Elastic (ESTC), a provider of open source search and analytics engine services, reported a smaller-than-expected Q4 loss backed by continued demand for the company’s enterprise search solutions. Shares jumped 12.8% in the extended trading session on June 2.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The company reported an adjusted quarterly loss of $0.08 per share, lower than the Street’s estimated loss of $0.16 per share. In the prior-year quarter, the company had a loss of $0.12 per share.

Revenue for the quarter was up 44% year-over-year to $177.61 million, versus the Street’s estimates of $157.94 million. SaaS (Software-as- a- Service) revenue grew 77% to $51.3 million, while calculated billings were up 38% to $240.9 million. Additionally, deferred revenue came in at $397.7 million, up 53%. (See Elastic stock analysis on TipRanks)

At quarter-end, the total subscription customer count grew to over 15,000, while the total customer count with Annual Contract Value (ACV) of more than $100,000 exceeded 730.

On an annual basis, revenue was up 42% to $608.5 million, including SaaS revenue growth of 80%. For Fiscal 2021, the company reported an adjusted loss of $0.09 per share, lower than the prior-year loss of $0.93 per share.

Shay Banon, founder and CEO of the company said, “Data volumes keep increasing as companies become more digital and move to the cloud, and our customers are seeing that the ability to search, observe, and protect this ever-increasing amount of data is critical to their success. We believe this continued demand puts us on the path to becoming a $1 billion plus revenue company in fiscal year 2023.”

For fiscal Q1, the company forecasts revenue to fall in the range of $171 million to $173 million, compared to the Street’s estimates of $168.8 million. The company expects a loss in the range of $0.13 – $0.10 per share, versus a loss of $0.12 per share estimated by analysts.

Elastic projects FY22 revenue to be in the range of $782 to $788 million and an annual adjusted loss in the range of $0.60 – $0.51 per share. The Street estimates annual revenues of $743.3 million and a loss of $0.48 per share.

Following the results, Robert W. Baird analyst Jonathan Ruykhaver lowered the price target on the stock to $145 (22.9% upside potential) from $155 while maintaining a Hold rating.

Ruykhaver said, “Overall, we continue to appreciate Elastic’s ability to innovate, and we are encouraged by the accelerating trends in large customer growth.”

Consensus among analysts is a Strong Buy based on 9 unanimous Buys. The average analyst price target stands at $173.63 and implies upside potential of 47.1% to current levels. Shares have gained 32.2% over the past year.

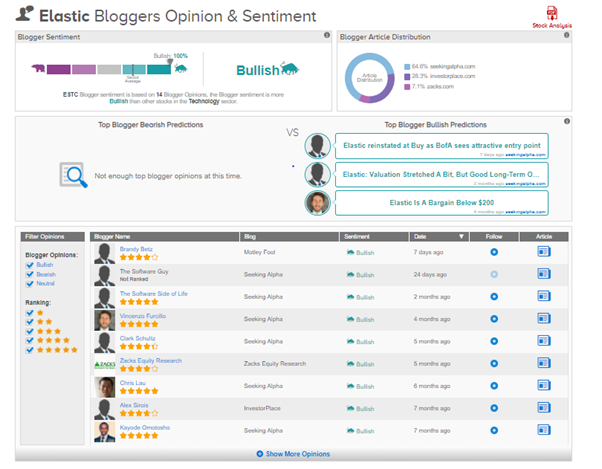

TipRanks data shows that financial blogger opinions are 100% Bullish on ESTC, compared to a sector average of 70%.

Related News:

Zoom Q1 Earnings & Revenue Outperform; Raises FY22 Guidance

Iteris Reports Q4 Loss, Beats Revenue Expectations

Old National and First Midwest Ink All-Stock Merger Deal