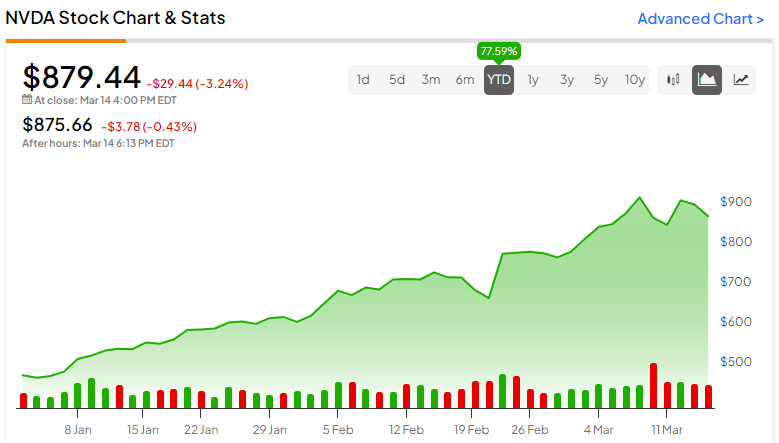

Chipmaker and AI prodigy Nvidia (NASDAQ:NVDA) continues its unstoppable upward journey, having more than tripled in value in 2023 and up about 78% year-to-date. The recent Q4 beat was spectacular and drove NVDA to its all-time highs. Being at the helm of the AI revolution, my bullish stance on NVDA remains. I am confident in its long-term potential for growth, driven by the artificial intelligence (AI) boom and its relatively favorable valuation. Hence, I will buy the stock at current levels.

NVDA Posts Blowout Q4 Earnings Yet Again

Now the third largest company in the world, Nvidia posted yet another blowout Q4 result on February 21, driven by accelerated computing and generative AI momentum. Adjusted earnings of $5.16 per share handily beat the analysts’ estimates of $4.59 per share. Also, the figure came in much higher (+486%) than the Fiscal Q4-2023 (ended January 2023) figure of $0.88 per share.

Impressively, Q4 revenue jumped 265% year-over-year to $22.1 billion, surpassing the consensus estimate of $20.5 billion. On top of that, its adjusted gross margin expanded 10.6 percentage points to 76.7% from 66.1% a year ago.

Importantly, NVDA’s crown-jewel segment, Data Center revenues, more than trebled year-over-year to $47.5 billion in Fiscal 2024. Q4 revenues for the segment also saw remarkable growth, increasing by 409% year-over-year to $18.4 billion.

As expected, revenues declined in China due to the U.S. export control restrictions. During the earnings call, management affirmed that China represented only a mid-single-digit percentage of Data Center revenue in Q4 versus 20-25% on an average basis over the last few quarters.

Looking ahead, the Q1 guidance appears promising, with revenues expected to hover around $24 billion. Adjusted gross margins are forecasted to be around 77%.

Exuberating great optimism for the future, CEO Jensen Huang commented during the call, “We’re at the beginning of two industry-wide transitions and both of them are industry-wide. The first one is a transition from general to accelerated computing… [and] a second industry-wide transition called generative AI.”

NVDA’s Long-Term Trajectory Remains Impressive

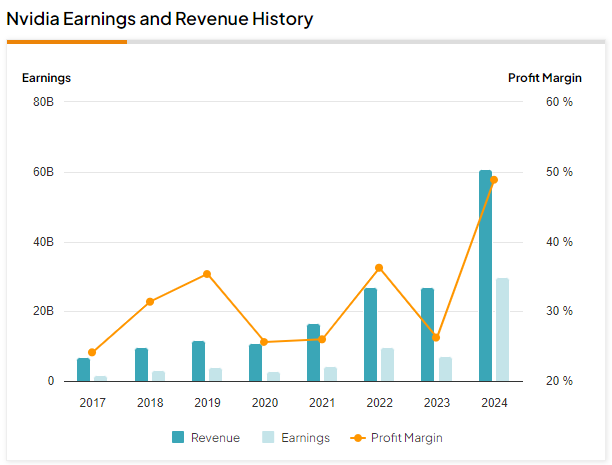

NVDA is Wall Street’s favorite for a good reason. Over the last six years, Nvidia’s revenues have skyrocketed by nearly 9x, from $6.91 billion in FY2017 to $60.9 billion in FY2024 (see below). What’s even more applaudable is that its earnings have grown by 18x from $1.67 billion to $29.8 billion over the same period, thanks to its rising profit margins. This data instills in me a profound sense of confidence in NVDA’s strong business fundamentals and its anticipated growth trajectory, driven by AI.

According to Wall Street estimates, NVDA is projected to achieve a net profit of $64.3 billion in Fiscal 2025, doubling from the $32.3 billion reported in the recently concluded Fiscal 2024. Furthermore, revenues are expected to surpass the monumental $100 billion milestone. These remarkable growth expectations provide compelling reasons to continue investing in this AI giant, especially considering that the growth narrative of disruptive generative AI is only just beginning.

NVDA Could Likely Go for a Stock Split

Inching closer to the $1,000 milestone price mark, many Wall Street analysts opine that a stock split could occur in the next year or so. NVDA underwent a 4:1 stock split in May 2021, when it was priced at approximately $600. This move facilitated easier access for smaller retail investors to purchase the stock. While a stock split doesn’t inherently alter the company’s valuation or fundamentals, it does broaden its investor base by attracting smaller investors.

Other prominent companies that have opted for stock splits include EV maker Tesla (NASDAQ:TSLA) (in 2020 and 2022) and Apple (NASDAQ:AAPL), Amazon (NASDAQ:AMZN), and Alphabet (NASDAQ:GOOGL). Therefore, it is likely that NVDA may consider another stock split in the near future.

NVDA Valuation Still Isn’t Expensive, Given Its Earnings Prowess

Having overtaken Amazon by market capitalization and on the verge of eclipsing Apple’s market cap, many investors are hesitant to purchase NVDA stock amid its remarkable rally and concerns about overvaluation.

On the contrary, however, NVDA stock is not expensive at all. Currently, it’s trading at an attractive forward P/E ratio of 36.9x (based on FY2025 earnings expectations). This is relatively cheaper than the multiples of its peer group. For instance, U.S.-based semiconductor company Advanced Micro Devices (NASDAQ:AMD) is trading at a forward P/E of 53.4x.

Furthermore, its current valuation reflects a discount from its five-year average of 46x. These are attractive discount levels and likely present a great buying opportunity, given the supernormal growth potential for the AI market titan NVDA.

Is NVDA Stock a Buy, According to Analysts?

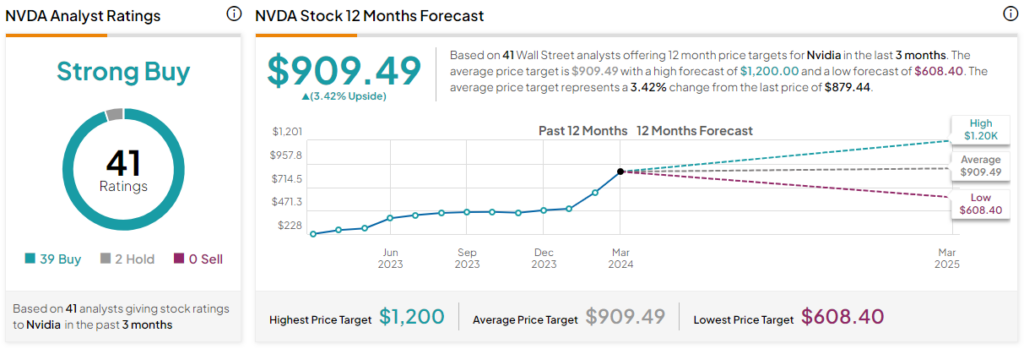

NVDA stands as an invincible force, a stock that garners widespread attention. With 39 Buys and two Hold ratings from analysts in the last three months, the consensus rating is unmistakably a Strong Buy. Nonetheless, the average Nvidia stock target price of $909.49 suggests that the shares will return 3.4% over the next year.

Interestingly, the average target price has been increasing incredibly as analysts strive to match NVDA’s continuous record-breaking highs month after month. It has increased from $661 just three months ago to $909.

Conclusion: Consider Buying NVDA for Its Long-Term AI Potential

NVDA stock is poised to soar to unprecedented heights, propelled by the extraordinary growth expectations within the AI space. As an industry frontrunner, NVDA maintains a substantial lead over its competitors, boasting an almost monopolistic position with an approximately 80% market share in AI chips. This dominant position ensures a robust moat and solidifies its grip on the flourishing AI landscape.

The insatiable demand for all things AI far outpaces the available supply, underscoring the potential for accelerated computing and generative AI adoption across various industries and regions. This trend is anticipated to be a primary driver of revenue and earnings growth for NVDA in the years ahead.

With NVDA’s highly anticipated live GTC conference scheduled for March 18-21, my bullish outlook on the company remains steadfast, prompting me to purchase shares at their current levels.