With the New Year less than a month away, now is a good time to start putting our investment portfolios into order for 2024. The goal is to maximize returns, as always, and there’s only one trick to that: finding the best stocks, with the strongest long-term potential. Finding can be a chore, however, since it involves sifting through the imposing wall of data tossed up by thousands of public stocks moving through tens of millions of trades every day.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

This is what the TipRanks Smart Score was made for. This data sorting tool, driven by an AI-powered, natural language machine learning algorithm, gathers all the data from the stock markets – the reams of information generated by those million and millions of daily trades – and collates it according to a set of factors that have been proven to match up with future share outperformance. Each stock then gets a grade, a simple score on a scale of 1 to 10, that gives a quick at-a-glance indication of where the shares will likely go in the coming 6 to 12 months. The Smart Score makes a handy guide for investors seeking a ready indicator of a stock’s main chances.

So let’s follow this lead, and use the Smart Score to find several stocks that score the ‘Perfect 10’ and show solid opportunity to outperform the market going forward. These 3 high-scoring stocks all show Strong Buy ratings from the analyst consensus, and room for more appreciation according to the data collected on the TipRanks platform. Here are the details.

Don’t miss

- Obesity Drugs Have Multi-Billion-Dollar Market Potential, Says Oppenheimer — Here Are 2 Stocks to Take Advantage

- J.P. Morgan Recommends These 2 ‘Strong Buy’ Stocks With Over 60% Upside Potential

- ‘Bright Spots’ Could Lift These 2 Hotel REIT Stocks Higher, Says Oppenheimer

Super Micro Computer (SMCI)

We’ll start with Super Micro Computer, an information tech firm based in San Jose, California and focused on developing and delivering application-optimized, high-performance server and storage solutions that address and solve the multitude of issues involved in high-end, computational-intensive server workloads. The company has more than two decades worth of design experience, and is a leader in the data server market, offering a wide range of storage systems, subsystems, and accessories, made to order to the customers’ unique specifications and configurations.

All of this makes Super Micro a world-class provider in the server hardware ecosystem. The company’s product lines have found applications in everything from Edge/5G, data centers, public/private cloud, to AI and machine learning, and are backed by solid software and service protection.

Super Micro’s top end products are known to stand at the cutting edge of liquid cooled server rack solutions, and they are in high demand, especially in the data center market. The company has manufacturing facilities in the US, Taiwan, the Netherlands, and Malaysia, and has been expanding its capacity across the board to reduce delivery times. Last month, Super Micro announced that increases in its manufacturing capacity had bumped up its ability to deliver products, to 5,000 fully tested AI, HPC, and liquid cooling rack solutions per month. The company has maintained this achievement while keeping up its reputation for ‘green’ computing.

Even better, for investors, Super Micro has also registered share growth of 221% so far this calendar year – and we still have a month left of 2023. In the November 1 release of the fiscal 1Q24 financial results, Super Micro posted a top line of $2.12 billion, up 14% year-over-year and beating the forecast by some $60 million. At the bottom line, the company’s earnings came to $3.43 per diluted share in non-GAAP measures, a figure that was 18 cents ahead of the estimates.

The company’s recent manufacturing expansion was cited as a particular strength by Rosenblatt analyst Hans Mosesmann, who says, “Supermicro is a leader in the liquid cooling ‘at scale’ and based on the new demand profile is set to expand starting next year capacity to 5K/month racks (incremental for liquid cooling) from current 4K racks/month. With Malaysia capacity increases racks/month move to 6K. The company over time will, we believe, monetize this advantage that can double AI compute per rack as power profiles go from ~20-30 KW to 80-100KW per rack.”

Putting this into a recommendation, the 5-star analyst goes on to explain why believes this stock will continue to gain: “We are impressed with the company execution and early focus on ‘green,’ building block formats, S/W investment, and liquid cooling initiatives now ready for prime time.”

Mosesmann rates SMCI as a Buy, and his $430 price target points toward a robust one-year upside potential of 59%. (To watch Mosesmann’s track record, click here)

The Strong Buy consensus rating on Super Micro’s shares is unanimous, based on 5 positive analyst reviews set in recent weeks. The stock is selling for $269.63 and its $405.60 average target price implies an upside of 50% in the next 12 months. (See SMCI stock forecast)

Pure Storage (PSTG)

Next up is Pure Storage, a digital tech firm working in a vital niche, data storage. Specifically, Pure Storage focuses on computer memory chips and data storage, through portable flash-based servers – but more recently through cloud-based data storage subscriptions, offering storage-as-a-service. The company’s product lines and services are fully scalable, allowing customers to adapt their data systems to their changing data needs. Pure Storage can work with small-office workloads, modern applications, or even data-center-scaled projects.

Pure’s cloud experience makes data storage easy, and the company boasts that it can permanently ‘uncomplicate’ the data storage experience for customers at all scales and in all niches. As the company puts it, cloud-based data storage, a cloud experience, reduces the complexity and expense of managing both data and the supporting infrastructure, empowering organizations to focus on their most important work.

Like many modern tech firms, Pure is working to perfect its core competency while also making a positive environmental impact. The company’s data storage systems are energy-efficient, and Pure bills them as ‘reducing data center emissions worldwide,’ an important point in an industry that is known for its high levels of electric power consumption.

All of this is for the good, and the stock is up by 22% year-to-date, but it has been subject to a bit of a beating recently, following last week’s release of the company’s fiscal 3Q24 earnings report – while Pure’s report beat the forecasts, the forward guidance for fiscal year 2024 revenue was considered disappointing. The company reduced its guidance from $2.96 billion for the fiscal year to $2.82 billion; the new target figure represents year-over-year growth of just 0.7%.

The current numbers are better. Fiscal Q3 revenue was up 13% y/y, to $762.8 million, and beat the forecast by $1.3 million. The earnings figure, of 50 cents per diluted share by non-GAAP measures, was 10 cents above expectations.

5-star analyst Nehal Chokshi, writing from Northland Capital Markets, looks at Pure Storage in context with its peers and comes down to a bullish conclusion, writing, “PSTG fits the characteristics of companies that are navigating the current macroeconomic weakness successfully of (1) less than 20% penetration into core addressable opportunity & (2) significant product differentiation that will drive consistent market share gains. On top of which, the strength in Evergreen subscription STaaS (storage as a service) and stronger product premium PSTG is able to drive leads us to raising our LT OM assumption from 23% to 32% within our DCF.”

These comments back up Chokshi’s Outperform (Buy) rating on these shares, and his $58 price target implies a strong 12-month potential upside of 75%. (To watch Chokshi’s track record, click here)

There are 10 recent analyst reviews for Pure Storage, and their 9 to 1 breakdown favoring Buys over Holds is decisive, giving the stock its Strong Buy consensus rating. The shares are currently trading for $33.15 and the $41.50 average price target suggests that they will gain another 25% in the year to come. (See PSTG stock forecast)

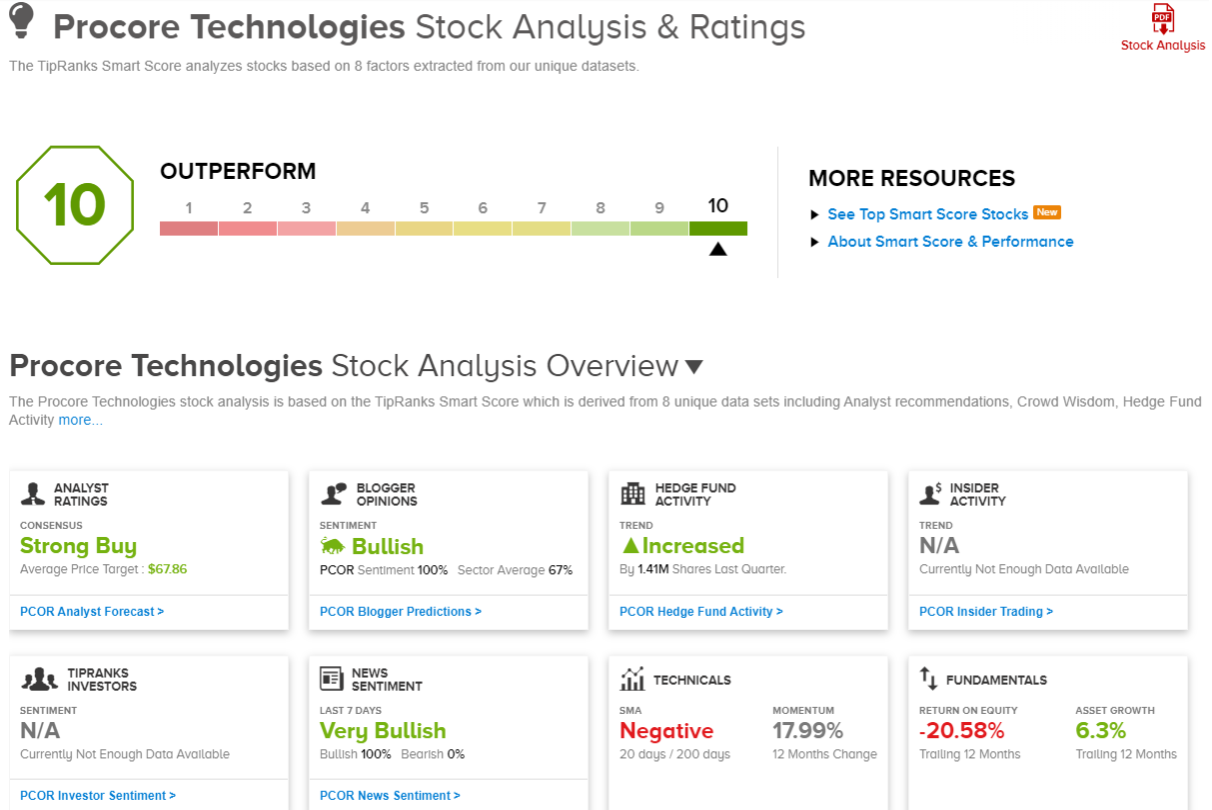

Procore Technologies (PCOR)

We’ll wrap up our Perfect 10 list with Procore Technologies, a company that applies high-tech and top-end software systems and data analysis to the construction industry. That may not sound like an easy marriage, but Procore makes it work. The company offers the industry a set of collaboration tools, based on a cloud-computing construction management platform, that can integrate the variegated efforts of builders, contractors, project managers, and property owners, for greater integration of their efforts.

These are all vital stakeholders in any construction project, and Procore’s platform allows for any one of them to take center stage, coordinating the efforts of the group. The platform is accessible from connected devices, such as smartphones and tablets, as well as desktop and laptop computers, and makes it possible for all the stakeholders to share document updates, site and project plans, and other vital data.

The company’s software platform doesn’t just integrate the stakeholders – it also offers a set of tools to effectively manage their work. These include such ‘vital stats’ as document storage, drawing markups, and meeting minutes, which are made digitally available, in real time, to the impacted parties. These products, and the ability to streamline the overall management of complex construction projects, have gained Procore plenty of industry popularity; the company boasts that its platform has been used or is in use with over 1 million projects in 150 countries around the world.

The global construction industry presents Procore with a rich environment for growth; by 2025, construction sector spend is expected to reach $14 trillion, and faces potential losses in the neighborhood of $500 billion due to poor communications and subsequent rework. That’s Procore’s target, and the company has estimated that potential productivity gains from smoothing out those rough edges and communications glitches can far exceed $1 trillion annually.

For BMO analyst Daniel Jester, Procore presents plenty of reasons for investors to take notice. “With a strong core in project management, multiple drivers to expand logos, a long-term platform vision to capture more workflows, and margins approaching an inflection to sustained breakeven over the coming year, we anticipate upward tension to numbers,” Jester wrote. “We see a compelling medium-term opportunity for the shares for a sector winner even in what is likely to be an uneven macro environment for construction in 2024.”

Jester’s commentary supports his Outperform (Buy) rating on PCOR, while his $76 price target indicates room for an upside potential of 26% on the one-year horizon. (To watch Jester’s track record, click here)

Overall, Procore’s Strong Buy consensus rating gets support from 13 recent Buy recommendations, that outweigh 3 Holds. The stock’s average price target, of $67.86, implies the shares will gain ~12.5% in the next year, from the current share price of $60.38. (See Procore’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.