Tectonic shifts are happening in the U.S. energy market as the industry undergoes a major transition in energy sources and installation projects are underway.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

According to American Clean Power, the U.S. energy storage market clocked a new record in the fourth quarter with new system installations of about 4,727 megawatt hours (MWh).

Despite delays, the period saw more capacity installations than the total installations during the first three quarters put together. Additionally, annual installations in the residential market are expected to reach 2GW by 2026.

Let us take a look at two names that are riding this energy wave and can offer opportunities for investors.

NRG Energy (NRG)

NRG produces and sells energy and associated services in the U.S. and Canada. Its 18,000 MW of generation capacity supports about six million home customers, along with commercial, industrial, and wholesale customers.

Shares of the company have jumped 14.7% in the last five days. A major part of these gains came on Friday, after the company announced its first-quarter numbers.

Revenue fell 2.4% year-over-year to $7.9 billion but exceeded the Street’s expectations by a massive $3.44 billion. Earnings per share at $7.17 also outperformed estimates by $6.53.

Notably, this quarter was a turnaround for the company, with a net income of $1.74 billion compared to a net loss of $82 million in the comparable year-ago period.

Additionally, in 2021, NRG acquired Direct Energy, a subsidiary of Centrica. The $3.72 billion acquisition added three million customers to NRG’s retail portfolio, while solidifying its integrated business model.

Morgan Stanley analyst Stephen Byrd has reiterated a Buy rating on the stock, while decreasing the price target to $46 from $47.

Overall, the Street has a Hold consensus rating on the stock based on a Buy and five Holds. The average NRG Energy price target of $42.50 implies the stock is fairly priced at current levels after the recent rally in the stock.

Additionally, TipRanks data indicates hedge funds have lapped up 253,200 shares of NRG in the last quarter based on the activities of eight hedge funds.

Furthermore, the stock offers a forward dividend yield of 3.38%. Investors have been cognizant of this fact as TipRanks data shows the number of portfolios holding NRG has risen by 9.3% in the last 30 days, at the time of writing, indicating very positive investor sentiment for NRG.

Vistra Corp (VST)

The second name on our list, Vistra Corp, has been steadily ticking northward and has gained 66.3% over the past 12 months.

Shares of this integrated retail electricity and power generation company rose nearly 4.8% on May 6, to hit a 52-week high, after it narrowed its first-quarter loss.

Vistra has a presence in 20 states and caters to about 4.3 million residential, commercial, and industrial retail customers. It has a capacity of 39,000 MW with a portfolio that includes natural gas, nuclear, solar, and battery energy storage facilities.

For Q1, revenue declined 2.6% year-over-year to $3.13 billion, missing estimates by $235.8 million. The net loss decreased to $284 million from $2.04 billion a year ago. The loss in the year-ago period was attributed to the negative impact of winter storm Uri.

Additionally, the company reaffirmed its 2022 guidance, upped its second-quarter dividend by about 18%, and reduced its number of outstanding shares by about 10.5% under its $2 billion stock buyback program. A further $805 million remains under this stock buyback program.

Curt Morgan, CEO of Vistra, said, “We are executing on a comprehensive hedging strategy to capitalize on the beneficial power and commodities markets that are expected to provide significant value to Vistra in 2023 and beyond, and are continuing the advancement of our capital allocation priorities, returning capital through stock repurchases and paying a meaningful and growing dividend.”

The company is in the midst of a transition, with Jim Burke slated to take over as CEO on August 1.

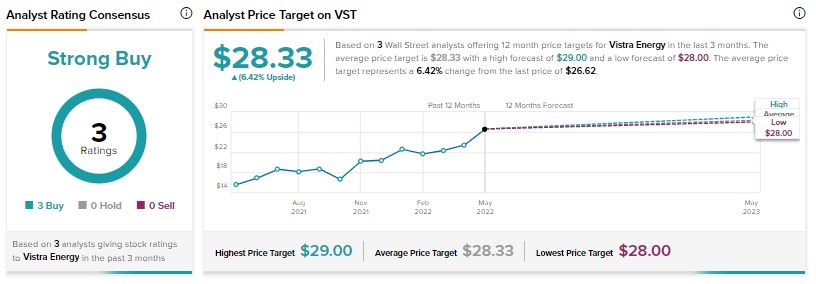

RBC Capital analyst Shelby Tucker has reiterated a Buy rating on the stock alongside a price target of $28. Overall, the Street has a Strong Buy Consensus rating on Vistra based on three unanimous Buys. At the time of writing, the average Vistra price target was $28.33, which implies a potential upside of 6.4%.

While hedge funds have decreased holdings in the stock by 165,900 shares in the last quarter, retail investors are very positive about the stock. At the time of writing, TipRanks data indicates the number of portfolios holding Vistra has increased by 4% in the past 30 days, with virtually all of this increase coming from investors who are under the age of 35.

Closing Note

As the demand for power keeps increasing in the U.S., power generation capacity needs to keep pace. Additionally, as the country moves away from conventional sources of energy, battery storage capacity additions will continue to gain emphasis. Amid this trend, both Vistra and NRG stand to gain in the coming periods.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure

Related News:

Crown Castle Stock: Too Pricey to Hide In

Is BHP Stock Worth Holding Despite Bearish Sentiment?

United Parcel Service Stock: Satisfactory Total-Return Prospects