In this piece, I evaluated two lending stocks: Affirm Holdings (AFRM) and SoFi Technologies (SOFI). A closer look suggests a bearish view for Affirm and a bullish view for SoFi.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Affirm Holdings provides an online platform for digital commerce consisting of point-of-sale installment loans for consumers, merchant commerce solutions, and a consumer-facing app. Meanwhile, SoFi offers lending and financial products ranging from student loans to mortgages and personal loans.

In terms of price performance, Affirm Holdings stock has tumbled 18% year-to-date, but it’s still up 83% over the past year despite the recent decline. Similarly, shares of SoFi Technologies have plunged 24% year-to-date, although that decline dragged their one-year return to a negative 14%.

With such a dramatic difference in their 12-month returns, it’s no surprise that their valuations are quite different.

Since neither company is profitable, we compare their price-to-sales (P/S) ratios to gauge their valuations against each other and that of their industry. For comparison, the diversified financials industry is trading at a P/S of 4x, versus its three-year average of 2.8x.

Since Affirm and SoFi are financial firms, we also consider their price-to-book-value (P/BV) ratios. Anything at a P/BV of 1x or below is often considered potentially undervalued.

Affirm Holdings

At a P/S of 5.6x and a P/BV of 4.7x, Affirm Holdings immediately looks overvalued relative to its industry and the value of its assets. The stock surged more than 30% following its last earnings report on August 28, adding fuel to the argument that Affirm may be overvalued. Thus, a bearish view seems appropriate, at least until a pullback occurs.

In fact, a reversal may be closer than one might think. Affirm’s Relative Strength Index stands at 73.7, suggesting it’s in overbought territory and that a correction might be just around the corner. However, at the current valuations, Affirm’s valuation appears to be getting ahead of itself, meaning the company requires significant growth before it will be priced right at current levels.

It’s not all bad news for Affirm, though. The company did put up some impressive growth in the latest quarter, including a 48% jump in revenue and a net loss that narrowed from $206 million in the year-ago quarter to $45.1 million in the latest quarter.

Additionally, Affirm CEO Max Levchin told shareholders in a letter that they recently set a goal of achieving operating profitability on a GAAP (generally accepted accounting principles) basis by the fiscal fourth quarter of 2025.

Nonetheless, with zero profits in the near term and quarterly revenue of $659 million, investors should question whether Affirm truly deserves a market capitalization of $12.6 billion.

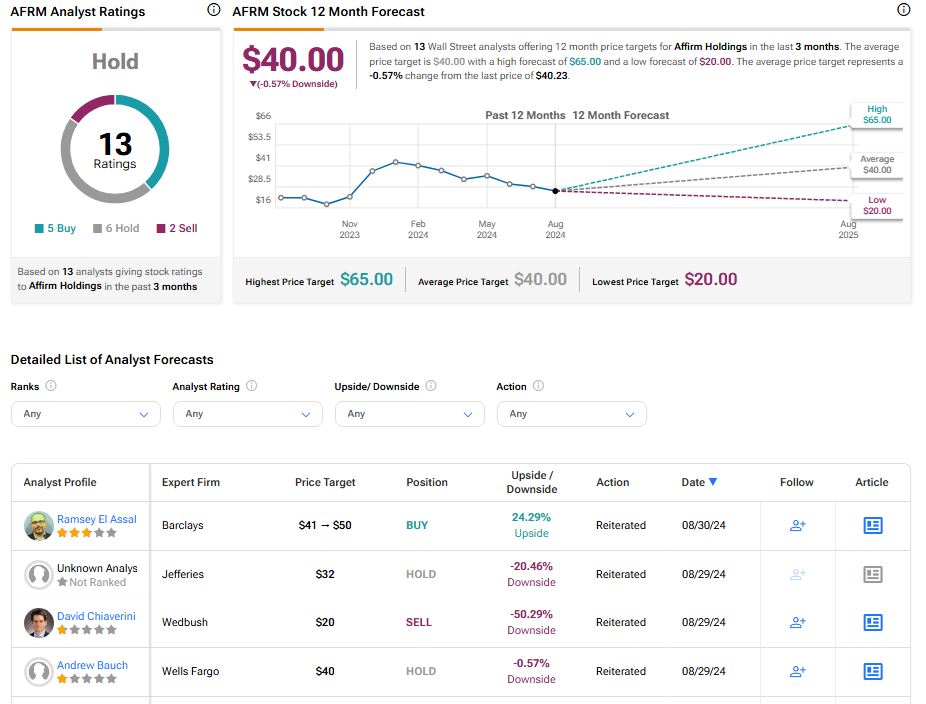

What Is the Price Target for AFRM Stock?

Affirm Holdings has a Hold consensus rating based on five Buys, six Holds, and two Sell ratings assigned over the last three months. At $40, the average Affirm Holdings stock price target implies a downside potential of 0.57%.

SoFi Technologies

At a P/S of 3.4x and a P/BV of 1.4x, SoFi looks far more reasonably valued. Given the recent dip in its stock price and the chance at profitability this year, a cautionary bullish view seems appropriate.

SoFi posted its third consecutive quarter of profits in July, demonstrating steady progress toward its goal of full-year GAAP profitability in 2024. Although that net income was slim, at $17.4 million on $587 million in revenue, SoFi is displaying some promising signs of stability.

The company’s stock has faced challenges this year due to concerns over interest rates. While lower rates could help SoFi attract more loans, they could also squeeze the company’s profit margins.

Nevertheless, one top investor recently noted that SoFi has continued to grow its customer base, even in a high interest-rate environment, which typically leads to a dramatic drop in lending.

This same investor thinks that higher volumes should enable SoFi to make up for lower margins over the long term, and I tend to agree. Thus, this looks like a solid buy-the-dip opportunity, though short-term volatility remains a possibility.

What Is the Price Target for SOFI Stock?

SoFi Technologies has a Hold consensus rating based on five Buys, seven Holds, and three Sell ratings assigned over the last three months. At $8.27, the average SoFi Technologies stock price target implies upside potential of 10.56%.

Conclusion: Bearish on AFRM, Bullish on SOFI

Although Affirm and SoFi utilize two different lending models to place money into the hands of consumers, those different models make SoFi look like the better, more stable long-term play. The buy now, pay later model faces weakness during times when purchases are down, but SoFi managed to buck the trend of reduced lending even when interest rates were high.

Additionally, Affirm still has to grow into its current valuation, while SoFi looks fairly valued and has significant upside potential in the near term, especially if it achieves full-year profitability, likely by the end of 2024. However, investors may need to be patient with SoFi as it moves forward into profitability, given the potential for increased volatility in its stock price due to interest rate swings.