Everyone knows that Big Tech has been the big leader in the market’s advance this year. A look at the market indexes will bear this out: the Dow has risen by 6% year-to-date, the S&P 500 by 18%, while the tech-heavy NASDAQ boasts an impressive 36% gain. What this means for investors, however, has been a subject of lively debate.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Chiming in from Bank of America, head of US equity strategy Savita Subramanian is urging investors not to worry so much about that narrow focus. In her view, big tech stocks should start looking more attractive in the near-term, as the companies benefit from a change in the market cycle.

“A lot of these big tech companies offer great growth way out in the future. So they’re going to get hurt harder by changes in the cost of capital. What some of these companies are doing is acknowledging that they’re too big to grow as quickly, so they’re returning cash and shortening their duration,” Subramanian opined.

Bank of America’s analysts are running with this idea, and they’re picking out some mid- and large-cap tech stocks that they think still have room to grow. We’ve dived into the TipRanks database to find out more about two of these Bank of America picks. Here they are, along with some recent thoughts from the Bank of America experts.

Don’t miss

- ‘Riding the Clean Energy Wave’: This Analyst Suggests 2 Stocks to Play the Renewable Energy Transition

- Billionaire Steve Cohen Goes Big on These 2 ‘Strong Buy’ Stocks — Here’s Why You Should Follow

- ‘Time to Hit Buy,’ Says Bank of America About These 2 Stocks

Gen Digital (GEN)

Based in both Tempe, Arizona, and Prague, Czech Republic, the first Bank of America pick is Gen Digital, a leader in online security. Describing its mission as fostering trust in the digital world, Gen Digital controls a family of brands that, together, provide a wide range of digital security and safety features. Based on names like Norton, Avast, and Reputation Defender, Gen’s stable of operating brands boasts a strong combination of market position and quality.

By the numbers, Gen has put up some impressive statistics. The company has operations in more than 150 countries and claims more than 500 million users globally. Gen Digital has been making extensive use of AI technology to solve issues of cybersecurity and offers its products on the popular freemium model, with a set of basic services available to all comers without charge, while paying subscribers can access a range of higher-level options.

During the July-September quarter, Gen Digital’s Avast brand reported stopping a record level of 1 billion online attacks per month. This is a record high and reflects a surge in AI-powered scams. Some of the chief areas of attack included finance and dating scams, adware, spyware, and malvertising. This data shows clear growth in the cybersecurity sector, a market that was worth $173.5 billion last year and is expected to reach as high as $266.2 billion by 2027.

In its last reported quarterly results, for fiscal 2Q24, Gen Digital showed continued solid performance. The company’s quarterly revenue came in at $948 million, up 27% year-over-year and a modest $500K above the forecast, while the 47-cent diluted EPS, the non-GAAP figure, was up 2 cents y/y and matched expectations.

In his coverage of GEN for Bank of America, analyst Jonathan Eisenson sees all of this providing a vista of opportunity for Gen Digital’s investors. He writes of the company, “We view Gen as an underappreciated software value play and highlight a few positives for the stock. First, we believe the consumer cyber safety market carries large, underappreciated growth opportunities, with Gen addressing a +$20bn TAM and 44% market share within the current target markets. The company has over 435mn freemium users and we see large cross-sell and upsell opportunities, as well as international expansion potential. We also highlight revenue and cost synergies from the Avast acquisition and view continued debt reduction and lower interest expense as stock catalysts. We model our FY25E/FY26E EPS at $2.29/$2.61, above the Street’s $2.25/$2.50, and we see additional upside potential to our estimates.”

Eisenson’s comments provide support for his Buy rating on GEN shares, while his $25 price target indicates room for ~20% upside in the coming months.

What does the rest of the Street have to say? 2 Buy ratings and 1 Hold have been issued in the last three months. As a result, GEN receives a Moderate Buy consensus rating. In addition, the $24.67 average price target suggests ~19% upside potential. (See GEN stock forecast)

StoneCo, Ltd. (STNE)

Next up is StoneCo, a financial tech company working in the Brazilian online payment sector. It’s sometimes easy for American investors to overlook the wide region south of the border – but that would be a mistake. Latin America is a dynamic region, home to several important developing economies – and to plenty of investment opportunities. StoneCo is one of these. The company works in the e-commerce niche, offering an end-to-end cloud-based platform for online purchases and payments.

StoneCo takes a customer-centric approach, and its product line is tailored to the needs of its small- to mid-sized business clients. Customers can find digital tools to solve every sort of POS issue, allowing users to conduct seamless business. The digital platform links electronic and in-person commerce seamlessly across brick-and-mortar, online, and mobile retail channels.

The company released its 3Q23 financial results earlier this month, and a look at them will show just where StoneCo stands right now. The top line came to R$3.14 billion, or approximately US$640 million after currency exchange. This was up 25% y/y, and was US$21.7 million better than had been expected. StoneCo’s bottom line for the quarter was given as R$1.32, a hefty increase from the R$0.35 in the prior-year quarter. The 27-cent US equivalent was 4 cents better than the forecast.

StoneCo has recently brought onboard new blood in the executive management team, as part of a concerted effort to improve execution on its long-term strategic plan. For Bank of America analyst Mario Pierry, this is a net positive, and should pave the way toward stronger growth.

“Stone’s recently disclosed strategy for the next three years sounded much like the past four years, which aims to increase the monetization of its client base through the cross sell of banking, credit and software services, while continuing to gain market share in the MSMB segment. While the strategy did not play out as expected in the past four years (due to poor execution and challenging industry dynamics), there has been significant turnover in the management team (including a new CEO, CFO, Head of Credit, and Head of Technology) and there is an increased sense of urgency on costs, which we think should yield better results this time. The successful execution of the strategy is expected to deliver net income CAGR of 31% from ’24-27 supported by solid top line growth and operating leverage, which is well above Consensus estimate of c.10%,” Pierry opined.

This stance is used to justify Pierry’s recent upgrade on STNE, from Neutral to Buy. He backs that with a price target of $17, implying the stock will appreciate by more than 22% in the coming year. (To watch Pierry’s track record, click here)

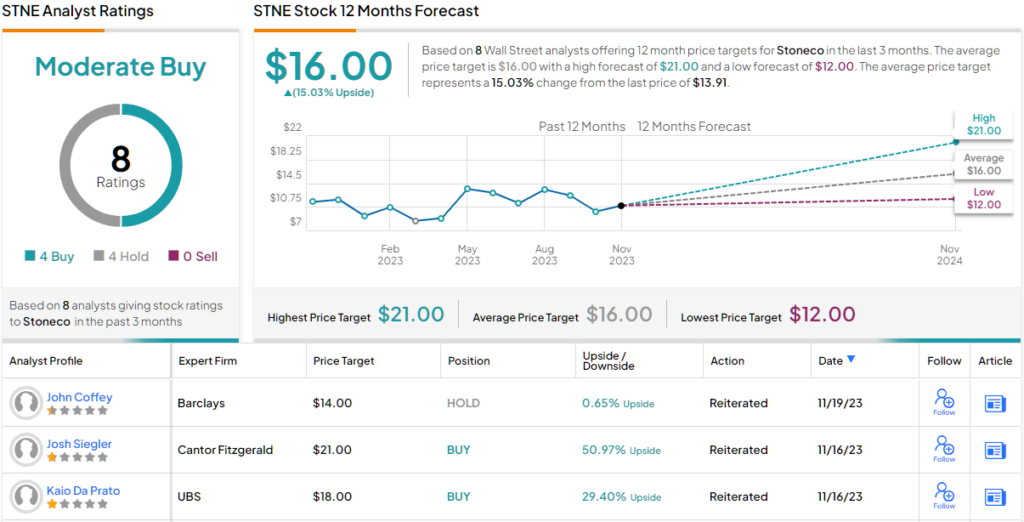

When it comes to other Wall Street analysts, opinions are split evenly. With 3 Buys and 3 Holds assigned in the last three months, STNE earns a Moderate Buy consensus rating. The average price target currently stands at $16, implying 15% potential upside in the year ahead. (See STNE stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.