Much-maligned Citigroup (NYSE:C) stock has rallied more than 40% off of its 52-week low. However, even after this rally, there’s still plenty of room for additional upside. I’m bullish on shares of the fourth-largest bank in the United States based on its incredibly cheap valuation, above-average dividend yield, and the steady progress the company is making on reducing expenses. Furthermore, several highly-regarded value investors have positions in the stock and seem to support management and its turnaround plans.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Signs That a Turnaround Is Underway

Citigroup stock won’t be winning many popularity contests any time soon. While there were plenty of ups and downs, the stock has treaded water over the past five years, ultimately remaining flat during a time frame in which the broader market has surged.

Part of the reason for this lackluster performance is that the bank has produced disappointing results. Citigroup’s recently-reported fourth-quarter results followed this trend, as the bank posted a $1.8 billion loss, which arose from a smorgasbord of charges related to overseas risks.

However, there were also signs of life, and overall, investors and analysts had a positive reaction to the report. For one thing, management expects $80-81 billion in revenue, a 4% increase versus full-year revenue for 2023.

Furthermore, the company is targeting significant reductions in expenses and making slow but steady progress toward this goal. Management guided for $53.5-53.8 billion in expenses in 2024, which would represent 1% in savings from last year’s $54.3 billion. Further out, the company is targeting a more ambitious reduction to $51-53 billion.

The company previously announced a program to cut headcount by approximately 10% and has started making layoffs and eliminating leadership roles, so it’s serious about these goals.

The outlook was well-received by analysts. Wells Fargo’s (NYSE:WFC) Mike Mayo calls Citi his top bank pick in the midst of a “multi-year inflection” and maintains an Overweight rating and $70 price target on the stock. Meanwhile, Bank of America (NYSE:BAC) maintained its Buy rating on the stock and increased its price target from $60 to $65. Similarly, Oppenheimer maintained its Outperform rating and increased its price target to a more aggressive $93, up from $85.

Big Investors Believe in the Turnaround

Several prominent value investors believe in the management team and the turnaround play.

During the most recent quarter, Edgar Wachenheim III’s Greenhaven Associates increased its Citigroup position by 22%, making it the firm’s third-largest holding. As of the 13F filing, shares of Citigroup accounted for nearly 9% of Greenhaven’s portfolio.

Wachenheim recently told Barron’s, “We strongly believe that Citigroup’s shares are deeply undervalued because the bank and its management are much better and stronger than their reputations.” Wachenheim went on to say, “We hear from a number of sources that Jane Fraser is doing an excellent job as Citi’s relatively new CEO.”

That’s a pretty convincing vote of confidence, and Warren Buffett seems to agree. At a recent lunch with Fraser, Buffett reportedly told the new CEO to keep going with her cost-cutting and turnaround plans. Buffett’s Berkshire Hathaway (NYSE:BRK.B) is a major shareholder that owns over 55 million shares of the bank as of its last 13F filing.

Resoundingly Cheap

In addition to the turnaround efforts, value investors like Wachenheim and Buffett clearly know that shares of Citigroup are incredibly cheap. Not only do they trade at just nine times projected 2024 earnings, a significant discount to the broader market, but they also trade at a massive discount to book value. Shares of the bank trade at a paltry 0.56 times book value.

It’s hard to overstate how cheap this is. It means that Citigroup currently trades for slightly more than half of what it would be worth if all of its assets were liquidated today.

Citigroup is also far cheaper than its “big four” banking peers, Bank of America, Wells Fargo, and JPMorgan Chase (NYSE:JPM), based on this metric. Bank of America shares trade at its book value, while shares of Wells Fargo and JPMorgan Chase trade above their book values. Some discount to these stocks is certainly warranted as they have produced better results than Citigroup, but the discount illustrates that there is room for upside ahead.

This ultra-low price-to-book value ratio gives investors significant potential upside and a nice margin of safety when buying shares. The aforementioned Wachenheim told Barron’s that he believes tangible book value will average $105-$110 in 2026 and that if shares “merely sell at book value and at 10 times normal earnings, an investor can double his or her money over the next two or so years.”

Solid Dividend Play

In addition to this staggeringly cheap valuation, Citigroup also looks attractive based on its dividend yield. Shares currently yield 3.9%, more than double the yield of the S&P 500 (SPX). Citigroup’s dividend yield is also higher than any of its big four banking peers, all of which yield below 3%.

Citigroup has paid a dividend for 11 years in a row, and the dividend should be safe, as the stock’s dividend payout ratio is a conservative 37.2%.

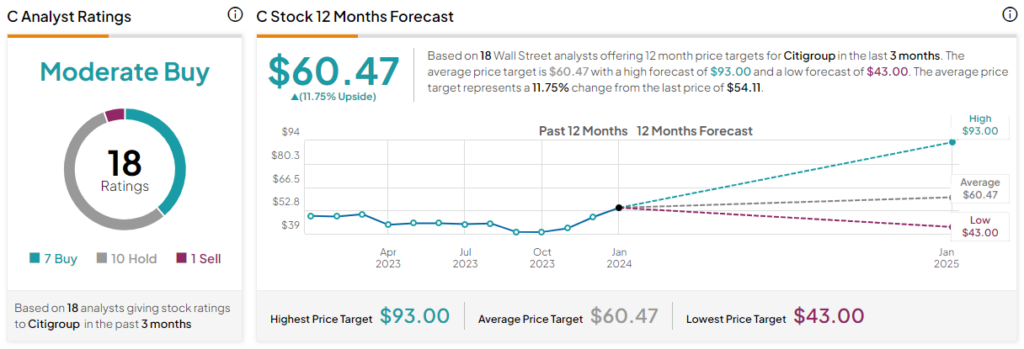

Is C Stock a Buy, According to Analysts?

Turning to Wall Street, Citigroup earns a Moderate Buy consensus rating based on seven Buys, 10 Holds, and one Sell rating assigned in the past three months. The average C stock price target of $60.47 implies 11.75% upside potential.

Looking Ahead

Citigroup has been an underperformer, but the stock is picking up momentum, and several prominent investors appear to believe in its turnaround potential. I’m bullish on the stock based on these plans, its ridiculously cheap price-to-book ratio, and its above-average dividend yield.