It’s safe to say now that stock investors are finishing 2023 in a pretty happy mood. We saw large gains in the markets, and even the late-summer swoon has been fully offset by November’s bullish turn, still in play six weeks later.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

At the start of this year, Bank of America set a year-end target for the S&P 500 at 4,600. The index has surpassed that, and BofA’s equity strategy team is predicting it will hit 5,000 by the end of next year.

Commenting on the markets, Savita Subramanian, the bank’s head of US equity strategy, writes, “The market has absorbed significant geopolitical shocks already and the good news is we’re talking about the bad news…. We’re bullish not because we expect the Fed to cut, but because of what the Fed has accomplished. Companies have adapted (as they are wont to do) to higher rates and inflation.”

The stock analysts at BofA are also gearing up for a solid 2024, and are busy picking out the stocks that they see as winners in the coming year. We’ve looked up some of their picks in the TipRanks databanks, to find out just why BofA is pounding the table on them. According to the data, the analyst consensus sees these 3 picks as Buy-rated, too. Here’s the scoop.

Don’t miss

- These 3 Biotech Stocks Have Strong Upside Potential, Says Deutsche Bank

- ‘Time to Hit Buy,’ Says Wells Fargo About These 2 Energy Stocks

- These 3 stocks are Cowen’s best ideas for 2024 including Amazon and Biogen

Wix.com (WIX)

The first stock on our list, Wix, is well-known among web developers, especially the do-it-yourself crowd. The company’s core product, that built its reputation and its initial audience, is a WYSIWYG (What-You-See-Is-What-You-Get) website design editor, purpose-built to make quality site building accessible to non-professionals – and even to those with limited or minimal knowledge of coding.

Wix got its start in 2006, and gained attention and built its customer base through use of the ‘freemium’ model, offering a base-level of services to all comers, free of charge, and making more advanced services and upgrades available for paying subscribers. Free services include design tutorials and site templates; more advanced services include business and e-commerce tools.

The cloud-based design platform has proved popular, and the company has expanded to a global footprint. Wix’s services are offered in 22 languages, and the company has offices and operations in 12 countries, including the US, Singapore, India, Germany, Canada, and Brazil.

In the third quarter of 2022, Wix met an important milestone – it reported its first quarter of profitable operations. The company has remained profitable since then, and in 3Q23, the last period reported, showed a non-GAAP income of $65.1 million, or $1.10 per share. The EPS was 39 cents per share better than had been anticipated. The company’s income was based on total revenues of $393.8 million, up almost 14% year-over-year and some $4.15 million ahead of the estimates. The third quarter also marked the third consecutive quarter of accelerating year-over-year revenue gains.

Of particular importance, Wix generated $62.8 million in free cash flow during Q3, or 16% of the total revenue. This marked a strong departure from the company’s historical pattern of burning cash.

Wix has caught the eye of Bank of America’s Mike McGovern, who appreciates the company’s turn toward profitability and its new-found cash flows. McGovern writes, “We like Wix’s underappreciated margin inflection story (mgmt. expects FCF margin to grow from just 4% in 2021 to 25% in 2025), as well as potential for new products to accelerate growth… We also like Wix’s AI strategy, making it less at-risk than some believe after the stock was included in AI-Risk buckets in early 2023 (alongside other website builders like SQSP). Wix has a suite of new offerings taking advantage of AI, making it more accessible to SMBs & individuals.”

This stance backs up McGovern’s Buy rating, and his $126 price target indicates potential for a 12% upside in the next 12 months. (To watch McGovern’s track record, click here)

The Bank of America take is far from the only upbeat view here; Wix has picked up 17 recent analyst reviews, barring one skeptic, all are positive, making for a Strong Buy consensus rating. The stock is selling for $112.35 and its $123.07 average target price implies a 9.5% one-year upside potential. (See WIX stock forecast)

Crocs (CROX)

The second stock on our list of BofA picks is Crocs, the footwear company that has built itself into an iconic brand in just 21 years of operations. Crocs gained its initial fame for its unique foam clogs, offered in a wide range of bright colors, that combined comfort, practicality, and ugly styling to create a combo that won over customers and fans alike. Today, Crocs has expanded its product lines to include flip flops, sandals, boots, and even comfortable work shoes. The company has even started marketing directly to healthcare workers, promoting a line of footwear designed for people who spend long days on their feet.

In 2022, Crocs acquired the Italian shoemaker HEYDUDE in a transaction worth $2.3 billion. HEYDUDE is known for its lines of lightweight, stylish footwear, offered at affordable prices – making it a good fit for Crocs. The acquisition was completed in February of last year.

By the numbers, Crocs has an impressive business. The company’s footwear – under both the Crocs and HEYDUDE brands – is available in 85 countries. The company sells approximately 100 million pairs of shoes every year, and can count on multi-billion-dollar annual revenue. Crocs has found a place for itself among the top athletic and leisure footwear brands in the world.

The company has been growing fast in recent years. Crocs saw $2.31 billion in revenue in 2021, for a 67% y/y increase. That revenue number was up to $3.55 billion in 2022, a y/y gain of 54%. The growth has continued this year although in a more muted fashion. In 3Q23, the top line came to $1.05 billion, up 6.6% from 3Q22 and $20 million ahead of the forecast. Crocs’ adjusted diluted EPS was up 9.4% y/y to reach $3.25, and came in 11 cents per share better than the estimates.

For BofA’s Christopher Nardone, the company’s solid record of growth is the key point. “The Crocs business has strong momentum having increased sales at a 25% CAGR since 2019 (sales +14% YTD),” Nardone said. “Some of this success has been obscured by the lackluster performance and market challenges facing the HEYDUDE (HD) brand, which we think is priced in. We expect continued strong sales at Crocs coupled with incremental progress at HD will lead to multiple expansion from depressed levels.”

Nardone complements his comments on Crocs by giving the stock a Buy rating – and by setting a $128 price target to suggest a one-year gain of 19.5%. (To watch Nardone’s track record, click here)

The 11 recent analyst reviews on CROX include 9 Buys to 2 Holds – giving the stock its Strong Buy consensus rating. CROX is selling for $107.11, and its average target price of $123.64 implies it will appreciate by more than 15.5% over the next year. (See CROX stock forecast)

Maravai Lifesciences (MRVI)

From the internet and shoes, will shift our focus to the healthcare industry. Maravai Lifesciences is an adjunct of the biopharmaceutical sector, with product lines designed to enable the research and development of new diagnostics, drug therapies, and vaccines. The company produces nucleic acid products, catalysts, and various reagents, and holds more than 1,500 patents for its branded technology portfolio.

The company boasts that its products have ‘set the standard’ in fields like enzyme development and biologics safety testing. Maravai has long been an important name in nucleotide research, and in the post-COVID research environment has been moving to expand into the mRNA field. The company’s products make it possible for the drug researchers to investigate and test infectious disease vaccines, cancer vaccines and treatments, cell therapies, and gene therapies, to avoid impurities and deliver pure therapeutic agents.

In recent quarters, however, Maravai has seen headwinds mounting. The company’s revenue has been falling y/y for the past several quarterly reporting periods. The company has initiated a cost-cutting plan, involving both layoffs and annualized cost reductions; this was announced after the 3Q23 report showed revenue down to $66.9 million, a decline of 65% y/y, a total that also missed Street expectations by $8.6 million. The company reported a net income loss of $15.1 million, or 5 cents per share, a figure that was 4 cents per share below the forecast.

Maravai attributed its recent sharp losses to a faster than expected drop in customer demand, as the pandemic fades into the background. Nevertheless, investor sentiment has been low, with the shares losing 54.5% of their value throughout the year.

BofA analyst Michael Ryskin acknowledges these problems facing Maravai, but adds his belief that the company is well-positioned to weather the storm and regain traction in the long term. He writes, “MRVI shares sold off in ’23 as pandemic related sales fell and biopharma spending slowed. MRVI is currently trading at ~20x BofAe FY24 non-COVID Adj EBITDA, which we see as an attractive valuation for investors and potential strategic acquirers. While near-term headwinds are likely to persist into 2024, we believe fundamentals will start to improve, cost actions will stabilize EBITDA, and valuation is compelling given the quality of the asset.”

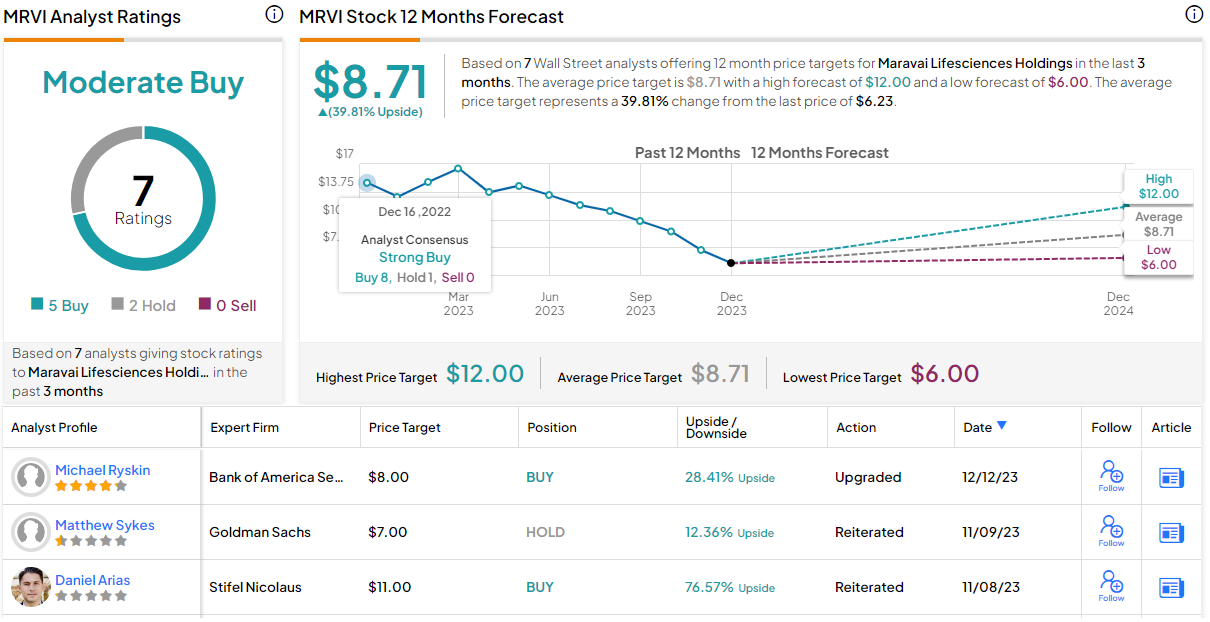

Quantifying his stance, Ryskin goes to rate MRVI as a Buy; he gives the stock a one-year price target of $8, to suggest a 28% gain. (To watch Ryskin’s track record, click here)

Turning now to the rest of the Street, where the stock gets a Moderate Buy consensus rating, based on 7 recent reviews that break down 5 to 2 in favor of Buys over Holds. The shares are priced at $6.23 and the $8.71 average price target points toward a gain of 40% on the one-year horizon. (See MRVI stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.