It’s only a few weeks to the New Year, so what better time to find out what stocks the major investment banks and research firms are recommending? TD Cowen, the New York-based multinational financial services firm, has been publishing the year-end stock calls from its analysts – and their choices make interesting reading.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

These are the ‘best ideas’ for 2024, from analysts with 5-star ratings from TipRanks; Cowen’s team has the experience and success to back up their recommendations, and investors can turn to them for valuable advice on the markets for these winter months.

The picks this year include equities from a variety of sectors – Big Tech, Big Pharma, consumer staples – with some prominent names such as Amazon and Biogen included on Cowen’s Best Ideas list.

So let’s take a closer look at these top picks. According to the latest TipRanks data, it’s clear that Wall Street agrees that these are stocks to Buy; each has a Strong Buy consensus rating from the Street’s analysts. Let’s dive in.

Don’t miss

- Goldman Sachs Says These 3 Healthcare Giants Look Very Attractive Right Now

- Time to Hit Buy on These 2 Building Stocks, Says Deutsche Bank

- These 2 MedTech Stocks Look Too Cheap to Ignore, Says Morgan Stanley

Amazon (AMZN)

First on our list is Amazon, the 800-pound gorilla in the world of e-commerce and online retail. Starting out back in the 90s as an online book seller, Amazon took a heavy hit when the dot.com bubble burst – but survived and has since expanded to become the world’s leader in online selling. Customers can find – almost literally – anything they want on Amazon: books, of course, but also computer gaming accessories, kitchen necessities, kids’ games, socks, electric shavers – the list will just grow more eclectic if we drag it out. Amazon moved a total of $693 billion in gross merchandise value last year.

But it’s not just online retail, of course. Amazon also has extensive operations in online services, such as subscription TV streaming and cloud computing, to home automation (Alexa, would you please…?), to audiobooks. Even groceries can be ordered online through Amazon’s services. The company’s website claims more than 2 billion visits every month, making it one the most-trafficked sites on the whole of the internet.

Business on this scale is sure to be reflected in the financial results, and so it is with Amazon. The company reported its 3Q23 results recently, and showed an impressive $143.1 billion in total revenues. That was up 13% year-over-year, and came in some $1.5 billion ahead of the forecasts. The gains in revenue rested on sound performance from the cloud computing segment, Amazon Web Services, which was up 12% for the quarter; from North American retail, which gained 11%; and mainly from international retail, which showed a y/y gain of 16%. Operating income rose to $11.2 billion vs. the $2.5 billion seen in the same period a year ago with the company delivering an operating margin of 7.8%, the highest since 1Q21’s record 8.2%.

Writing on Amazon for Cowen, 5-star analyst John Blackledge names the company as his top pick in large cap stocks, given the combination of record margins and high AWS growth. In Blackledge’s words, “AMZN is our top ‘24 large cap pick based on two key drivers, including (i) Record Op Inc Margins: We forecast AMZN ‘24 Op Inc of $58BN, 25% above cons, yielding 9.1% Op Inc margins, as high-margin AWS and Advertising businesses continue to scale while ‘rest of biz’ Op Inc turns positive after significant cost-cutting and easing inflationary & FX headwinds. We estimate ‘rest of biz’ ‘24 Op Income of ~$4BN following >$38BN in losses from ‘21-‘23E; (ii) AWS revenue growth accelerates: as AWS starts to lap cost optimizations, our public cloud survey work suggests 75% of customers will be through optimizations by end of ‘23. Also, AWS bookings are accelerating into 4Q23, which bodes well for next year & beyond.”

Looking ahead, Blackledge rates these shares as Outperform (Buy), and sets a $200 price target that points toward a one-year upside potential of 34%. (To watch Blackledge’s track record, click here)

Amazon hasn’t just picked up 42 recent analyst reviews in recent weeks – it has picked up 42 unanimously positive analyst reviews, to give the stock a Strong Buy consensus rating. The shares are trading currently for $148.84, and their $177.32 average target price implies a gain of 19 % in the next 12 months. (See Amazon stock forecast)

Biogen, Inc. (BIIB)

Next up is Biogen, a major name in the world of biopharmaceutical research. The company, based in Cambridge, Massachusetts, has an extensive product line of drugs and drug candidates either approved for, or under investigation for, the treatment of serious neurological diseases, most of which have ‘high unmet medical needs.’ Biogen has a world-wide footprint, with operations across the Americas, Europe, and Asia.

Biogen’s research pipeline currently features 21 separate tracks, ranging from early- to late-stage human clinical trial research. Of these research tracks, 5 are focused on potential treatments for Alzheimer’s and related dementia, and 4 are targeting Parkinson’s disease and similar movement disorders. Other research tracks focus on multiple sclerosis, ALS, lupus, and spinal muscular atrophy. Biogen is targeting ‘difficult-to-treat diseases,’ with the aim of developing transformational medicines – medicines capable of changing the way the medical field promotes public health.

In addition to its large research program and drug candidate lines, Biogen has a stable of approved medications already on the market and generating solid revenue for the company. Newly prominent among these are the recently launched Leqembi and Skyclarys, two new drugs with strong potential to boost Biogen’s bottom line significantly going forward.

Leqembi, a treatment for mild cognitive impairment or dementia due to Alzheimer’s disease, is administered via IV infusion and was approved for use earlier this year. Biogen realized approximately $2 million worth of in-market product revenue from Leqembi in 3Q23. The proven efficacy of the drug in clinical trials gives Biogen reason to hope that its ongoing commercial launch will bring the company to a leading position in the treatment of Alzheimer’s.

Skyclarys, the other recently launched mediation, is a treatment for Friedrich’s ataxia, or FA. It is the first – and so far, the only – FDA approved drug to treat FA in adult patients over age 16. Biogen did not develop Skyclarys itself, but it has acquired the drug through its recently completed acquisition of Reata Pharmaceuticals. Commercialization activities for Skyclarys are ongoing, and Biogen expects that the new drug will be ‘significantly accretive’ to earnings beginning in 2025.

As for earnings, Biogen has a steady income stream and is profitable – setting it apart from most research-oriented biotech firms. In 3Q23, Biogen had $2.53 billion in total revenues, in-line with the prior-year Q3 total, and $130 million above the forecast. The bottom line came to $4.36 per diluted share, by non-GAAP measures, beating the estimates by 37 cents per share.

For Phil Nadeau, another of Cowen’s 5-star stock analysts, this background makes Biogen the right choice as a ‘top pick’ in the large cap category. Nadeau acknowledges recent downbeat sentiment around the stock but is upbeat that the new drug launches can turn things around. He writes, “BIIB is a top large cap pick for 2024… Sentiment in BIIB is poor following 4 years of declining revenue. However, we expect that the launches of Leqembi and Skyclarys will return Biogen to growth in 2024 and drive a mid-single digit revenue CAGR for the next several years. We are optimistic that the reacceleration of Biogen’s top-line will reinvigorate sentiment…”

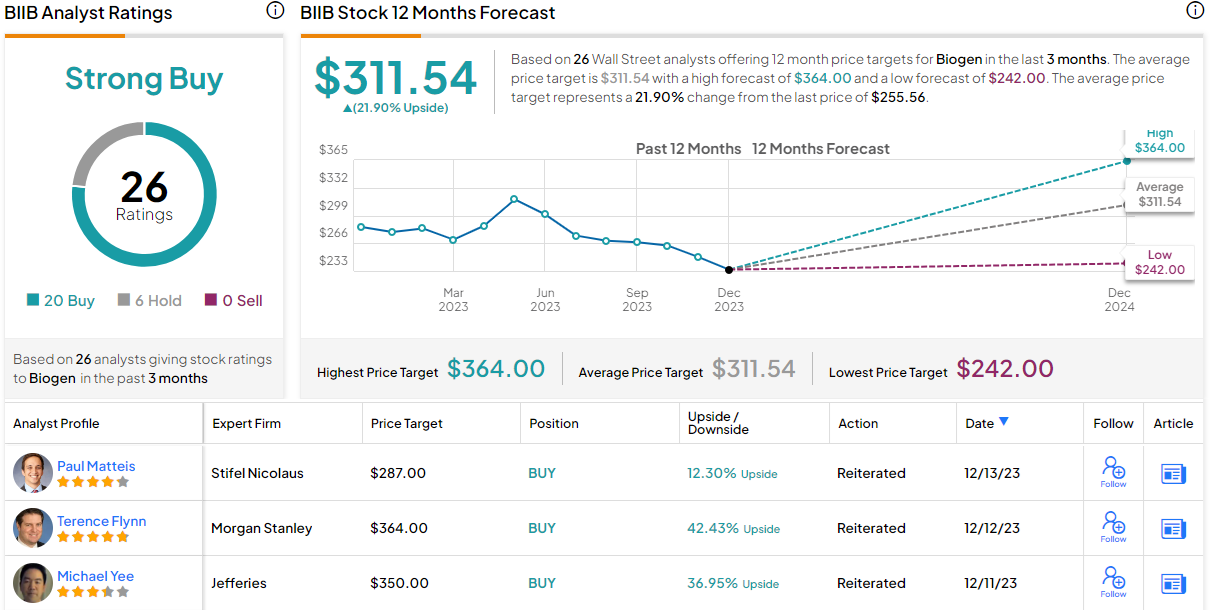

These comments support Nadeau’s Outperform (Buy) rating on the shares, while his $305 price target suggests that BIIB will gain 19% in the year ahead. (To watch Nadeau’s track record, click here)

The Strong Buy analyst consensus rating on BIIB is not unanimous – but it is based on 20 Buy ratings, against 6 to Hold. The shares are selling for $255.56, and their average price target is $311.54, slightly more bullish than the Cowen view and implying a 22% upside potential on the one-year horizon. (See Biogen stock forecast)

Constellation Brands (STZ)

Last up on our list of Cowen’s best ideas is Constellation Brands, a consumer staple and the largest beer importer in the United States. The company’s core business is the import of Mexican beer to the US market – Constellation owns the Modelo and Corona brands, which were the two best-selling import beers in the US last year. After Bud Light’s recent marketing implosion, Constellation picked up much of that slack with improved sales numbers for Modelo. In addition to its beers, Constellation boasts a strong portfolio of wine and spirits.

The company’s beer business is strong, and as noted, Constellation has successfully taken business from its competitor Bud Light, formerly the country’s best-selling beer. The Modelo brand, which saw the lion’s share of that take, saw solid gains this year, and in Constellation’s recent report for fiscal 2Q24, the Modelo brand family’s momentum drove the company’s beer business growth. The beer segment posted a 12% quarterly net sales increase, with Modelo Especial growing 9% and the Modelo Chelada brands posting a combined 40% growth. Constellation describes Modelo Especial as the ‘#1 brand share gainer’ in the US beer market, and the #1 selling brand by dollar sales.

On earnings, Constellation beat the forecast in its fiscal Q2. The company reported $2.84 billion at the top line, up almost 7% y/y and $20 million ahead of expectations. The bottom-line earnings figure, the non-GAAP EPS of $3.70, was 33 cents better than the forecast.

The stock has underperformed year-to-date, compared to the S&P 500, but its 8% ytd gain is still a net positive – and combines with the company’s modest dividend to give investors a sound return that beats inflation by a wide margin. The dividend was last paid on November 17 at a rate of 89 cents per common share. This annualized to $3.56 per share and gave a modest yield of 1.52%. The dividend return is supplemented by the company’s policy of supporting share value and returning profits to shareholders through buybacks; Constellation recently approved an additional $2 billion in share repurchases as part of its capital return policy.

All the above presents a picture of a company with a solid position in a strong market – and that’s the thesis behind Vivien Azer’s write-up of STZ for Cowen. The consumer staples expert is impressed by this company’s growth in the beer market, and says, “STZ is our Best Idea in 2024… We believe STZ is the best growth story in U.S. beer, while offering ancillary wine and spirits exposure through an evolving portfolio. The company’s robust capital returns are driven by industry-leading beer margins through an efficient portfolio of above premium Mexican import brands that have consolidated an average of 160 bps in monthly Nielsen dollar share over the last five years. Secular alcohol premiumization, outsized preference with younger LDA consumers, and demographic trends in Hispanic beer drinkers (who over-index to STZ’s brands) all serve as significant long-term tailwinds as growth from the Modelo brand family has re-accelerated share gains.”

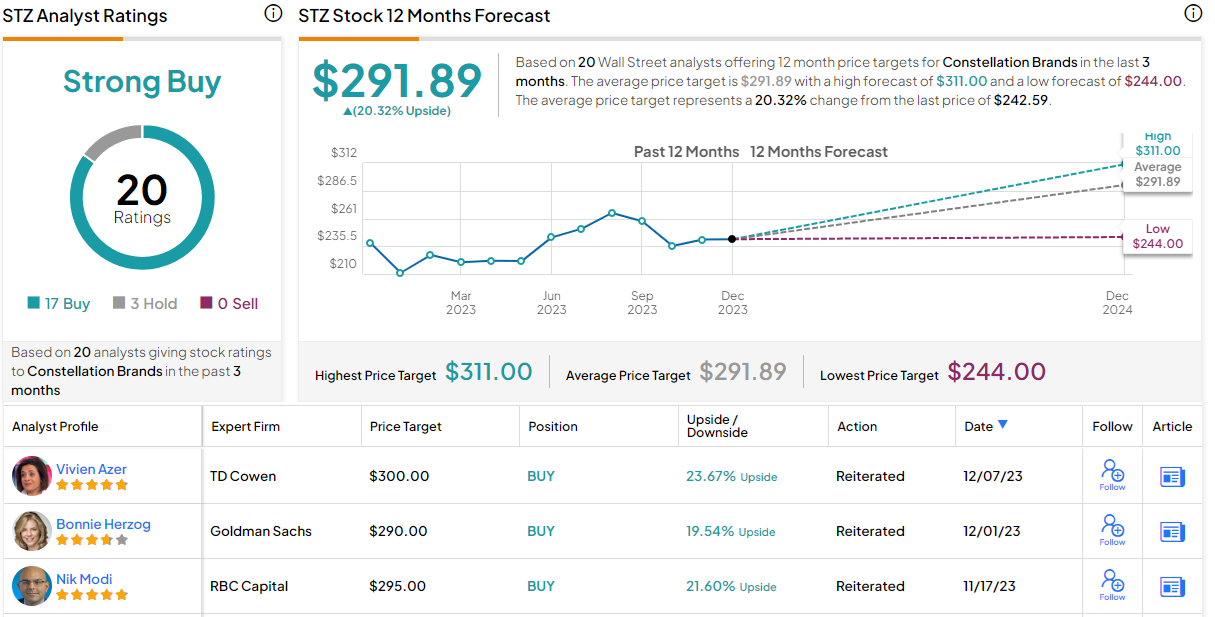

Accordingly, Azer gives STZ an Outperform (Buy) rating and her price target, set at $300, implies a one-year increase of 24%. (To watch Azer’s track record, click here)

There are 20 recent analyst reviews of this stock, and these include 17 to Buy and 3 to Hold – for a Strong Buy consensus rating. The average price target here is $291.89, suggesting a 12-month upside potential of 20% from the current $242.59 trading price. (See STZ stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.