Ridesharing and delivery behemoth Uber Technologies (NYSE:UBER) stock took Wall Street by surprise yet again earlier this month, as its Q1 results remained unfazed by macro concerns. The stock is up 55% year-to-date. However, despite the stock continuing to head north, I continue to be bullish and believe that there is more upside ahead. This is primarily due to Uber’s persistent stride towards profitability and its industry-leading status underpinned by robust business fundamentals.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

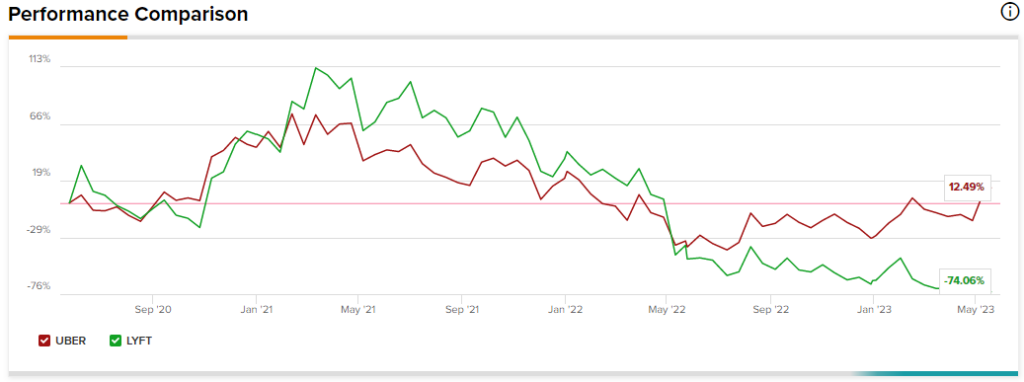

It’s remarkable that Uber stock rallied following its upbeat results while its main rival, Lyft (NASDAQ:LYFT), continues to fall. In sharp contrast to Uber stock, Lyft shares are on a downward spiral despite reporting a Q1 beat almost three weeks ago. The recent quarterly results once again prove that Uber has a clear market-leading position in Mobility (total trips increased 24% year-over-year to 2.1 billion). Uber continues to outperform Lyft, as seen from the price-performance comparison chart below.

When I last wrote about Uber, I highlighted how Uber looks set on its fast-paced growth toward profitability. With its improving operating leverage and successful cost discipline, the company is fast approaching its profitability goals. Uber has already been reporting profits on an adjusted basis for the past seven quarters and has turned free-cash-flow positive ($549 million in Q1). On top of that, management said that it is on track to report profits on a GAAP basis soon.

In addition, the ride-hailing industry is still in its nascent stage with a significant total addressable market (TAM). According to MarketsandMarkets, the industry is expected to grow at a CAGR of over 16% from the 2021-26 forecast period. Being an industry leader, Uber will continue to benefit from the overall industry growth.

Blowout Q1 Results & Upbeat Guidance

On May 2, Uber reported blowout Q1 results, topping both earnings and revenues expectations. Not only did the company report robust gross bookings that grew 19% year-over-year, but it also impressed investors with higher EBITDA, aided by enhanced unit economics. Specifically, the incremental EBITDA margin as a percentage of gross bookings came in at 12%, well above the company’s long-term target of 7%. Notably, this is the seventh quarter in a row that the firm has surpassed its incremental EBITDA margin target.

On top of that, Uber’s GAAP net loss narrowed significantly to $157 million during the quarter compared to the $5.9 billion reported in Q1 2022. This clearly indicates that the company is quickly approaching break-even levels.

The key highlight of the report was robust bookings growth seen in Mobility (40% year-over-year) and Delivery (8% year-over-year). Despite tough macro trends, bookings remained resilient, which gave management enough confidence to lay out an optimistic, higher-than-expected bookings outlook for 2023.

What appealed to investors more was the raised guidance. For the second quarter, adjusted EBITDA is now expected to range between $800 million – $850 million, driven by strong gross bookings of $33 billion – $34 billion. Importantly, the company also expects its free cash flows to ramp up in the coming quarters and projects positive free cash flow for the full year.

Now, investors may think, is the company being overly optimistic, especially given a tough macro outlook? Digging deeper into this, if the macroeconomic scenario does get worse, users may postpone their decisions to buy expensive cars. They will likely benefit from more ridesharing options instead. This, in turn, may support the company’s mobility revenues.

Being fully aware of such a possibility, it is therefore not surprising that Uber is rapidly expanding UberX Share — its shared rides offering — into many more cities.

Advertising Growth Could be a Long-Term Revenue Driver

Top companies, including Amazon (NASDAQ:AMZN) and Netflix (NASDAQ:NFLX), are tapping the growth of high-margin digital advertisements. Uber has also followed suit, joining the industry.

In October 2022, Uber revealed its advertising division — Uber Journey Ads — a new way to monetize Uber rides. Teaming up with businesses, Uber shows video advertisements to customers via in-car tablets.

Notably, Uber expects to achieve Advertising revenues of $1 billion by 2024. The recent quarterly numbers imply that it is a plausible target. Uber saw record growth in the Advertising segment and continues to increase its focus on it. During Q1, the company stated that the number of advertisers using the Uber platform has grown by 70% to 345,000, which is outstanding.

To further tap the high-growth phase of the ad business, Uber keeps innovating. It recently revealed its plan to add advertisements on top of cars. This new ad feature will enable drivers to earn an additional $100 per week on average. The ad feature is a win-win for both Uber and its drivers as it can lead to higher driver retention, driven by better incentives.

Is Uber Stock a Buy, According to Analysts?

As per TipRanks, the Wall Street community is clearly optimistic about the stock. Overall, Uber commands a Strong Buy consensus rating based on 27 unanimous Buys. UBER stock’s average price forecast of $49.04 implies 25.2% upside potential from current levels.

In terms of its valuation, UBER is trading at an EV/sales ratio of 2.5x, higher than the peer group average of 1.7x. Nonetheless, the premium can be justified, given the company’s favorable industry-leading position and significant growth potential.

Conclusion: Uber Remains Attractive for the Long Term

UBER stock continues to gain from strength to strength, riding high on multiple positive factors. These include persistently upbeat results, improving margins, strong momentum in its Mobility and Delivery segments, and high growth potential from advertisements and other strategic innovations. Uber has shown its resiliency, and its multiple growth drivers continue to make me bullish on the long-term return potential of the stock.