Dunkin’ Brands Group confirmed on Friday that it will be snapped up by Inspire Brands in an all-cash deal valued at about $8.8 billion.

Under the terms of the merger agreement, Inspire Brands will commence a tender offer to acquire all of the outstanding shares of Dunkin’ Brands (DNKN) for $106.50 per share to take the company private. The deal terms represent a premium of approximately 30% to Dunkin’ Brands’ 30-day volume-weighted average price and a premium of about 20% per share to its closing stock price on Oct. 23. DNKN shares closed 1.4% lower at $99.71 on Friday. The total transaction consideration amounts to $11.3 billion including the assumption of Dunkin’ Brands’ debt.

The merger will bring together Inspire’s more than 11,000 Arby’s, Buffalo Wild Wings, SONIC Drive-In, and Jimmy John’s restaurants worldwide with Dunkin’ Donuts and Baskin-Robbins chains. Inspire generates $15 billion in annual systemwide sales. Following the completion of the transaction, Dunkin’ and Baskin-Robbins will be operated as distinct brands within Inspire.

“During the global pandemic, we have stood tall. We’ve had each other’s backs and are now stronger than ever,” said Dunkin’ Brands CEO Dave Hoffmann. “We are excited to bring meaningful value to shareholders who have been with us on this journey and believe that Inspire Brands, a preeminent operator of franchised restaurant concepts, will continue to drive growth for our franchisees while remaining true to all that is unique and special about the Dunkin’ and Baskin-Robbins brands.”

The transaction is expected to close by the end of 2020. In the run-up to the deal, which was reported by The New York Times last week, DNKN shares surged 12% over the past 5 days, taking their year-to-date gain to 32%. (See Dunkin’ stock analysis on TipRanks)

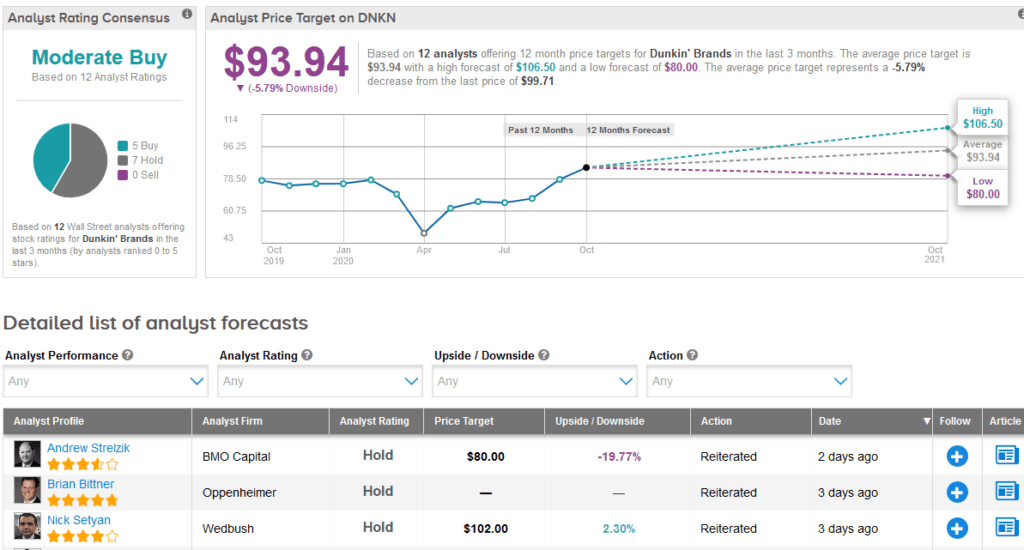

BMO Capital analyst Andrew Strelzik last week raised the stock’s price target to $80 from $66, after the company’s Q3 results beat the Street consensus thanks to better-than-expected comparable sales, franchise fees, and operating margins, as well as modest tax favorability,

However, Strelzik stuck to a Hold rating saying that the timing of recovery from Covid-19 remains uncertain, and the fundamentals will continue to matter less to shares “as long as M&A speculation persists”.

Overall, Wall Street analysts are cautiously optimistic about the stock. The Moderate Buy analyst consensus splits into 5 Buys versus 7 Holds. Meanwhile, the analyst average price target stands at $93.94, indicating 5.8% downside potential lies ahead following the recent rally.

Related News:

Alphabet Rises 6.5% On Robust 3Q Results; Street Sticks To Buy

Pinterest’s Blowout 3Q Sends Shares Up 32%

eBay Slips 4% As Online Goods Growth Volume Slows