Talk about tech, and what comes to mind first? Perhaps AI, perhaps digital networking, perhaps web access anywhere, anytime, through a pocket-sized device. We’ve gotten used to a seamless experience on the user side of the digital world.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

But for all of AI’s advances, or the increased capacity of new networks, digital tech still rests on the hardware behind it. Without the semiconductor chips, the server stacks, and the high-performance computers powering the cloud or miniaturized to fit in our smartphones, our digital universe would grind to a halt.

JPMorgan’s 5-star analyst Samik Chatterjee has taken the measure of this, particularly the way that advances in AI functionality and capabilities will require more advanced hardware. He sees this opening up plenty of opportunities for hardware- and AI-related tech, as AI-driven growth will likely provide a boost for IT hardware stocks in the coming year.

“Despite a cautious view on the sector in aggregate for 2024 on account of the elevated valuation multiples heading into 2024, the leverage to AI for certain sections of the broader Hardware coverage is likely to be a windfall moment with an opportunity for a re-rating on account of the incremental TAM opportunity around AI,” Chatterjee recently opined. “In particular the re-rating should be more impactful for IT Hardware where the maturity of the product markets has driven stagnant value multiples over the years with stock prices closely correlated to cyclicality of underlying customer spend.”

Chatterjee backs his general outlook with several stock recommendations; we’ve used the TipRanks platform to take a closer look at them, and found that Wall Street agrees that these equities are all ones to Buy. Let’s dive in.

Hewlett Packard Enterprise (HPE)

We’ll start with Hewlett Packard Enterprise, the global edge-to-cloud company that spun off from Hewlett-Packard in 2015, taking the parent company’s interests in servers, storage, and networking public as an independent entity – while keeping the cachet of the recognizable name. Today, HPE’s product lines provide solutions for edge-to-cloud computing, data collection and intelligence, data security, hybrid cloud activities – and AI technologies, using accumulated data to train and tune AI models.

In an important development earlier this month, on the AI side, HPE announced that it had entered into a definitive agreement for the acquisition of Juniper Networks. HPE will pay $40 per share to acquire Juniper, in an all-cash transaction with an equity value of approximately $14 billion. The Juniper acquisition will shift HPE’s AI-related portfolio toward higher margin networking business, with higher growth potential. The move is part of HPE’s continuing strategy to capitalize on trends in the AI world, particularly in the increased demand for secure and unified IT solutions for connecting, protecting, and analyzing edge-to-cloud data.

HPE’s close connection to AI has been a tremendous net benefit for the company in the past year, as the public profile of AI tech, especially generative AI, has significantly increased. HPE was able to leverage that to generate record-level performance in its fiscal year 2023, bringing in $29.1 billion in total annual revenue – for a 5.5% year-over-year gain. The company’s cash flow was substantial, too; at $2.2 billion, it was up $400 million y/y.

Zooming in, we can look at HPE’s last financial release, for fiscal 4Q23, and we’ll find that the overall solid annual performance covered up a pullback in the final quarter. The company’s quarterly top line came in at $7.4 billion, down 6.6% y/y and missing the forecast by $20 million. At the bottom line, the company’s non-GAAP EPS was listed as 52 cents, down from 57 cents one year prior – but 2 cents per share ahead of expectations. On an important note for future business, HPE reported a y/y increase of 37% in annual recurring revenue, to $1.3 billion in Q4.

Of particular interest to return-minded investors, HPE has maintained its capital-return program, and in fiscal 4Q23 sent $209 million back to shareholders, through both share buybacks and dividend payments. The company’s next dividend payment, for fiscal 1Q24, was declared at 13 cents per common share. This annualizes to 52 cents, and gives a yield of 3.16%.

For Chatterjee, the key point here is HPE’s solid connection to AI. He sees this as the driver for the company going forward, writing, “We rate shares of HP Enterprise Overweight led by our expectations for the company to be a key beneficiary of the AI driven server-compute investment cycle, which could not only provide further upside to our estimates, but also drive investors to attribute a higher target valuation multiple relative to the historical average on account of the leverage to the AI investments.”

Getting into specifics, Chatterjee adds, “We estimate AI-server revenue can track up to ~ $10 bn by 2027, accounting for ~30% of total revenue. Importantly, we estimate HP Enterprise’s AI revenue to translate into earnings of ~$0.65 by 2027 or represent ~25% of total earnings in the out-year.”’

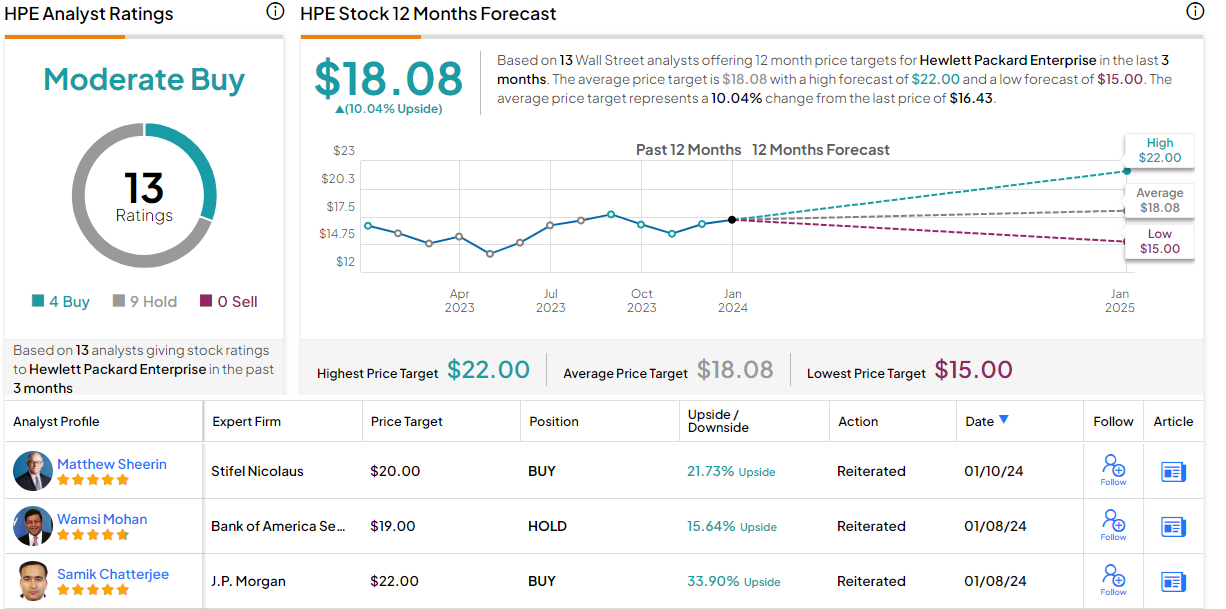

The top analyst’s Overweight (Buy) rating here comes with a price target of $22, suggesting a one-year upside potential of 34%. (To watch Chatterjee’s track record, click here)

This stock holds a Moderate Buy rating from the Wall Street analysts’ consensus, based on 13 recent reviews that break down to 4 Buys and 9 Holds. The shares are trading for $16.14 and their $18.08 average target price implies a gain of 12% in the next 12 months. (See HPE stock forecast)

Arista Networks (ANET)

Next on today’s list is Arista Networks, one of the pioneers in the field of software-driven cognitive cloud networking. This facet of cloud computing has the capacity to power large-scale data centers, enterprise campus environment, and high-end AI applications, putting this Silicon Valley tech firm at the epicenter of today’s high performance computing field. Arista offers its customers a platform that delivers results: in agility, analytics, automation, availability, and system security.

The firm’s product line is based on modularity, making it scalable for applications of all sizes. The company offers a variety of cloud network designs, to support server scales from 100 to 2,000, and on up to 100,000-plus. The layered construction of the server hardware permits both high capacity and redundant activities, necessary for operational efficiency in software-defined networking, large-scale data centers and cloud computing servers, and high-performance computing applications.

Arista’s hardware architecture has proven highly amenable to supporting AI. The company’s networked servers provide a solid foundation for the GPU and storage interconnects needed to drive AI and machine learning workloads. Arista also provides the IP/ethernet switches and the standardized transports needed to expand the hardware as the AI capabilities scale upwards.

On the company’s financial side, we find that Arista has posted solid growth over the past few years. The company’s revenues, earnings, and share price are all on upward trajectories; the share price has gained over 110% in the last 12 months.

The last financial report, for 3Q23, showed a top line of $1.51 billion, a total that was up 29% year-over-year and came in $30 million better than had been anticipated. The firm’s bottom line earnings, non-GAAP EPS of $1.83, was up 58 cents per share from 3Q22, and was 25 cents per share over the forecast.

Turning again to JPM’s Chatterjee, we find the analyst highly bullish on this company’s connection to AI. Chatterjee writes, “With Arista well-positioned to benefit from the adoption of Ethernet-based datacenter switches for AI, we estimate AI-related revenue can track up to ~$2 bn by 2027. Based on industry estimates, the aforementioned would equate to market share of ~30% relative to the Ethernet opportunity or ~18% relative to the total opportunity (includes InfiniBand), which compares to Arista’s current share of 30%+ in the highspeed datacenter switch market. Importantly, we estimate Arista’s AI revenue to translate into earnings of ~$2.25 by 2027 or account for 20%-30% of total earnings in the out-year.”

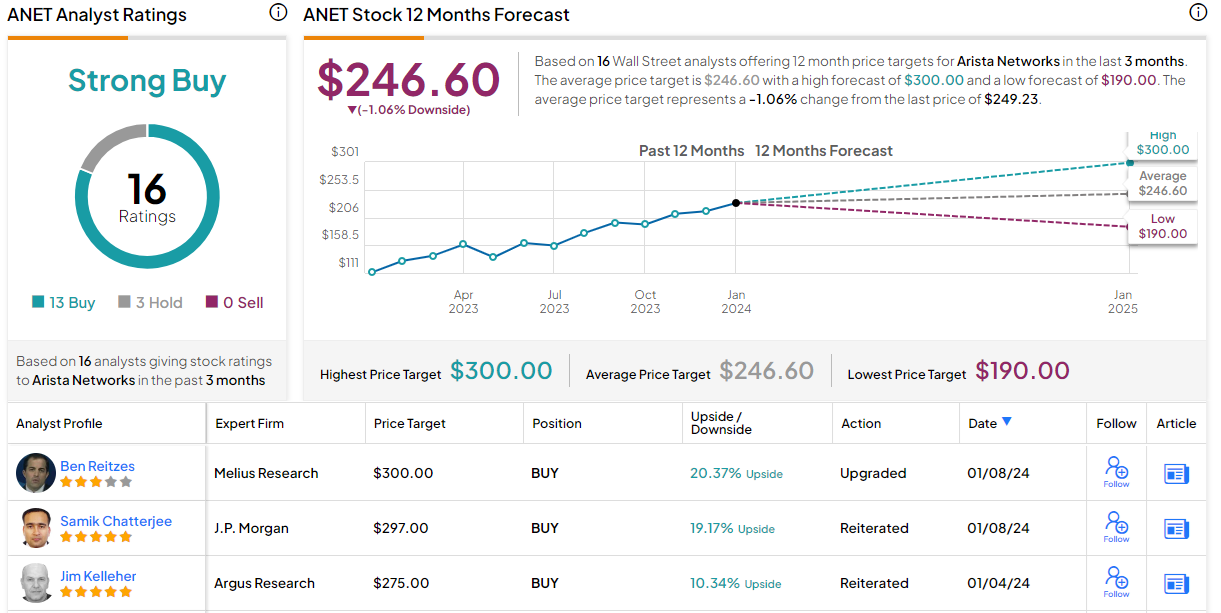

Looking ahead, Chatterjee gives Arista an Overweight (Buy) rating, and his $297 price target indicates room for a 19% gain on the one-year horizon.

The 16 recent analyst reviews on ANET shares include 13 Buys to 3 Holds, supporting a Strong Buy consensus rating. This stock is currently trading for $249.23, and the rapid gain in share price has pushed that value slightly above the $246.60 average price target, suggesting the shares will stay rangebound in the year ahead. (See Arista stock forecast)

Dell Technologies (DELL)

We’ll wrap up this list with Dell, a name most of us probably know from the personal computing world. Dell was founded back in the 80s and is still in the business of making computers. The company remains a leading supplier of laptops, PCs, and accessories such as monitors and gaming peripherals.

While general PC hardware remains at the core of Dell’s business, the company also has a large presence in the world of IT hardware. Dell’s Infrastructure Solutions Group, which covers its networking, server, and storage hardware segments – all essential in building out AI systems, data centers, and high-performance computing architecture – generated 38% of the company’s revenue in its last reported quarter.

Looking at those last reported quarterly results, we find a mixed showing. Dell brought in $22.3 billion in revenue for its fiscal 3Q24. This was down by 10% y/y, and it missed the forecast by $600 million. However, bottom line earnings, at $1.88 per diluted share in non-GAAP measures, were profitable – and were 42 cents per share ahead of the estimates. In a note of particular importance for investors interested in AI hardware, Dell’s server and networking revenue saw a strong boost in the last financial release, powered by AI-optimized servers. The segment brought in $4.7 billion in revenue, up 9% from the previous quarter.

Checking in one last time with JPM’s Chatterjee, we find him again upbeat, citing Dell’s hardware connection to AI as a reason for investors to buy in. Chatterjee says, “Dell is uniquely positioned to benefit from the adoption of AI-based hardware in both datacenter infrastructure as well as end-point devices given its portfolio encompassing servers, storage appliances and PCs. We estimate AI-server and AI-PC revenue can track up to ~$15 bn and ~$19 bn by 2027, respectively, which in aggregate would account for ~30% of total revenue. More importantly, we estimate the AI opportunity for servers and PCs would account for ~$2.55 and ~$1.55 of earnings, respectively, or represent almost ~50% of total earnings in aggregate in the period.”

These comments support the analyst’s Overweight (Buy) rating, and his $90 price target implies a 15% potential upside on the one-year time frame. (To watch Chatterjee’s track record, click here)

Wall Street clearly agrees with the bulls here, as the 12 recent analyst reviews have a lopsided 11 to 1 split favoring Buy over Hold – for a Strong Buy consensus rating. Shares are trading for $78.25 and their $85.08 average target suggests an upside potential of 9% for the coming year. (See DELL stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.