Quite frankly, the narrative regarding a popular financial technology (fintech) stalwart appears to be a stark one: if you’re buying shares of SoFi Technologies (NASDAQ:SOFI), you better pray for a soft landing. A soft landing refers to an economy’s transition from growth to slower growth, or stagnation, without plunging into a recession. Otherwise, the company faces significant risks that will not be easy to overcome. Therefore, I am bearish on SOFI stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

SOFI Slips after CART Stock IPO Disappoints

Just a few weeks ago, the narrative for SOFI stock stood on much more pleasant ground. At the time, the underlying fintech – which broadcasted ambitions to become a full-service financial institution – had great news for stakeholders. It was about to take its initial steps into the world of underwriting traditional initial public offerings (IPOs). Unfortunately, the move represented a sour note.

As TipRanks reporter Sirisha Bhogaraju noted, SoFi received approval to help underwrite the new listing of grocery delivery app Instacart (NASDAQ:CART). Following a long dearth of significant IPO activity, all eyes focused in on Instacart’s debut. By helping to launch its shares into the capital market, SoFi stood poised to prove that it could hang with the alpha dogs of finance.

However, the Instacart IPO has so far been a dud. Marking its public trading debut on September 19, CART has slipped more than 35% since then. Not surprisingly, SOFI stock – which earlier benefited from the hype – has also fallen by 3% during the same period.

On paper, just the mere fact that SoFi participated in the hotly anticipated IPO is a victory. To be sure, not just anyone can help underwrite a new listing. For a smaller firm like SoFi, it must prove to the lead underwriters that it can bring value to the table.

In many cases, the lightweight enterprise may offer a committed network of interested retail or institutional investors. In other situations, the entity may offer to absorb more risk by agreeing to hold more shares. Either way, it’s likely that SoFi had to pay to play, and that raises questions about the ongoing vitality of SOFI stock.

Worrisome Financial Exposure

More critically, SOFI stock suffers from worrisome financial exposure. On October 30, the fintech stalwart will release its earnings results for its fiscal third quarter. Probably, management will need to deliver a print that knocks the ball out of the park. If not, the underlying business could suffer quite badly.

In the company’s Q2 presentation, management revealed an arguably alarming data point. While total loan originations jumped to $4.38 billion from $3.57 billion in Q1, the vast majority of the loans stem from personal loans at $3.74 billion. That’s a huge problem because personal loans are unsecured. If the borrower can’t repay the loan, the lender is basically on the hook.

It’s an issue that came up in Q1 earlier this year. Back then, personal loans accounted for 82.7% of total loans. In the latest Q2 report, this exposure increased to 85.4%.

To be fair, if the economy was decisively on an upward trajectory – and the common household could easily afford the necessities of life along with some discretionary luxuries – the personal loan exposure wouldn’t be such a worrisome figure. With a strong labor market, companies are continuing to lay off their workers. It’s this kind of contradiction that warrants vigilance toward exposure to unsecured loans.

Now, so far, SOFI stock has gained almost 86% since the start of the year. Investors don’t appear too worried about the exposure. Nevertheless, if policymakers can’t control inflation, this vulnerability could bite back hard.

Strong Labor Market May be a Headwind

Last Friday, the equities sector ended the week on a high note, thanks in large part to the September jobs report. While such a positive surprise sounds great intuitively, in context, it could cause problems for the economy. Subsequently, that would not be good news for SOFI stock.

Specifically, the Federal Reserve has struggled with containing stubbornly high inflation. So, more people having more money to spend fundamentally exacerbates the acceleration of consumer prices. Thus, the Fed may be forced to raise borrowing costs, adding another wrinkle to SOFI’s unsecured personal loans exposure.

Is SOFI Stock a Buy, According to Analysts?

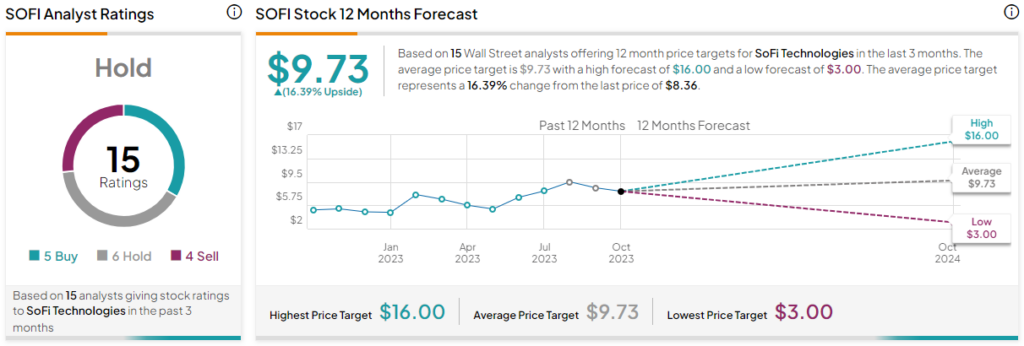

Turning to Wall Street, SOFI stock has a Hold consensus rating based on five Buys, six Holds, and four Sell ratings. The average SOFI price target is $9.73, implying 16.4% upside potential.

The Takeaway

While SOFI stock has been a Wall Street darling for its underlying ambitions, circumstances have conspired against the fintech. First, the much-anticipated IPO recovery may turn out to be a dud. Second, SoFi itself is deeply exposed to personal loans, products that risk going bad if the economy suffers. Therefore, caution is key.