The Russian war in Ukraine is grinding on, and the hot war in the Middle East shows no signs of stopping. So, you would expect the price of oil to climb. But despite volatility in the energy sector this year, oil prices are down 11% year-to-date.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

In a note from investment bank Wells Fargo, top analyst Roger Read has cast his eye on the oil and natural gas markets, specifically on the energy stocks, and he sees room and reason for investors to buy.

Read, who is rated 5-stars by TipRanks, believes that wars or no wars, the oil and gas markets won’t see a spike in prices.

“We are constructive on global oil prices and expect the market to remain range-bound into 2024, reflecting our expectation of a balanced market. We expect E&Ps to benefit from modest oilfield service price deflation in 2024 with upside potential of further deflation if commodity prices undershoot our expectations,” Read opined.

Assuming support for the energy market, Read has also been picking out stocks that are set to gain next year. He is pointing out two energy stocks in particular, upgrading his stance and telling investors that it’s ‘time to hit buy.’ Let’s take a closer look.

Don’t miss

- These 3 stocks are Cowen’s best ideas for 2024 including Amazon and Biogen

- Goldman Sachs Says These 3 Healthcare Giants Look Very Attractive Right Now

- Time to Hit Buy on These 2 Building Stocks, Says Deutsche Bank

Coterra Energy (CTRA)

Operating out of Houston, Texas, the first Wells Fargo pick, Coterra Energy, is an oil and gas exploration and production firm working in its home state’s Permian Basin, in the Anadarko Basin of Oklahoma, and in the rich gas fields of the Marcellus Shale in the Pennsylvania Appalachians. The company has its hands in the best of both worlds, with solid assets in both oil and natural gas, creating a diversified portfolio capable of weathering economic headwinds.

That portfolio includes a total of 672,000 net acres across its operating areas. Of this, some 183,000 net acres are in the Marcellus shale. This production area is Coterra’s richest, generating 100% natural gas production and holding 1,498 MMboe in proven reserves as of the end of last year. In the oil regions of Texas and Oklahoma, Coterra holds 307,000 and 182,000 net acres, respectively, and has a combined total of 900 MMboe in proven reserves, in crude oil, natural gas, and natural gas liquids.

Last year, Coterra’s combined oil and gas production came to 2,470 Mboe/d. The lion’s share of that production, more than 2,200 Mboe/d, was natural gas from the Marcellus formation. This year, Coterra is on track to improve on those production numbers. The company’s 3Q23 output – the last quarter reported – came to 670 Mboe/d, well above the 655 Mboe/d figure that had formed the high end of the previously published guidance. This success was driven by strong performance in each of the company’s regions. Looking ahead, Coterra has published full-year 2023 production guidance in the range of 655 to 665 Mboe/d; this represents a 3% increase, at the mid-point, from the previously given full-year outlook.

Despite Coterra’s high output, the company’s revenues have declined from last year. In Q3, the top line reached $1.36 billion, representing a 46% decrease year-over-year. However, it is worth noting that this figure remains in-line with the forecasts. On the bottom line, reported as a non-GAAP adjusted EPS of 50 cents per share, there was a significant retreat from the $1.42 reported in 3Q22. Nevertheless, it did surpass the estimates by 7 cents per share.

Top analyst Read sees Coterra’s production increases – and its potential for more of the same – as the key point here. He writes of the company, “We are upgrading CTRA to Overweight from Equal Weight on relative valuation and strong momentum on oil production growth… Over the past 12 months, mgmt has deftly orchestrated a turnaround for the company. The company has been outpacing its production outlook for FY’23 and increased its production guidance for two consecutive quarters. Given continued operational efficiency gains and strong well performance, we would not be surprised if the company positively revises its 3- yr outlook in February.”

Along with his new Overweight (i.e. Buy) rating, Read give CTRA shares a price target of $30, implying a one-year upside potential of 19%. (To watch Read’s track record, click here)

Overall, Coterra Energy holds a Strong Buy consensus rating from Wall Street, based on 14 recent stock calls that include 11 Buys and 3 Holds. Coterra shares are trading for $25.13, and their $33.36 average price target suggests a one-year gain of nearly 33%. (See CTRA stock forecast)

Antero Resources (AR)

The second energy stock we’ll look at is Antero Resources, a hydrocarbon E&P company that focuses solely on natural gas. Antero has extensive holdings in the Marcellus and Utica shale formations of the Appalachian Mountain region and operates in West Virginia and Southeastern Ohio, in the valley of the upper Ohio River.

The company’s holdings and reserves are extensive, especially in its West Virginia Marcellus footprint. Antero has 440,000 net acres in this region and operates 1,200 producing horizontal wells in the area. Backing that up, the company has over 1,600 undeveloped core drilling locations in these holdings and can count on 17.8 trillion cubic feet of proven natural gas reserves. The company’s Ohio footprint is smaller; in the Utica Shale, Antero has 75,000 net acres that host 200-plus producing horizontal wells and some 250 undeveloped core drilling locations.

Antero’s overall production is impressive. Looking at last year’s numbers, the company’s wells brought to the surface the equivalent of 104 LNG tanker cargos. The bulk of this output was generated through hydraulic fracking techniques, which have made Antero one of the largest suppliers for the US liquefied natural gas (LNG) export market.

A look at Antero’s most recent quarterly production helps to tell the story. In 3Q23, the company averaged a net production total of 3.5 Bcfe/d, for a 9% y/y increase. This total included 2.3 Bcf/d of natural gas, up 4% from the prior year period, and 202 MBbl/d of natural gas liquids, up 18% year-over-year.

Following from this, the company’s revenue in 3Q23 came to $263.8 million, for a 14% y/y increase and beating the forecast by $2.77 million. The non-GAAP bottom line earnings per share were reported as 23 cents, 4 cents per share better than had been anticipated.

Wells Fargo’s Roger Read is upbeat on Antero due to the company’s sound, and increasing, production numbers. Read writes, “We discern positive rate of change in AR’s operational performance and capital efficiency. The company has increased its FY’23 production guidance for two consecutive quarters on strong well performance and improving operations. Mgmt continues to feel confident on 2024 capital efficiency trends with preliminary 2024 D&C capex expected to be at least 10% below 2023 levels, assuming holding production flat from H2’23 levels without baking in any cost deflation.”

For the company’s prospects over the next couple of years, Read sees a path toward positive reward and recommends that investors buy in now, saying, “Following a tough 2023, we see strong likelihood of mean-reversion in valuation of the stock given in-line 2024/25E EV/EBITDA multiples (5.1x/3.4x vs gas group median at 5.1x/3.4x) at WFS commodity price deck, but robust 2025 FCF yield (16.4% vs gas group median at 11.6%). Thus, we upgrade AR to Overweight from Equal Weight, as we see attractive risk-reward in the stock in 2024.”

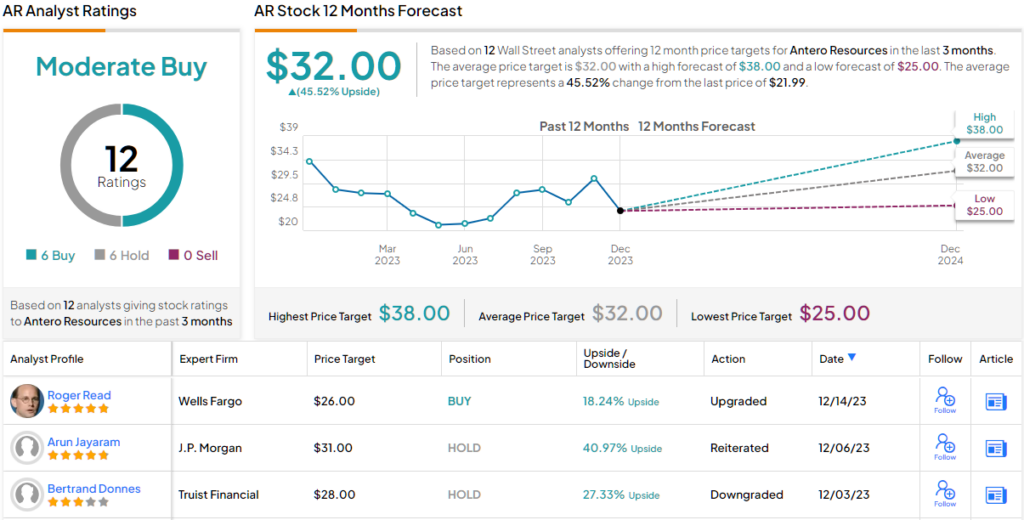

The 5-star analyst’s upgraded Overweight (i.e. Buy) rating on AR comes with a $26 price target that indicates potential for an 18% share appreciation over the next 12 months. (To watch Read’s track record, click here)

Overall, Antero has a Moderate Buy consensus rating from the Street’s analysts based on an even split in the 12 recent reviews, 6 to Buy and 6 to Hold. The stock’s current trading price is $21.99 and the average target price of $32 implies ~45% upside on the one-year time frame. (See Antero stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.