everyone will need access to public charging infrastructure for full integration to become a reality. That benefits EVgo, but a caveat exists. It’s possible that the industry has already plucked the low-hanging fruit, presenting a risk for all players.