A key to success in the stock market is a touch of foresight. Not quite precognition, but an ability to spot and put together clues and trends, to discern the ‘next big thing’ before it hits. This is true in every stock sector, but today we’ll focus on biotech.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The biotech firms have famously high product lead times, paired with equally high overhead expenses; it’s a combination that would make them unlikely investments, except that when a drug is approved, it can turn into a blockbuster. Successful biotech investors will learn how to spot those blockbuster biotech opportunities before they hit.

A new sector review by Oppenheimer’s five-star analyst Jay Olson sees just such an opportunity in the market for obesity drugs. He notes that this field has multi-billion-dollar market potential, and writes, “We consider obesity the next wave for healthcare investors following on the heels of Immuno-Oncology (IO). Consensus sales for obesity drugs already approved and in development are expected to reach ~$67B. Meanwhile, obesity sales are expected to exceed IO in 2029 before reaching a similar peak in 2032. The obesity opportunity is driven by overwhelming demographics and favorable treatment dynamics in subpopulations enabling positive treatment outcomes.”

Olson goes on to start picking the biopharma companies that are ready to take advantage of this ‘next wave.’ Here are two of Olson’s choices, two stocks that are set for gains in the year ahead, on the obesity drug bandwagon, with details taken from the TipRanks platform.

Don’t miss

- J.P. Morgan Recommends These 2 ‘Strong Buy’ Stocks With Over 60% Upside Potential

- ‘Bright Spots’ Could Lift These 2 Hotel REIT Stocks Higher, Says Oppenheimer

- There’s an Opportunity Brewing in These 3 Stocks, Says Goldman Sachs

Viking Therapeutics (VKTX)

We’ll start with Viking Therapeutics, a biopharmaceutical company in the clinical stages of development, focusing its research on the treatment of endocrine disorders and other metabolic diseases. The company’s pipeline features novel therapies that are either first-in-class or best-in-class and are designed as orally-dosed, small-molecule compounds.

Viking currently has three drug candidates in its research pipeline, spread across four separate study tracks. The company’s leading drug candidate, VK2809, shows promise as a potential treatment for several metabolically-linked conditions, including non-alcoholic steatohepatitis (NASH), type-2 diabetes, and obesity, all of which are interrelated. The company’s second-leading candidate, VK2735, directly targets metabolically-linked obesity.

Viking has garnered attention with VK2809, its NASH candidate, which is currently in the Phase 2b clinical trial stage, known as VOYAGE. Earlier this month, the company released data indicating a positive effect on liver fat reduction across various patient subgroups, including patients with F1 fibrosis and a related risk factor such as obesity.

Of more immediate interest to investors seeking a biopharma with an obesity-centered pipeline, Viking initiated the Phase 2 VENTURE trial for VK2735 in the treatment of obesity this year. VK2735 is a wholly-owned drug candidate, acting as an agonist of the GLP-1 and GIP receptors. Previous data from the Phase 1 trial demonstrated that the drug candidate was well-tolerated under various dosing regimens, with an acceptable safety profile. Viking has completed the patient enrollment process for the VENTURE study, and results are expected to be released in 1H24.

Oppenheimer’s Jay Olson sees these two drug candidates as key drivers for Viking, especially VK2809 and its applications for NASH. He does not neglect the obesity-centered candidate VK2735, however, and writes, “We view VKTX’s lead candidate THR-β agonist VK2809 for NASH as similar to Madrigal Pharmaceutical’s MGL-3196 with comparable Ph2a efficacy results of relative liver fat reduction that are at least as strong. We believe that if VK2809 Ph2b biopsy-confirmed NASH trial outcome is sufficient to continue into Ph3 development, then we see VKTX’s current market cap as undervalued compared to its peers. We believe that VK2735 offers asymmetric upside potential based on current valuation.”

Olson sees plenty of room to run on this stock – more than enough to justify his Outperform (i.e. Buy) rating. He gives these shares a $40 price target, implying a robust 207% upside potential on the one-year horizon. (To watch Olson’s track record, click here)

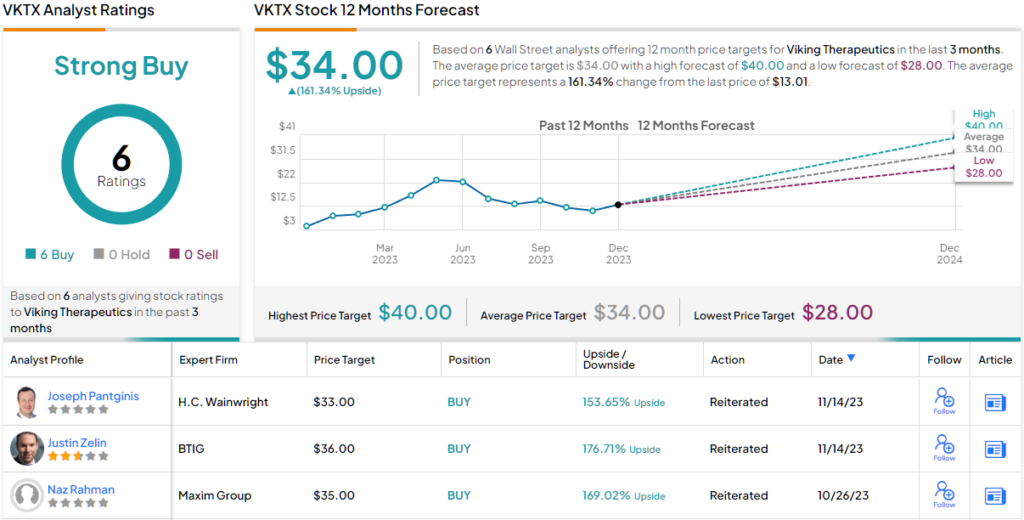

It’s clear that Wall Street agree with this bullish case. The stock has 6 recent ratings, and they are unanimously positive – for a Strong Buy consensus rating. Shares are trading for $13.01, and their $34 average price target suggests a one-year upside of 161%. (See VKTX stock forecast)

Amgen, Inc. (AMGN)

For the second Oppenheimer pick, we’ll look at one of the largest biotechs in the US. Amgen, based out of Thousand Oaks, California, is ranked sixth largest among US biopharmas, by market cap – and ranked #18 globally by annual revenue. The firm is the largest employer in its home city, with approximately 5,000 employees working at its headquarters.

Amgen has both a solid stable of marketable drugs and an extensive research pipeline of new drug candidates. Unlike the small biopharmas, Amgen can boast having a sizable revenue stream, some $26 billion in 2022, based on its lines of approved products. That revenue stream is expanding this year; Amgen’s $19.87 billion in revenue through the third quarter of this year was up 2.8% from the first nine months of last year.

That gives the company a strong foundation to fund its extensive research program. For our purposes here, we’ll look at two drug candidates in the program – AMG 133 and AMG 786. Each targets obesity, but in different ways. AMG 133 is a multispecific molecule designed to inhibit the GIPR receptor while activating the GLP-1 receptor. The target patient population for the current Phase 2 study of the drug candidate targets overweight or obese adults with or without type 2 diabetes mellitus. Enrollment in the study is complete, and Amgen expects to release its topline data late next year.

Amgen’s second obesity drug candidate is AMG 786, a small molecule compound in a targeted obesity program. Amgen has been careful in designing these drugs, to avoid duplicating their modes of action. The initial data readout on AMG 133 is planned for 1H24.

Oppenheimer’s Jay Olson holds an optimistic view of Amgen, particularly highlighting AMG 786 as a significant factor. He states, “We view several pipeline assets as underappreciated ahead of near-term readouts, such as oral AMG-786 with a unique MOA for obesity with Ph1 data in 1H24… We forecast Amgen revenue growth over the next ten years leveraged by margin expansion, as management has a track record of financial discipline. On the top line, we believe Amgen is in a position to maintain long-term revenue growth as mature products fade while the R&D pipeline continues to more than compensate with innovative new products.”

Taking this forward, Olson gives AMGN shares an Outperform (i.e. Buy) rating, along with a $310 price target that suggests a 14% increase over the coming year.

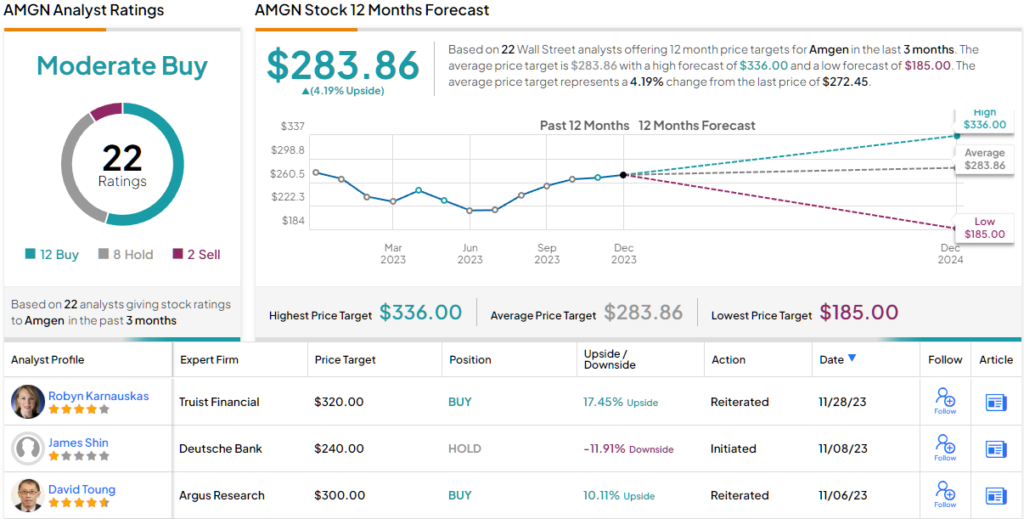

Turning now to the rest of the Street, opinions vary. 12 Buys, 8 Holds and 2 Sells add up to a Moderate Buy analyst consensus rating. Additionally, the $283.86 average price target implies a modest upside potential of 4%. (See Amgen stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.