As investors prepare their investment portfolios for 2024, it’s important to bear in mind a fundamental paradox associated with pricing signals. Occasionally, sound stocks find themselves trading at rock-bottom prices with no substantial fault of their own. Various factors, such as unfortunate timing or transitory dips in revenue or earnings, can drive prices down. There are numerous reasons why shares can flirt with a bottom, and they do not necessarily indicate weak underlying fundamentals.

The solution to this paradox, the way to identify robust stocks at bargain prices, lies in the data, in dipping into the deep wells of information generated by several million daily stock trade transactions to find out what the market really thinks of any particular stock.

That’s a daunting task, but the TipRanks Smart Score is up to it. This data sorting tool makes use of both AI and natural language processing to sort through the sheer volume of stock data and to use it. The Smart Score algorithm compares every public stock to a set of factors that have been shown to predict future performance. It gives them a rating, a simple score on a 1 to 10 scale that shows each stock’s likely forward performance. The ‘Perfect 10s,’ the stocks with the highest Smart Scores, are worth a closer look from investors. And when top-scoring stocks, when combined with rock-bottom pricing, it’s a potential bargain that can’t be ignored.

Against this backdrop, we pinpointed two stocks from the TipRanks Perfect 10 list, each flirting with bottom-level pricing but offering investors ‘Strong Buy’ ratings from the Street, solid upside potential, and that data-backed perfect Smart Score.

Darling Ingredients (DAR)

The first stock on our list is Darling Ingredients, a food industry-slash-agritech company that has found an interesting, and useful, niche making use of food production by-products to reduce waste in the chain from farm to table. The company notes that, typically, only 50% of an animal raised as livestock will make it to human dinner tables – but that the ‘other 50%’ doesn’t need to be thrown out. The animal remains and organic materials left over from the food production system can be diverted back into useful products.

At the practical side, Darling takes that approach. The company gathers animal by-products and turns them into a wide range of food service ingredients. These can include gelatin (used in medicine, for pill capsules), collagen peptides (used as supplements to promote skin, hair, and nail health), and foods for both livestock and pets. Finally, ‘waste’ products that cannot be consumed by people or animals, such as inedible animal fats, can be gathered and converted into green energy products, particularly biodiesel fuel.

This puts Darling at the forefront of both the waste reduction and renewable fuel fields – two ‘green economy’ segments that have strong social and political support.

Nevertheless, Darling’s share price is down 34% from the peak it reached in July of last year. The sell-off in DAR came in the wake of an EPA update in the renewable volume obligations – that’s government mandates – for the quantity of renewable fuels that must enter the US fuel supply. Darling is an important producer of D4 RINs – an advanced type of biomass diesel which can be used to comply with several RIN mandates. The reduced obligations from the EPA pushed down prices on D4 RINs, which are now well below $1 per gallon.

The rapid fall in D4 RIN prices was bad enough. But shortly afterward, Darling reported its 3Q23 results, in which the company missed expectations at both the top and bottom lines. Darling’s revenue came to $1.6 billion at the top line, down 8.6% year-over-year and $160 million below the forecast. At the bottom line, the company reported an EPS, by GAAP measures, of 77 cents per share, missing the estimates by 4 cents.

Covering this stock for Stifel, analyst Derrick Whitfield outlines a path for Darling as it recovers from the sell-off. Whitfield writes, “We believe the negative associated with the D4 RIN collapse is priced into the stock while the near-term and Q124 catalysts are not. The event path we see to re-rate the stock is: 1) CARB plans to publish its Staff Report by year-end, which could increase LCFS prices and DGD’s 2024 margins by +100% and +70%, respectively, 2) expansion of consensus DGD’s margins (~$0.09/gallon) following DGD 3’s LCFS Tier 2 pathway certification on December 6th, 3) progression on SAF business with proof of commercial contract and DGD 3 conversion, which could expand DGD margins by $0.38/gallon assuming DGD 3 conversion only, 4) proof of a sustainable margin ($1.10/gallon) in the current depressed margin environment, and 5) narrowing of waste FOG price spreads resulting from increased industry utilization of waste FOG feedstocks (driven by LCFS and 45Z policy), potentially expanding Upstream EBITDA by + $50mm.”

Whitfield goes on to rate DAR shares as a Buy, and his $123 price target implies a one-year upside potential for the stock of 166%. (To watch Whitfield’s track record, click here)

It’s clear from the consensus rating, a Strong Buy based on 10 Buys and 2 Holds, that Wall Street generally agrees with the bullish views on this one. The shares are trading for $46.21, and the $76.80 average price target suggests a potential gain of 66% for the year ahead. (See DAR stock analysis)

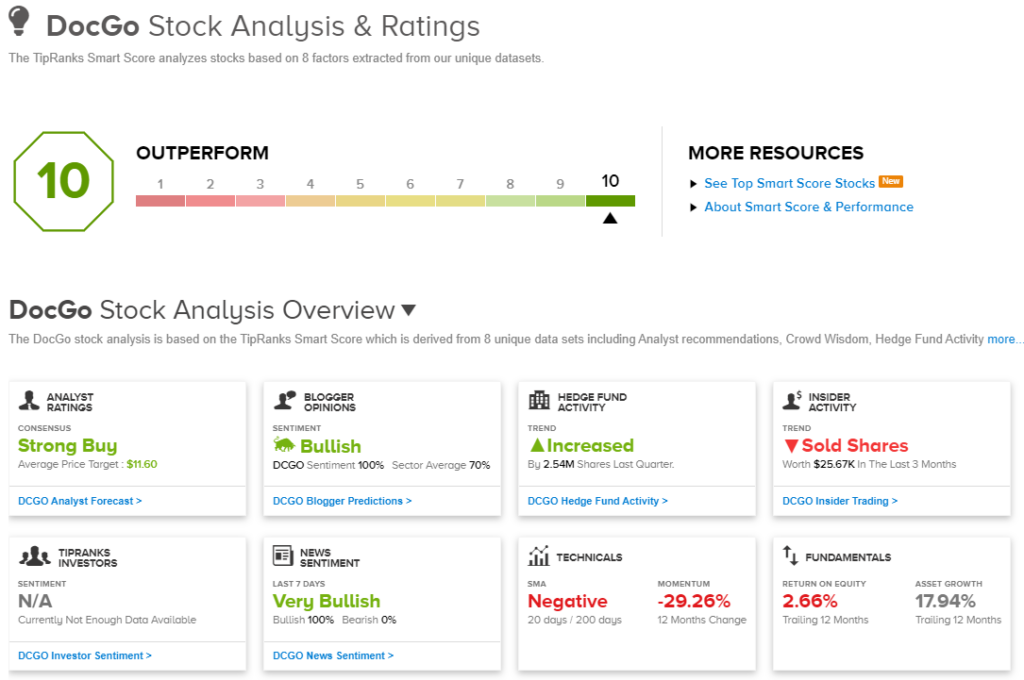

DocGo (DCGO)

Now, let’s take a closer look at DocGo, a healthcare company that has effectively built its own niche within the telehealth segment. DocGo has successfully addressed the challenge posed by the disconnect between remote medical consultations via video and the occasional requirement for patients to have in-person interactions with healthcare providers. Drawing inspiration from the ‘last mile’ concept in the package delivery industry, DocGo steps in to bridge this gap by dispatching healthcare professionals to the patient’s location, seamlessly connecting virtual consultations with essential in-person care.

That this service is necessary and attractive can be seen in some of the company’s numbers. DocGo has over 6,000 employees working in the US and the United Kingdom. It has active operations in 28 US states as well as the UK. DocGo has tallied more than 7 million direct patient contacts in its company history.

The other relevant number to show DocGo’s success is the company’s revenue. As of 3Q23, the company has recorded five consecutive quarters of sequential revenue growth. In that third quarter, the company’s top line came to $186.6 million, up an impressive 78.9% year-over-year and $38.9 million over the estimates. The bottom line, however, reported as a 5-cent EPS, missed the forecast by a penny.

With all of that, DocGo’s share price has plummeted in recent months. The stock peaked in August, at more than $10 per share, and is down some 53% from that level. A series of idiosyncratic headwinds have buffeted the stock.

These headwinds included the rejection by the New York City comptroller of a $432 million contract for mobile health services to the city’s migrant population – although the Mayor, Eric Adams, retains the power to reinstate the contract. After that, DocGo faced a potential scandal when CEO Anthony Capone resigned after it came out that he had misled on details of his educational background. The CEO position has since been filled by Lee Bienstock, the Google veteran who had been serving as DocGo’s COO.

David Larsen, an analyst at BTIG, expresses optimism about DocGo’s prospects under new leadership and a workable business model. He stated, “Mr. Bienstock’s background at Google and his experience in sales and advertising from a technology platform, in our view enhances his ability to scale DCGO. We expect the contract with the City of New York to be renewed in 2024 and beyond, cash is flowing well with that client, we view the long-term in-sell potential into health plans as being very robust, DCGO continues to win new deals, and we are impressed with the breadth and depth of services that DCGO has, including primary care. The stock has been under pressure, but with 40% y/y revenue growth and a ~10% adjusted EBITDA margin, our view is that it’s only a matter of time before the value of the business is reflected in the share price.”

These comments back up Larsen’s Buy rating on the stock, and his $13 price target suggests the shares will appreciate by a robust 164% over the course of 2024. (To watch Larsen’s track record, click here)

Clearly, the bulls are running on this stock. DCGO shares have a unanimously positive Strong Buy consensus rating, based on 5 recent analyst reviews. The $4.93 current trading price and the $11.60 average price target combine to imply a one-year gain of 135%. (See DocGo stock analysis)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.