It’s been a rocky and muted recovery for many of the top travel and leisure stocks that fell at the hands of the coronavirus crisis. America may have returned to normal following the lockdown days. Still, other parts of the globe (like China and its zero-COVID policies) are taking strict measures to limit the spread of COVID-19. Due to its exposure in the Shanghai region, Disney (NYSE:DIS) is one company that’s taken a harder hit due to recent lockdowns. In this piece, we’ll check in on three travel and leisure stocks, DIS, BKNG, DAL, that retain their “Strong Buy” ratings from Wall Street analysts.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Each play has considerable upside in 2023 as firms look to move past lingering headwinds from COVID-19 and worsening macroeconomic conditions from higher interest rates.

Disney (NYSE:DIS)

Disney stock is back where it spent most of the early part of 2020. This week, long-time CEO Bob Iger made his return to the House of Mouse after the sudden ousting of Bob Chapek.

Undoubtedly, Chapek’s performance has been abysmal, even with COVID-19 headwinds considered. Shares of Disney rallied around 6% following news of Bob Iger‘s return. Iger is expected to stay on for at least two years. That should be enough time to turn the tides around and reverse the significant (and ineffective) changes put forth by Chapek.

Indeed, DIS stock has been a disaster under Chapek. With Iger back aboard, investors seem more enthused. Still, questions linger as to whether Iger is the right man to turn things around. He did make plenty of mistakes before he left when Disney stock was a sinking ship amid the 2020 stock market crash.

With rates on the rise and losses from streaming platform Disney+ mounting, Iger is likely to explore ways to enhance profitability prospects. Undoubtedly, Iger has his work cut out for him. With activist investors getting involved, Disney is sure to be a messy but major mover over the next year.

At below $100 per share, I think the stock is deeply undervalued when you consider the current catalysts (CEO change and activist involvement) in place. The stock trades at a palatable 2.2x sales. Sure, there’s tons of baggage and a worsening macro climate, but it’s tough to pass up on the legendary brand while it’s down and out. Whether Iger can fix Chapek’s mismanagement, though, remains to be seen.

What is the Price Target for DIS Stock?

Wall Street is confident in Disney. The average DIS stock price target of $122.25 entails 23.65% gains for the year ahead.

Booking Holdings (NASDAQ:BKNG)

Booking Holdings stock is another travel and leisure titan that’s crumbled under the pressure of the pandemic and looming recession. The stock is down around 26% from its all-time high just north of $2,000. Though the travel-booking scene is quite competitive, I do view Booking as one of the widest-moat players within the space.

Booking is a leader in the European market. Its heavy exposure to Europe comes with advantages. Most notably, the European market is better known for its smaller hotel chains compared to the U.S. or Canada, where big chains like Hilton (NYSE:HLT) are popular.

Booking can consolidate many smaller boutique hotels together on its platform that are harder to find via search engines. So, when it comes to Booking, there’s a discovery aspect that makes it a tougher platform for rivals to top.

With a recession on the way, travel demand could take a breather after its historic recovery from COVID-19. At 32.3x trailing earnings, BKNG stock still seems priced as though the coming recession won’t completely derail the recovery.

Despite economic uncertainties and a rich multiple, Booking is still a standout player that will be ready to roar once travel demand is ready to return to recovery mode.

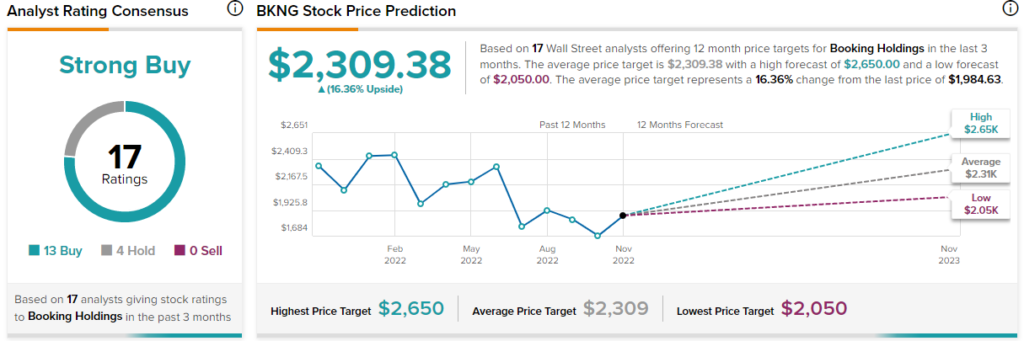

What is the Price Target for BKNG Stock?

Wall Street loves Booking. The average BKNG stock price target of $2,309.38 implies 16.4% upside potential.

Delta Air Lines (NYSE:DAL)

Delta Air Lines is a Strong-Buy-rated airline with nine unanimous Buy ratings. The stock’s 2020-21 rally faltered in 2022, with shares now down around 45% from their pre-pandemic heights.

Indeed, there’s a lot of room to run if Delta can make it through another year of challenges. Third-quarter earnings results were something to get excited about. Though Delta missed by the slightest of margins ($1.51 EPS vs. $1.53 consensus), air travel recovery demand was encouraging.

Indeed, things could turn again as we near a recession. Regardless, management has done a respectable job of managing lofty operating costs. It could take a while for an investment in DAL stock to pay off, but with such a depressed 0.5x sales multiple, I think the risk/reward is as good as analysts think.

What is the Price Target for DAL Stock?

Wall Street continues to favor Delta. The average DAL stock price target of $46.22 implies a whopping 31.7% in gains over the year ahead.

Conclusion: Travel and Leisure Stocks are Worthy Bets

Despite the rocky road ahead, there are reasons to believe that the travel and leisure plays are still worthy bets over the long run. At this juncture, a 2023 recession looks to be factored into valuations for the most part.