New technologies bring with them new demands on security, and we’ve all learned the vocabulary of the digital world’s risks: spyware and malware, malignant ads and phishing, hacking and ransomware. It seems the threats are never-ending.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The increase in malevolent software attacks has driven a related increase in regulatory requirements, that is helping to push increased cybersecurity spending by both public and private businesses. A run of recent, high-profile, cyberattacks has simply driven that point home.

The upshot is, companies everywhere are working to firm up their cybersecurity defenses, to satisfy regulators, to reassure customers, and to prevent the losses consequent to a major hack attack. In a 2023 report on the Cost of Data Breach, IBM estimated that the “global average cost of a data breach in 2023 was $4.45 million.” That’s a serious incentive for companies to bump up cybersecurity spending – and it’s a serious tailwind for cybersecurity stocks.

This fact has caught the eye of Shyam Patil, 5-star analyst from Susquehanna, who writes in a recent industry report, “We are bullish on the cybersecurity software space as we see cyber budgets and use cases continuing to grow, driven by an ever-evolving threat landscape, internal and external innovation, and requirements from both regulators and insurers. Additionally, we expect consolidation to remain a key theme, as we continue to see a move toward platformization and increasing desire among enterprise customers to combat vendor sprawl. That said, we see the rapidly changing nature of the marketplace and threat landscape continuing to lead to new entrants.”

Patil also has an idea which cybersecurity stocks represent the best opportunities right now and we have decided to give three of his picks a closer look. For a more rounded view of their prospects, we also ran them through the TipRanks database. Here’s the lowdown.

Don’t miss

- Jefferies Says Solar Stocks Offer a Positive Risk-Reward — Here Are 2 Names to Take Advantage

- Bank of America Pounds the Table on These 3 Buy-Rated Stocks

- These 3 Biotech Stocks Have Strong Upside Potential, Says Deutsche Bank

Palo Alto Networks (PANW)

First up is Palo Alto Networks, a digital security company offering comprehensive cybersecurity solutions and a line of firewall products, all designed to create a safe and secure environment in cloud, network, and endpoint services. Palo Alto’s product lines offer a high level of protection for online and cloud-native systems, protection that can be tailored for enterprise customers, small businesses, and even for individual home use. The company’s security products are offered on the popular software-as-a-service subscription model.

Some numbers will give an idea of the scale – and importance – of Palo Alto’s work. The company’s December 19 daily data showed a total of 1 trillion cloud events processed. This included 1.44 billion new unique objects analyzed, 4.53 million new unique attacks objects identified, and 324,920 malware executions blocked, and 9,610 exploit attempts detected. Overall, the company’s defenses counted 7.05 billion attacks prevented inline.

From the user’s perspective, Palo Alto’s security systems allow any cloud system to be secured, and allow security operations to be automated for maximum efficiency in detection, investigation, and response. Palo Alto boasts that no matter what the security challenge is, it can be conquered, even the latest threats, based on AI and machine learning technologies.

In November, Palo Alto Networks reported its financial results for fiscal 1Q24 (October quarter). Revenue was up almost 22% year-over-year, reaching $1.9 billion – a total that beat the forecast by $60 million. The company’s backlog, listed as the remaining performance obligation, bodes well for the near-term; it came in at $10.4 billion for the quarter, up 26% year-over-year. At the bottom line, Palo Alto brought in a non-GAAP net income of $1.38 per diluted share, up from the 83-cent figure of the prior-year quarter and $0.22 above the consensus estimate.

In his coverage of this stock, Shyam Patil, takes an overall upbeat view, writing, “PANW’s category-leading positioning in network and cloud security underpins our Positive view on the company. We see PANW as one of the key beneficiaries of consolidation and platformization in the space, with several checks highlighting the ease of the company’s products. We acknowledge the company is trading at a premium but see this as well-deserved given the premium nature of the asset.”

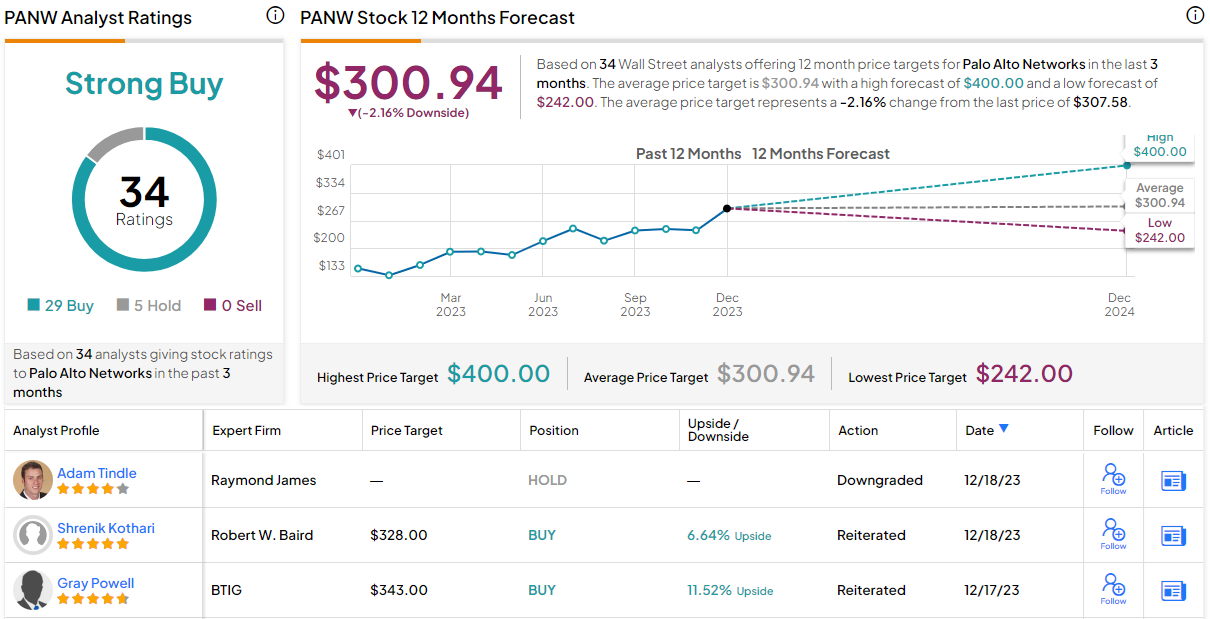

Quantifying this stance, Patil rates the shares as Positive (a Buy), with a Street-high $400 price target implying a one-year upside potential of 30%. (To watch Patil’s track record, click here)

This stock boasts a Strong By consensus rating, based on 34 recent reviews that include 30 Buys and 4 Holds. However, the shares have gained over 120% year-to-date, and the average price target of $300.94 now suggests the stock will stay rangebound for the foreseeable future. (See PANW stock forecast)

SentinelOne (S)

Next on our list of Susquehanna picks is SentinelOne, a cybersecurity company and platform built for autonomous action, aiming to protect and secure all facets of today’s digital infrastructure – the data systems, as well as the storage, processing, and information systems. The company gives its customers and end-users solutions based on AI, to prevent online security threats through early detection and response.

SentinelOne’s platform will work proactively to halt cybersecurity threats. The system hunts across endpoints, containers, cloud software and workloads, and IoT devices, to locate and defeat every attack, every second. The company’s Singularity Platform performs at large and small scales, with higher speed and more accuracy than any human operator – or any team of human operators.

The key here is endpoint security – SentinelOne’s specialty. The company targets its protection on all system endpoints – the devices that can be connected to the network – and provides security for all originated and received communications. The endpoints protected are varied, and can include all linked desktops, laptops, and mobile devices.

It’s a value proposition that served the company well in its recent report for Q3 of fiscal year 2024. The company beat both the top and bottom line forecasts and increased its revenue guidance for both Q4 and the full fiscal year 2024.

At the top line, the company’s total revenue came to $164.17 million, up 42% y/y and some $7.85 million better than the forecasts. Adj. EPS of -$0.03 beat the Street’s call by $0.05.

On guidance, the company predicted Q4 revenue at $169 million, significantly better than the consensus estimate of $166.63 million. For fiscal year 2024, SentinelOne is forecasting revenue of $616 million, well above the previous $605 million forecast – and well above the $605.2 million the analysts were expecting.

That’s the background for Patil’s comments. The 5-star analyst notes that the company has a solid position – and also benefits from a solid reputation. He says of the firm, “SentinelOne’s unique positioning as a cloud-first endpoint vendor and a general industry perception of its best-in-class technology serve to underpin our Positive view on the company. We see S as one of the key beneficiaries of the need for improved security and expended observability, with several checks highlighting the quality of its technology. We see significant opportunity ahead in the form of market expansion and competitive displacements.”

Patil’s Positive (Buy) rating on these shares is complemented by his $35 price target, which points toward a 31% gain on the one-year horizon.

Overall, Wall Street gives SentinelOne a Moderate Buy consensus rating, backed up by 26 recent analyst reviews that break down to 12 Buys and 14 Holds. However, here the 83% year-to-date gains have seen the stock surpass the $25.43 average target, which now represents downside of 5% from current levels. (See SentinelOne stock forecast)

Check Point (CHKP)

Last up today is Check Point, an ‘old timer’ in the world of internet security. Check Point has been handling online security since 1993, living up to its own stated mission: to make online communications and critical data safe, secure, reliable, and available everywhere the user needs it. Today the company is an industry leader and one of the largest pure-play digital security firms in the global market.

Check Point’s solutions protect its customers from cyberattacks of all sorts. The company’s Harmony product line focuses on remote users, Cloud Guard automatically secures cloud-based software and networks, Quantum provides a unified security environment for data centers and network perimeters, and Horizon is a prevention-oriented suite of security operations. The company boasts a client list over 100,000 strong, that includes one-fourth of the global Fortune 500 firms.

In addition to protecting its own customers, Check Point has taken proactive steps to protect its own intellectual property – a vital step that helps to ensure the integrity of its own products. The company currently holds 73 US patents, and has another 30 patents pending. Check Point’s solid suite of security products and tools are used by clients at all scales, across 88 countries around the world.

Check Point’s business generated an adj. net income of $242 million in 3Q23, the last quarter reported. This was up 10% y/y and resulted in non-GAAP EPS of $2.07, 5 cents per share ahead of the forecast. Check Point’s revenue total for the quarter came to $596 million, up 3.2% from the prior-year quarter – and nearly $3.8 million better than expected.

Beating the earnings forecasts and maintaining its sound position in a vital niche will attract optimistic analyst attention to any company, and Susquehanna’s Patil says of this stock, “CHKP’s solid positioning in the space and positive sentiment from our checks with regard to tech capabilities and execution, coupled with the company’s renewed willingness to invest in S&M and acquire key technologies, lead to our Positive rating on the stock. We acknowledge that the company’s growth profile has been slower than some others in the space but see the potential for acceleration in years to come and believe the name is particularly attractive for GARP investors.”

That Positive (Buy) rating comes with a $190 price target to imply a potential upside of 27.5% for the year ahead. (To watch Patil’s track record, click here)

This is another stock with a Moderate Buy rating from the analyst consensus; Check Point’s 23 recent analyst reviews feature 9 Buys – but also 14 Holds. That said, the $150.94 average price target implies the shares are currently fully valued. (See CHKP stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.