Uber Technologies posted a larger-than-expected loss in the third quarter, as the company’s core ride-hailing business continues to grapple with the Covid-19 impact, while demand for its food-delivery services is solid.

In the quarter ended Sept. 30, Uber (UBER) reported an adjusted EBITDA loss of $625 million, which is larger than analysts’ expectations of a $597 million loss. The company incurred a non-adjusted loss of $0.62 per share in the third quarter, compared with the $0.65 loss per share estimated by analysts. Total sales generated in the quarter amounted to $3.13 billion, falling short of analysts’ average estimate of $3.2 billion. Meanwhile, adjusted net revenue at Uber’s delivery unit, including Uber Eats, surged 190% to $1.14 billion.

In constant currency terms, mobility gross bookings, including rides, plunged 50% in the reported year-on-year, while delivery gross bookings exploded 135% during the same period.

“Despite an uneven pandemic response and broader economic uncertainty, our global scope, diversification, and the team’s tireless execution delivered steadily improving results, with total company Gross Bookings down just 6% year-on-year in September,” said Uber CEO Dara Khosrowshahi. “Mobility Gross Bookings nearly doubled from Q2 levels and Delivery surged again to 135% year-on-year growth thanks to an increasing pace of innovation, which saw us launch new industry-leading safety technology; extend delivery offerings into groceries and prescriptions; bring Uber Green to more than 50 cities; and expand both Uber Pass and Eats Pass membership plans.”

Furthermore, Uber CFO Nelson Chai said that the company remains confident that it can achieve quarterly adjusted EBITDA profitability before the end of 2021.

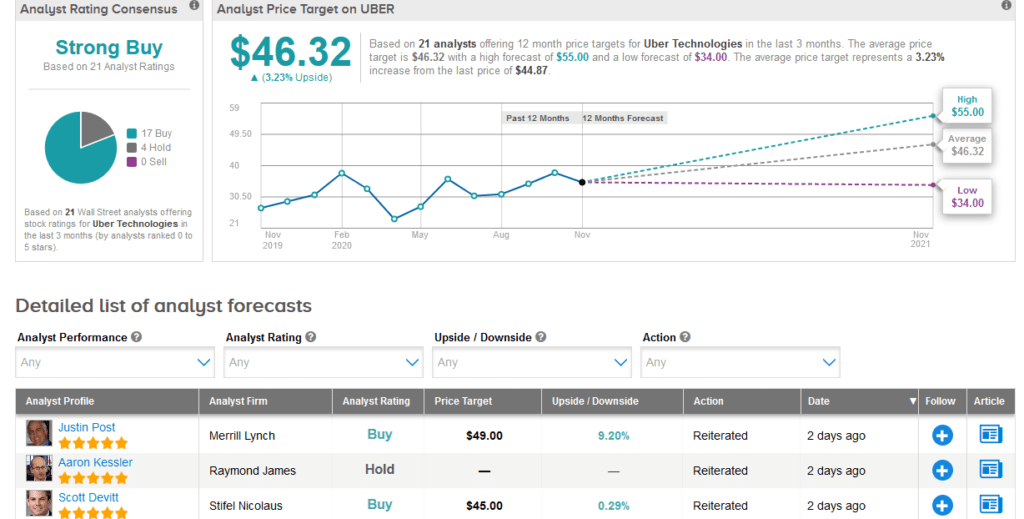

Shares in Uber rose 6.9% to $44.87 on Friday, taking this year’s advance to a stellar 51%. In the past few months, Uber has been focusing on ramping up its food delivery business to try to offset weak rides demand during the coronavirus pandemic. (See UBER stock analysis on TipRanks)

In reaction to the earnings results, Wedbush analyst Daniel Ives bumped up the stock’s price target to $49 from $41 and reiterated a Buy rating, commenting that Uber’s delivery business is growing faster than most competitors in the US and internationally.

“The pandemic continues to weigh heavily on the rideshare business with second wave fears abound across the US and Europe. The delivery business continues to be a major bright spot for Uber […] we expect to see continued strength on this front looking ahead into 2021,” Ives wrote in a note to investors. “Uber continues to expect to hit EBITDA profitability by the end of 2021 which remains a laser focus for the Street.”

The rest of the Street is mostly in line with Ives’ bullish outlook. The Strong Buy analyst consensus boasts 17 Buys vs. 4 Holds. The average price target of $46.32 implies upside potential of about 3.2% to current levels.

Related News:

Buffett’s Berkshire Operating Profit Sinks 32%, Buys Back $9B In Stock

CVS Gains 6% On Raised 2020 Profit Outlook; Analyst Says Hold

ViacomCBS Drops 6% As 3Q Profit Drops 17%; Needham Says Buy