The stock market presents a somewhat confusing picture for now. The main indexes are all steeply down for the year so far – with losses of 16% on the S&P 500 and 25% on the NASDAQ. Drops of this magnitude come with a caveat, however: it’s inevitable that some fundamentally sound stocks are seeing drops in share price just due to the overall market’s downward trend.

Indeed, Wall Street’s analysts are seeing plenty, in their words, attractive entry points — beaten-down stocks that are primed for gains despite the challenging market environment. We’ve used the TipRanks database to pull up the details on three such stocks. Let’s dive in.

Varonis Systems (VRNS)

We’ll start in the cybersecurity sector, with Varonis Systems. The company provides automated data protection, an essential service in the modern digital economy. Varonis’ products promote detection and defeat of online threats like ransomware, while also tracking digital behavior and abnormal user activity to identify potential cyberattacks.

In the recently reported 1Q22, Varonis showed powerful growth in multiple key metrics. These included 29% year-over-year revenue growth, 32% annualized recurring revenue growth, and 53% growth in subscription revenue. The company’s top line came in at $96.3 million. Varonis managed these increases in what is, historically, its lowest-performing calendar quarter; the company typically sees revenues and other metrics start low in Q1 and increase to the end of the calendar year.

While the Q1 report was generally good, the quarterly net loss, of 9 cents per share, beat the forecast of 10 cents – but was deeper than the year-ago EPS loss of 8 cents. In addition, while management’s revenue guidance for 2022 represents a 25% increase at the midpoint, the low end is still below expectations, raising the possibility that the company could underperform.

Investors should note that Varonis shares are down 57% from the peak they hit in September last year. At least one analyst, however, believes that now is the time to buy the dip.

Andrew Nowinski, 5-star analyst from Wells Fargo, rates VRNS an Overweight (i.e. Buy), while his $60 price target indicates room for 88.5% upside by this time next year. (To watch Nowinski’s track record, click here)

“[Varonis’] pullback creates attractive entry point in light of improving demand trends… Over the last 6 months, shares of VRNS have declined significantly more than the NASDAQ. During this period, the EV/CY23E Sales multiple has declined from 12x to 7.9x (based on consensus estimates), and shares now trading below the peer group average (7.9x vs. 8.6x for the peer group). From a revenue growth perspective, the peer group average is only 23% in CY23, though we believe Varonis has the potential to continue growing revenue in the 30% range, which would be a premium to the peer group average,” Nowinski opined.

Tech firms like Varonis tend to pick up plenty of analyst attention, and this company has 14 recent analyst reviews. These include 12 Buys and only 2 Holds, for a Strong Buy consensus rating. Meanwhile, the average price target of $56.43 implies an upside of ~77% from the current share price of $31.83. (See Varonis stock forecast on TipRanks)

Aaon, Inc. (AAON)

For the second stock on our list, we’ll move over to HVAC. Aaon designs, produces, and markets a range of equipment for indoor climate control and ventilation, including air handlers, chillers, condensers, heat pumps, and control units. The company markets to both commercial scale and residential customers, and is based in Tulsa, Oklahoma.

So far this year, Aaon’s shares are down 32%, even as company revenues are growing year-over-year. In 1Q22, the company had a top line of $182.8 million, up a robust 57% from the year-ago quarter. The work backlog in Q1 came to $461.4 million, a company record – and up by 377% from 1Q21.

All of this indicates a company that is seeing increasing and accelerating growth, a story that caught the attention of D.A. Davidson’s 5-star analyst Brent Thielman.

“Margins were near our expectations and up considerably from 4Q (suggesting AAON is managing today’s supply/inflation challenges more effectively); while the bigger story is massive growth and order activity fueling a significant build in backlog. These order trends don’t appear to be abating. While we’ve historically yielded to valuation, the recent pullback coupled with what looks to be solid double-digit growth in 2022/2023 lends a more attractive entry point,” Thielman noted.

These comments support Thielman’s Buy rating on AAON shares, and his $70 price target suggests that the stock has an upside potential of ~30% over the next 12 months. (To watch Thielman’s track record, click here)

Blue collar industrials don’t hold the same cachet as high techs, and Aaon only has two recent analyst reviews. Both are positive, however, making the Moderate Buy consensus rating unanimous. The shares are trading for $54 and their $71 average target implies a one-year upside of 32% from current levels. (See AAON stock forecast on TipRanks)

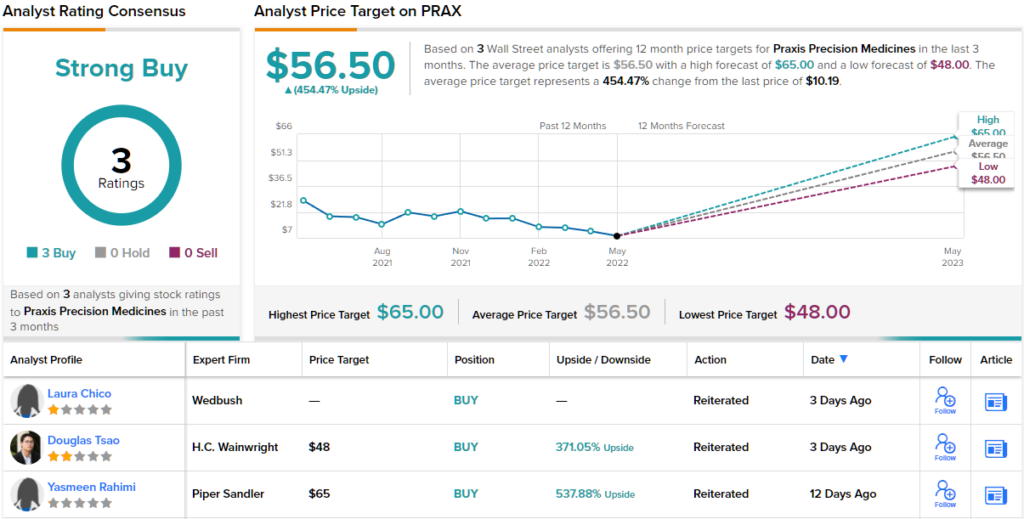

Praxis Precision Medicines (PRAX)

Last but not least is Praxis Precision Medicines, a clinical-stage biopharmaceutic firm developing new treatments for central nervous system disorders. These are a serious class of diseases, causing everything from anxiety and depression to ongoing seizures; Praxis is working on novel treatments, approaching them through genetic research.

The company currently has several ongoing clinical trial programs, a highly desirable position for a biopharma to hold. The most advanced drug candidate is PRAX-114, a potential treatment for both major depressive disorder (MDD) and post-traumatic stress disorder (PTSD). Praxis expects to release data from two clinical trials of PRAX-114 on MDD later this year – the Aria study, a Phase 2/3 placebo controlled monotherapy trial, should show topline results in June, while the Acapella Phase 2 dose-ranging study is expected to release results in 3Q22. Praxis anticipates initiating a Phase 3 study of this drug candidate against MDD sometime during Q4 of this year.

On the PTSD side, PRAX-114 is undergoing a Phase 2 safety, tolerability, and efficacy trial. The company expects to make results available during 2H22.

Praxis has another major research program at the Phase 2 level – PRAX-944 is a drug candidate designed to treat essential tremors. In data released earlier this month, Praxis announced that the drug candidate had demonstrated clinically significant effect in functional improvement of patients with essential tremor. The results came from Part B of a Phase 2a study. The Phase 2b dose ranging study, with 112 patients, is ongoing.

Finally, Praxis has an ongoing program in the treatment of epilepsy. The leading candidate here, PRAX-562, is scheduled to begin a Phase 2 trial in 2H22, and the preclinical drug candidate PRAX-628 will begin Phase 1 testing before the end of this year.

Like many clinical-stage biopharma companies, Praxis’ shares are highly volatile; the company’s stock is down 48% so far this year. However, Wedbush analyst Laura believes PRAX is a solid risk-reward proposition at current levels.

Chico notes the multiplicity of research tracks as a positive for investors to consider, but points out PRAX-114 as the key factor going forward.

“We continue to see PRAX holding a unique collection of wholly-owned assets. Further execution on certain proof-of-concept studies such as PRAX-114 in ET can only help to broaden the optionality. With the equity markets in disarray, we do detect hesitancy into the upcoming ARIA readout, in part due to earlier data points from SAGE’s zuranolone in major depressive disorder,” Chico noted.

“For our part, we see distinctions on both the molecules themselves, as well as in the clinical trial design features across the programs. Additionally, with management’s commentary indicating ARIA recruitment demographics appear to be tying with their prior expectations, we think this is a positive signal. Simply put, we see current levels offering an attractive entry point,” the analyst added.

To this end, Chico sets an Outperform (i.e. Buy) rating on PRAX shares, and her price target, of $34, indicates her belief in a 233% one-year upside potential (To watch Chico’s track record, click here)

Overall, all three of the recent analyst reviews on Praxis are positive, for a unanimous Strong Buy consensus rating. The stock’s average price target of $56.50 implies a powerful 454% upside from the current share price of $10.19. (See PRAX stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.