Shares of Stamps.com plunged 11.5% on Nov. 6 despite the company beating analysts’ 3Q expectations and raising its full-year outlook.

Stamps.com (STMP), a provider of online postage and shipping software solutions, delivered 3Q revenue of $193.9 million, surpassing analysts’ estimate of $161.8 million. Moreover, revenue grew 42% year-over-year as the company is gaining from accelerating e-commerce demand amid the pandemic. The 3Q adjusted EPS jumped 242% year-over-year to $3.83 and crushed analysts’ forecast of $1.46.

Following the strong 3Q performance, Stamps.com now expects 2020 revenue between $705 million to $735 million compared to the previous guidance range of $650 million to $725 million. Also, it predicts adjusted EPS in the range of $10.35 to $11.35, up from the previous guidance of $6.25 to $9.25. (See STMP stock analysis on TipRanks)

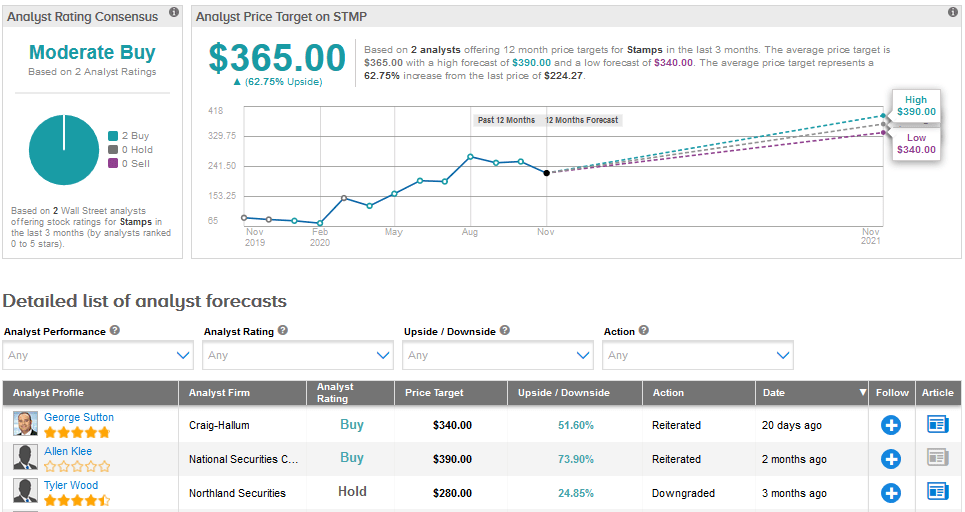

Shares of Stamps.com have surged a staggering 168.5% year-to-date and the average analyst price target of $365 indicates further upside potential of 62.8% in the coming months. The Street has a cautiously optimistic outlook on Stamps.com. Its Moderate Buy analyst consensus is based on two recent Buys.

Last month, Craig-Hallum analyst George Sutton reiterated a Buy rating for Stamps.com with a price target of $340 following positive comments from ShipStation CEO Nathan Jones (Stamps.com owns ShipStation) about its new integration targeting Alibaba’s over 10 million B2B sellers. Sutton added that ShipStation is a “strong contributor” to the company’s numbers.

The analyst noted “Jones made some key points regarding the significant current momentum, provided some revenue transparency regarding ShipStation in the consolidated results and makes it clear how embedded the Stamps.com properties are within the eCommerce ecosystem.” He added that Stamps.com is a no-brainer stock to own over the long term.

Related News:

Dropbox Shares Fall 5% Despite Beat and Raise Quarter

Glu Mobile Posts Record-Breaking Revenue; Shares Up 27%

Uber Posts Worse-Than-Feared Loss On Weak Rides Demand; Wedbush Raises PT