With unemployment rising to 15%, and the grim corporate earnings seasons wrapping up, investors may struggle to keep up the relatively buoyant mood that has boosted markets in recent weeks. They may find some support from the Federal Reserve, where Chairman Jerome Powell this week urged Congress and the White House to agree on additional stimulus packages. The Fed has already cut rates down to 0 to 25 basis points; they have no further ammunition, so if more help is to come, it will need to come on the spending side. Urging action, Powell said that an economic recovery “could come more slowly than they would like.”

Confident Investing Starts Here:

- Quickly and easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

Viewing the situation for investment bank JPMorgan, quant strategist Dubravko Lakos-Bujas sees further aid as inevitable: “[This] crisis is a consequence of an exogenous shock, and is unique given the absence of ‘bad actors.’ This makes policy response much less contentious, more proactive and essentially unconstrained.” In his view, there is no ceiling on any action Congress or the Federal Reserve may take – and that may be the bottom line, as far as investors are concerned.

Turning to a micro-level view, the stock analysts at JPM are making some concrete recommendations – and they are targeting the dividend stocks. We’ve pulled three of JPM’s bullish calls, and ran them through TipRanks database to see what other Wall Street’s analysts have to say about them.

Annaly Capital Management, Inc. (NLY)

First up is a real estate investment trust, a niche well-known for its high dividends due to corporate tax code requirements. Annaly focuses its efforts on mortgage-backed securities, the lending side of the REIT sector, and holds an asset portfolio worth $133 billion.

Like most companies, Annaly saw a sharp earnings drop in the first quarter. EPS, at 21 cents, was down 19% sequentially, although it did come in just over the 20-cent forecast. The true rough spot was that earnings did not fully cover the company’s Q1 dividend. At 25 cents quarterly, the dividend payment annualizes to $1 even and gives a fantastic yield of 16.9%. Annaly has a long history of maintaining reliable dividend payments, including adjusting the payout if needed to keep it viable. That the company did not make such an adjustment in Q1, despite a payout ratio of 119%, suggests that the company expects earnings to turn upwards in the near term.

NLY shares have underperformed in the current bear cycle, losing as much as 59% from peak to trough. Since bottoming out, the stock has regained 40% from its low point – but share prices remain mired in penny-stock territory.

Writing for JPM, 5-star analyst Richard Shane sees the low share price here as an opportunity. He writes, “We reiterate our preference for NLY’s large agency MBS portfolio, which consists predominately of specified collateral that performed well in the lower rate environment leading up to the pandemic. We continue to see upside to shares at current levels…”

Backing his optimistic stance on NLY, Shane gives the stock a Buy rating. His $8.50 price target implies a strong upside of 45% in the next 12 months. (To watch Shane’s track record, click here)

Overall, Wall Street is in cautious agreement with Shane on Annaly. Of 9 recently published stock reviews, the Buys outweigh the Holds 6 to 3. The stock’s current share price is low, at $5.86 even after gains in today’s session, and the average price target of $7.33 suggests room for 25% growth this year. (See Annaly stock analysis on TipRanks)

Blackstone Mortgage Trust (BXMT)

Sticking with REITs, we turn to Blackstone. This company invests mainly in original senior loans, backed by collateral, in the North American, European, and Australian markets. Blackstone’s real estate portfolio holds $161 billion in assets under management.

Like NLY above, Blackstone shares felt a hard hit when the market turned sour in Q1. From peak to trough, BXMT lost an eye-opening 68% of its share value. Even after gains in recent weeks, the stock is still down 46% from its high point in February – this is serious underperformance, as the S&P 500 is only down 15% from its peak.

Blackstone’s underperformance comes even as the company beat the earnings forecast in Q1. While EPS was down year-over-year, it did beat quarterly expectations by 5.4%, coming in at 58 cents. Revenues missed the forecast, but still came in at a solid $100.6 million.

For income investors BXMT offers a solid dividend payment that has been held steady – regardless of quarterly earnings – for the past three years. The 62-cent quarterly payment gives an annualized value of $2.48 and a yield of 11.7%. This is nearly 6x the average dividend yield among S&P listed companies, and an impressive return by any standard.

Richard Shane covers BXMT, too, and he is satisfied that the company can weather the coronavirus storm. Shane says of Blackstone, “BXMT remains a market leader best positioned to negotiate optimal terms with both financing counterparties and well-capitalized institutional borrowers… the overall impact of COVID-19 to quarterly earnings was minimal as all loans have paid interest through April… BXMT noted approximately $821M in liquidity…”

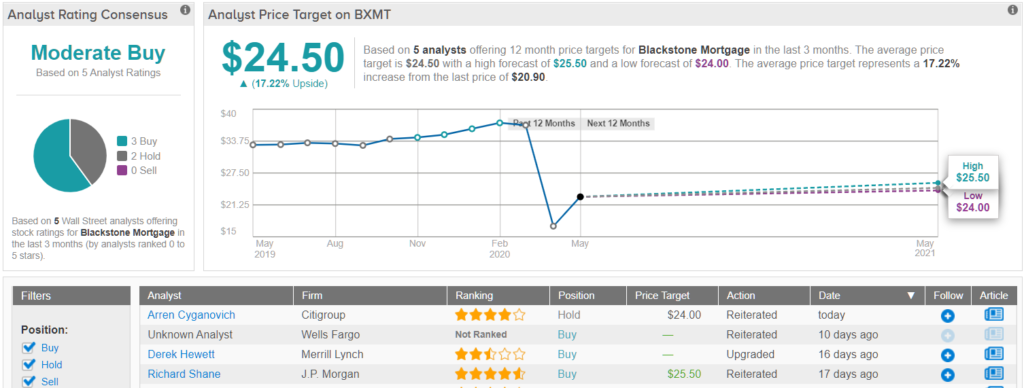

In his note on the stock, Shane reiterates his Buy rating, along with a $25.50 price target that suggests an upside potential of 22%. (To watch Shane’s track record, click here)

What do other analysts say about Blackstone? It’s almost split. TipRanks analytics shows out of 5 analyst, 3 are bullish on the stock, while 2 remain sidelined. The consensus price target of $24.50 shows a potential upside of 17.22%. (See Blackstone stock analysis on TipRanks)

Enbridge, Inc. (ENB)

Last up is Enbridge, a major player in the North American energy industry. While oil prices collapsed during Q1 as economies were shut down, that did not negate the need for oil and other hydrocarbons. Even limited economic activity, along with such essentials as home heating and power generation, maintained some demand. Enbridge, which is Canada’s largest natural gas distributor and the owner of the longest crude oil transport network in North America, was well positioned to remain profitable.

And it did. The company’s Q1 earnings came in at 62 cents per share, beating the forecast by 21.5% and showing impressive 34.7% sequential growth. Quarterly revenues, of $8.96 billion, beat the estimates by 5.2%.

Enbridge has an interesting dividend history. The company has kept up its quarterly payments reliably for the past three years, in part by adjusting the payout to match earnings. The current dividend, which was declared earlier this week, is 57.75 cents per share. The annualized payment of $2.31 puts the yield at 7.5%, not as high as the REITs above but still far better than average – and enormously higher than the badly depressed Treasury bond market.

JPM’s Jeremy Tonet believes Enbridge holds a strong business position. He writes of the company, “In addition to the strong results, we view reiterating guidance as a significant positive for ENB, especially considering Mainline concerns. Furthermore, ENB continues to progress several key initiatives, including Mainline recontracting…”

In line with this view, Tonet sets a price target of $56 Canadian ($39.86 US at current rates), implying a 29% upside potential for the coming year. Tonet’s bullish upside backs his Buy rating. (To watch Tonet’s track record, click here)

The analyst consensus view here is another Moderate Buy, based on 16 ratings that include 12 Buys, 3 Holds, and a single Sell. ENB shares are currently priced at US$30.98, and the average price target of $38.02 indicates a 23% upside potential. (See Enbridge stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.