A slowdown in its China business and macro and geopolitical concerns have weighed on Nike’s (NYSE:NKE) recent performance. Moreover, higher input costs due to the ongoing supply-chain headwinds remained a drag.

Given the challenges, Nike stock is trading in the red and is down about 16.7% year-to-date.

Now What?

It’s worth noting that Nike is witnessing an improvement in its business. During the most recent quarterly conference call, Nike CFO Matt Friend stated that in China, the company witnessed an improvement in full-price sales compared to the prior period, which is encouraging. Meanwhile, Nike’s China business showed sequential improvement, with the rate of decline decelerating on a quarter-over-quarter basis.

Moreover, Nike expects its China business to show further improvement on the back of higher demand driving full-price sales.

On the supply-chain front, Nike stated that its factories in Vietnam and entire supplier base are operational. Moreover, inventory supply has started to improve across all geographies. Furthermore, strong demand for its products, improving full-price sales, and strategic pricing will likely help counter higher product costs.

In response to Nike’s recent quarterly performance, Jefferies analyst Randal Konik stated that ongoing supply-chain challenges could continue to hurt its margins. However, he highlighted that “inventory supply levels are improving,” which is positive.

Konik is bullish on Nike stock and sees a favorable risk/reward scenario at current levels. Supporting his bullish view, Konik stated, “Despite Covid issues impacting all companies, NKE is executing well.” The analyst is upbeat about Nike’s business and brand amid a growing emphasis on health and wellness. He added that Nike’s increased focus on digital “should lead to share gains ahead.”

Along with Konik, Guggenheim’s Robert Drbul is also bullish on NKE stock. Drbul stated, “While there remains heightened uncertainty around COVID-19, we expect another sequential improvement in 4Q22 revenues for Nike in China.”

The analyst highlighted a higher full-price sales mix, strong demand, and improvements in inventory supply as positives.

Bottom Line

Nike is executing well despite its challenges. Further, its strong brand power, strength in the direct-to-consumer business, an improved sales mix, the recovery in China, and normalization in inventory supply bode well for growth. However, uncertainty related to COVID and the current geopolitical environment could play spoilsport in the short term.

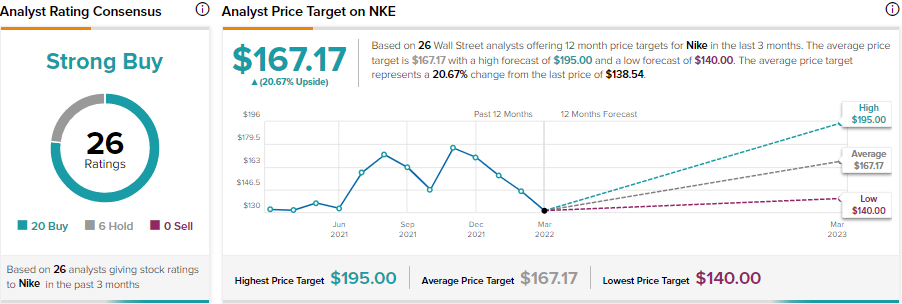

Nevertheless, Wall Street is bullish on NKE with 20 Buy and 6 Hold recommendations for a Strong Buy consensus rating. Further, the average Nike price target of $167.17 implies 20.7% upside potential to current levels.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure