In this piece, I evaluated two server stocks, Super Micro Computer (NASDAQ:SMCI) and Dell Technologies (NYSE:DELL), using TipRanks’ comparison tool to see which is the better stock. A closer look suggests a bearish view for Super Micro Computer and a bullish view for Dell Technologies.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Super Micro Computer manufactures servers and other computer products, with a focus on artificial intelligence (AI) applications. Meanwhile, Dell Technologies provides hardware and software solutions, including servers, workstations, desktop and notebook computers, and third-party software and peripherals.

Shares of Super Micro Computer plummeted on Friday, tumbling 20% in a single day, although that plunge wasn’t enough to erase its three-month jump, which currently stands at 171%. The stock is up 177% year-to-date and 794% over the last year.

Meanwhile, Dell Technologies stock is up 11% year-to-date and 15% over the last three months, resulting in a one-year gain of 106%.

With such a massive difference in these stocks’ performances, it’s no surprise that Super Micro Computer is trading at a much higher valuation than Dell Technologies. We’ll compare their price-to-earnings (P/E) multiples to gauge their valuations against each other and that of their industry.

For comparison, the U.S. tech hardware industry is trading around its three-year average P/E of 27.2.

Super Micro Computer (NASDAQ:SMCI)

At a P/E of 62.8, Super Micro Computer is trading at a sizable premium to its industry and to Dell Technologies after being caught up in the AI hype. While there is much to like about the company, it’s simply too expensive at current levels — given that what goes up usually comes back down. Thus, a bearish view seems appropriate for Super Micro Computer at this time.

To demonstrate just how frothy the market has gotten on Super Micro Computer stock in such a short time, its 52-week range is $85.61 to $1,077.87, with that record high having been hit last week. As such, it’s no wonder that insiders have been unloading their shares as the price has soared.

In fact, insiders were already dumping their shares three months ago at around $300 per share — before the surge that took the stock’s price above $1,000, albeit temporarily. Since then, there have been just a few Auto Sell transactions. It will be interesting to see what new data reveals on insider sales in the near future, given the wild action we’ve seen in this stock.

On the other hand, Super Micro Computer has demonstrated long-term staying power. Its stock price is up 4,084% over the last five years and 3,722% over the last 10, so when a more attractive entry price appears, it might be a good idea to scoop up some shares, especially considering the company’s positive earnings trends.

Super Micro Computer smashed earnings estimates in the last three quarters, with the most recent quarter coming in at $5.59 per share on $3.66 billion in revenue versus the consensus numbers of $5.16 per share on $2.97 billion in sales.

Of course, calling the bottom in this stock will be a challenge. However, the stock’s recent drop may be just the beginning of a near-term correction that could eventually present an attractive buy-the-dip opportunity.

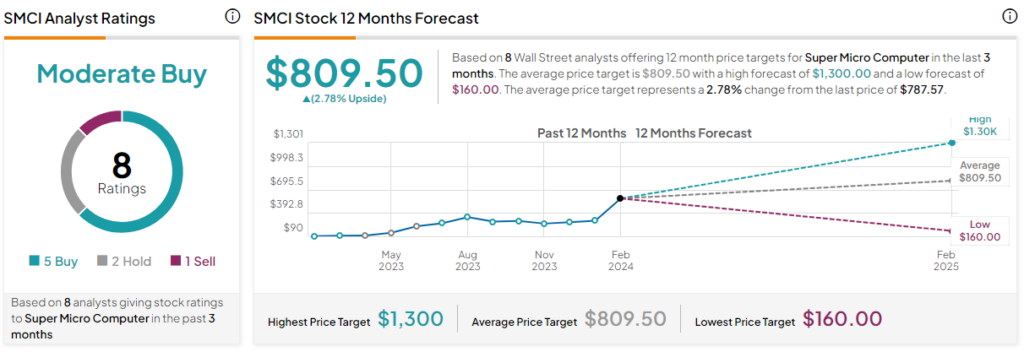

What Is the Price Target for SMCI Stock?

Super Micro Computer has a Moderate Buy consensus rating based on five Buys, two Holds, and zero Sell ratings assigned over the last three months. At $809.50, the average Super Micro Computer stock price target implies upside potential of 2.8%.

Dell Technologies (NYSE:DELL)

At a P/E of 23.3, Dell is trading at a small discount to its industry. Although the company does offer exposure to AI through some of its products, it hasn’t captured any of the AI-related hype. As a result, a long-term bullish view seems appropriate, especially considering Dell’s long-term share price gains.

At first glance, Dell displays robust earnings trends, smashing bottom-line estimates in the last several quarters, although it did miss the revenue consensus for the most recently completed quarter. The company posted $1.88 per share in earnings on $22.2 billion in sales versus expectations of $1.46 per share on $23 billion in revenue.

However, what’s most important for future upside in Dell is its AI exposure. A month ago, JPMorgan (NYSE:JPM) analysts highlighted Dell as one of three stocks likely to see significant upside from AI. In fact, the last quarter offered a small glimpse that backs up what JPMorgan highlighted.

Dell’s Infrastructure Solutions Group, which includes its servers and networking and storage hardware segments, all of which support AI, accounted for 28% of its sales in the last quarter. The division’s overall revenue also rose 9% quarter-over-quarter, so this is something worth watching in Dell’s upcoming earnings report for an update on its progress in AI.

Additionally, like most tech companies, Dell has had its ups and downs over the years, although it’s up 218% over the last five years. Thus, it’s likely worth buying and holding over the long term.

Finally, Dell Technologies is one of a relatively small number of tech companies that pays a dividend. Its current dividend yield is 1.76%, with a payout ratio of 21.99%. The payout ratio is the total annual dividend paid to shareholders relative to the company’s net income or earnings.

At 22%, Dell’s dividend appears quite safe while still allowing for R&D investments. Additionally, management expressed commitment to at least a 10% annual growth rate in the quarterly dividend through Fiscal 2028, sweetening the deal further for shareholders who invest for the long term.

What Is the Price Target for DELL Stock?

Dell Technologies has a Strong Buy consensus rating based on 11 Buys, one Hold, and one Sell rating assigned over the last three months. At $84.00, the average Dell Technologies stock price target implies upside potential of 1.9%.

Conclusion: Bearish on SMCI, Long-Term Bullish on DELL

Super Micro Computer is certainly not a bad company, but its valuation is simply too high. In fact, it’s so high that a plausible entry point doesn’t look possible any time soon, although it could be worth monitoring to see if or when it finally falls into the doldrums.

On the other hand, Dell Technologies hasn’t gotten the attention it deserves for its AI-related offerings. At its current valuation, the stock just looks too cheap to ignore.