Mastercard stock (NYSE:MA) keeps reaching new all-time highs. The card payment processor giant continues to enjoy unstoppable momentum despite the tough macroeconomic environment. Strong consumer spending, inflation, and the ever-persisting theme of society going cashless are three key catalysts powering Mastercard’s strong top- and bottom-line growth. This trend appears set to continue, suggesting more upside ahead despite the stock’s strong rally lately. Hence, I’m bullish on MA stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Mastercard’s Momentum: No Signs of Slowing Down

Mastercard’s impressive momentum is showing no signs of slowing down. The company is currently benefiting from three key factors: strong consumer spending, rising prices (inflation), and the ongoing shift towards a cashless society.

In its most recent Q2 results, Mastercard achieved a notable 15% increase in net revenue. This growth was driven by the combination of these three factors, along with the recovery of cross-border travel. The company’s value-added services and solutions also played a significant role in boosting its results.

Globally, there was 12% growth in the total dollar volume of transactions and a 14% increase in purchase volume compared to the same period last year. While the U.S. saw a respectable 5.8% rise in purchase volume, Europe and Latin America experienced substantial growth, with increases of 25.3% and 17.4%, respectively. This growth is directly linked to the continued recovery of international travel in a post-COVID-19 world, whether for business or leisure.

Mastercard’s strong performance in Europe and Latin America is also tied to the impact of inflation. Here’s the simple explanation: in an inflationary environment, the prices of goods and services generally go up. This means that each transaction processed by Mastercard is likely to have a higher value compared to times of low inflation or deflation. Since Mastercard’s fees are calculated as a percentage of the transaction amount, higher transaction values translate to increased revenue for the company.

In August, the Eurozone experienced inflation of 5.3%, while the U.K. saw an inflation rate of 6.8%. Other major European markets, such as Sweden and Poland, saw inflation rates of 7.5% and 10.1%, respectively, for the period. In more established Latin American markets like Brazil and Mexico, inflation stood at 4.6% each in August despite gradual easing. This shows how Mastercard benefits directly from inflation, seeing a significant boost in its growth, from mid-single digits to low-double digits, from this one factor alone.

Although inflation is expected to continue its gradual decline in the future, it seems that robust consumer spending and international travel will likely remain strong. As someone living near the Acropolis, I can attest that tourism has reached extraordinary levels, with visitors waiting in line for up to two hours to catch a glimpse of this iconic landmark.

While this is anecdotal evidence, it aligns with numerous reports indicating that Europe witnessed unprecedented levels of tourism during this summer season, primarily due to a surge in American travelers. As we transition from summer to winter, there doesn’t seem to be any compelling reason why this trend wouldn’t persist for the popular winter destinations. Cross-border fees are super profitable for Mastercard, which backs the stock’s optimistic outlook.

Fiscal 2023: Another Year of Record Profits

Following very strong momentum during the first half of Fiscal 2023, Mastercard has positioned itself for another year of record-breaking profits. Remember that Mastercard’s revenues can be essentially viewed as royalties because the company’s gross margin is literally 100%. With a great chunk of revenue flowing directly to the bottom line, Mastercard’s profits are easily boosted as its revenues grow.

In particular, in Q2, Mastercard enjoyed a notable increase in net income, largely due to significant revenue growth and controlled expense expansion. The net income margin rose impressively to 45.4%, a considerable increase from 41.4% the previous year. This surge, coupled with revenue growth, caused its net income to escalate by 25%, reaching $2.8 billion. Additionally, EPS witnessed substantial growth of 28%, a progression further accelerated by a reduced share count due to Mastercard’s ongoing buybacks.

In the latter half of the year, management anticipates that net revenue growth will persist within the low-teens range, excluding any contributions from acquisitions or exceptional items. Considering this projection alongside Mastercard’s H1-2023 performance, Wall Street foresees that Mastercard’s EPS for Fiscal 2023 will land at $12.16. This figure implies a year-over-year growth rate of 14.2% and another milestone for the payments processing behemoth.

Is MA Stock a Buy, According to Analysts?

As far as Wall Street’s view on the stock goes, Mastercard boasts a Strong Buy consensus rating based on 18 Buy and one Hold recommendation assigned in the past three months. At $466.18, the average Mastercard stock price target suggests 12.1% upside potential.

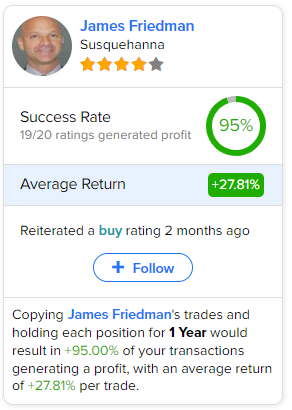

If you’re wondering which analyst you should follow if you want to buy and sell MA stock, the most profitable analyst covering the stock (on a one-year timeframe) is James Friedman from Susquehanna, with an average return of 27.81% per rating and a 95% success rate.

The Takeaway

All in all, Mastercard’s unstoppable momentum, driven by strong consumer spending, inflation, and the shift toward a cashless society, remains undeterred. Its Q2 results showcased substantial revenue growth, with international travel recovery and inflation playing pivotal roles. Looking ahead, Fiscal 2023 promises another year of record profits. In that regard, I can see more upside ahead for MA stock.

Sure, based on Wall Street’s estimate, shares appear to be trading at a rather hefty forward P/E of about 34x. However, taking into account the company’s unparalleled moat (duopoly along with Visa (NYSE:V)), double-digit EPS growth, and commitment to rewarding shareholders, I believe that Mastercard stock is quite fairly valued. Therefore, I believe there is no cause for concern in holding the stock, even as it has recently achieved record highs.