Ulta Beauty (ULTA) is a retailer of beauty products and services in the United States. The company operates in five major product segments. The largest segment by revenue is Cosmetics, followed by Skincare, Bath, and Fragrance, Haircare Products, Services, and Other.

In the spring of 2020, Ulta was forced to shut all of its stores temporarily due to COVID-19. Results suffered significantly during this period. The company focused on omnichannel sales during this time and has come back stronger than ever.

I am bullish on ULTA stock. (See Analysts’ Top Stocks on TipRanks)

Ulta Crushes Earnings Estimates

Ulta reported Q3 2022 earnings on December 2, and beat estimates across the board. The company posted $2 billion in top-line revenue, $120 million over estimates.

It also posted $3.93 earnings per share in the quarter, easily besting the $2.47 estimates. The company is showing that it is fully recovered from its pandemic-related shutdown in 2020.

Q3 revenue was an impressive 29% above the same period in the prior year, when just $1.5 billion was posted. Gross profit was 44% higher, showing that the increase in revenue was not just the result of higher prices due to inflation.

Operating margin dipped slightly from 17% in Q2 fiscal 2022 to 14%. As a seasonal business, the current holiday shopping season will be critical for Ulta.

The company is trending to have its best quarter ever in Q4. This will likely add up to the company’s best full year on record for revenue and earnings per share.

Raised Targets Warranted

After earnings were released, several analysts boosted targets for Ulta Beauty. Oppenheimer has named the company a top pick on strong growth and increased guidance moving forward.

Earnings per share are now expected to reach $16.70 to $17.10 against the prior estimate of $14.50 to $14.70 for the current fiscal year. Using the midpoint of this estimate puts the P/E ratio at just under 24. This is very reasonable for a growing, highly profitable company.

The company’s balance sheet is also very strong. During the height of the pandemic in 2020 Ulta took out $800 million in long-term debt to weather the storm. Two quarters later, the company paid it back in full and remains long-term debt free.

The company maintains over $600 million in cash and equivalents on the balance sheet at last report. Because of this, the enterprise value is even more attractive than the market cap. On a forward basis, the company trades at an EV to EBITDA ratio of just 15.1.

Further drivers of growth include opening mini Ulta stores insider Target (TGT) locations throughout the U.S. This will provide significant synergies between the two companies, including the sharing of rewards members, increased foot traffic, and the ability to market to new consumers.

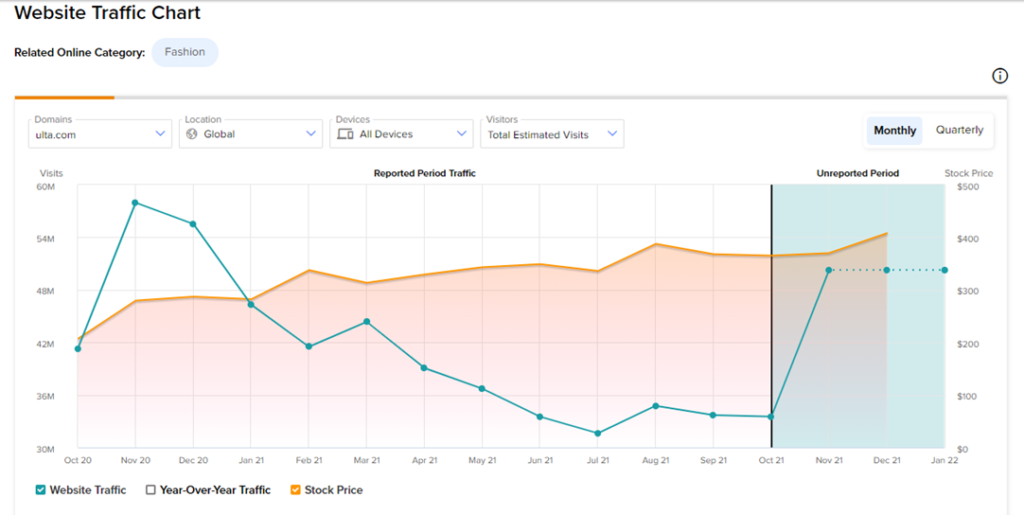

Ulta’s Website Traffic

According to TipRanks’ Website Traffic Tool, year-to-date visits to Ulta’s website are up 2.5% from the same period last year.

This bodes well as we head into the all-important holiday shopping season.

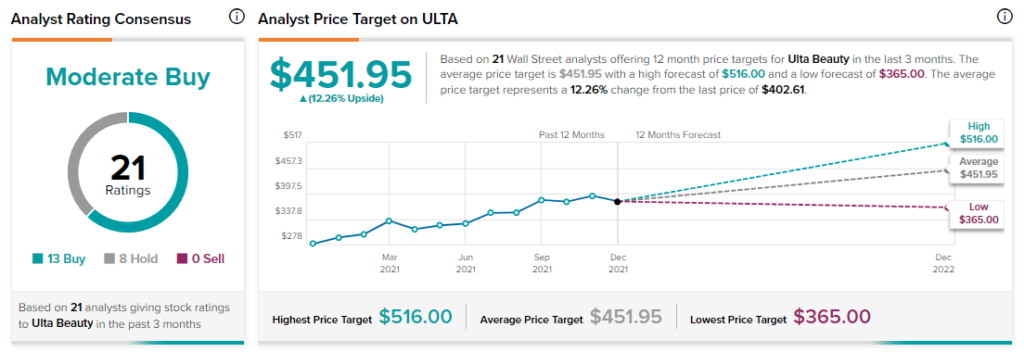

Wall Street’s Rating

Turning to Wall Street, analysts are somewhat bullish on ULTA stock, with a Moderate Buy consensus rating. This rating is based on 13 Buy recommendations, and eight Hold recommendations.

The average Ulta Beauty price target of $451.95 implies 12.3% upside from the current price.

Summary on Ulta Beauty Stock

Ulta Beauty survived the worst the pandemic had to offer and has come back stronger than ever. Q3 earnings showed that analysts were far too conservative in initial estimates.

The core business is strong, profitable, and growing. The stock is starting to attract positive attention from analysts, and still trades at a very reasonable valuation. Ulta Beauty remains a terrific value for long-term investors.

Disclosure: At the time of publication, Bradley Guichard had a position in securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates Read full disclaimer >