Given the troubling state of the U.S. economy, what’s driving the bullish sentiment on Wall Street? Stimulus.

Among the bulls is chief investment strategist at CFRA, Sam Stovall, who estimates that the S&P 500 will hit 3,435 within a year. From current levels, this would reflect a double-digit gain, and come in above the 3,393 high-point posted on February 19. Back in March, he even went so far as to call for a new high in the third quarter, but since then he has updated his forecasts.

“We’ve had a lot of people compare it with the Crash of ’29, the Depression of the 1930s, etc. But back then, you had the government actually tightening their reins, balancing their budget — you did not have a reactive Federal Reserve,” Stovall stated. He added, “Who’s to say we don’t go for a retest first? That’s a normal situation. However, I don’t think we’re going to get an even lower low because of the stimulus already injected into the system.”

To this end, risk-tolerant investors are looking to take advantage of lower share prices, which present more attractive entry points. What’s the advantage of stocks with bargain price tags, specifically those trading for less than $5 per share? Should these names, which are deemed “penny stocks,” experience even minor share price appreciation, it can translate to massive percentage gains.

Therefore, huge returns are on the table, but penny stocks aren’t everyone’s cup of tea. Some argue that there could be a good reason they are trading at such low levels, and that the risk outweighs the potential rewards.

Understanding the risk involved, we wanted to see if we could track down any compelling penny stocks in the healthcare space. Using TipRanks’ database, we pinpointed three that have received enough support from Wall Street analysts to earn a “Strong Buy” consensus rating. The cherry on top? All three of the tickers could double in the next year. Let’s dive in.

Marinus Pharmaceuticals, Inc. (MRNS)

Focused on the development of neuropsychiatric therapeutics, Marinus is one of the top players in the orphan epileptic disorder space. Following a first quarter update on the company’s progress, Wall Street believes its long-term growth narrative is strong and that its $2.06 share price reflects the ideal entry point.

As part of the update, management announced that the design and dosing for the RSE pivotal Phase 3 trial for its lead development candidate, ganaxolone (GNX), had been confirmed, with it set to begin in the third quarter. The co-primary endpoints for the trial are status cessation within 30 minutes and suppression for at least 24 hours, and it will be powered 90% to hopefully show 30% efficacy for GNX when compared to the placebo.

Commenting for Oppenheimer, analyst Jay Olson said, “We view pivotal Phase 3 design as similar to positive Phase 2 trial while benefiting from longer dosing with 12 hours exposure vs. 8 hours prior. MRNS expects top-line data in the first half of 2022.”

Additionally, the company finished enrolling participants for its CDD pivotal Phase 3 MARIGOLD trial, with the top-line data also slated for release in the third quarter. Olson argues that the discontinuation rate of less than 10% and high enrollment rate imply that tolerability levels are “favorable.” The analyst added, “Pre-commercialization and NDA filing preparations remain on track despite COVID-19. We believe MRNS could have a substantial competitive advantage as a first mover.”

If that wasn’t enough, Olson thinks the TSC Phase 2 open-label trial, which should start screening patients in Q2 and could see top-line data published in Q1 2021, could serve as a significant catalyst for shares. While COVID-19’s impact on enrollment caused management to downsize the PRE Phase 3 VIOLET trial into a Phase 2 proof-of-concept trial in order to reprioritize resources, MRNS still has plenty going for it.

“We view MRNS as well-positioned despite potential COVID-19 disruptions, with $77.8 million cash balance providing runway into 3Q21. We view MRNS’s pipeline as attractive with multiple opportunities and several key near-term catalysts. We believe the current share price provides an attractive entry point,” Olson explained.

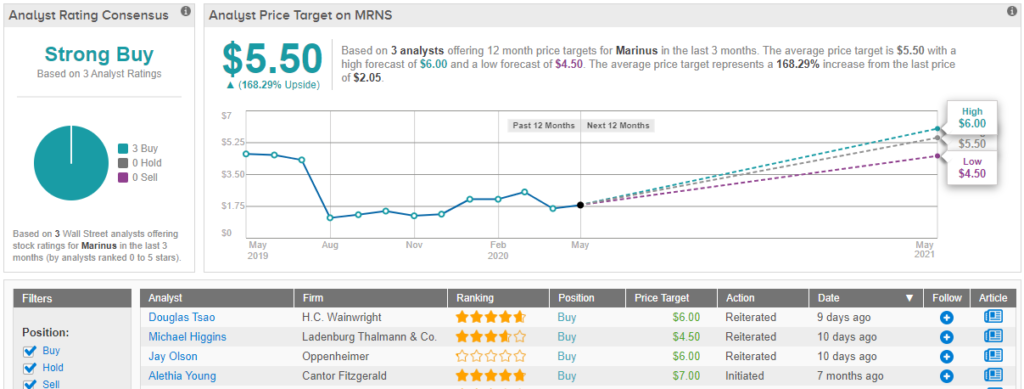

To this end, Olson kept his Outperform call and $6 price target as is. Should this target be met, a twelve-month gain of 191% could be in store. (To watch Olson’s track record, click here)

What does the rest of the Street think about Marinus’ long-term growth prospects? It turns out that other analysts also have high hopes. Only Buy ratings have been received in the last three months, so the consensus rating is a Strong Buy. In addition, the $5.50 average price target suggests 168% upside potential. (See Marinus stock analysis on TipRanks)

Arbutus Biopharma Corporation (ABUS)

With a diverse chronic hepatitis B virus (HBV) product pipeline including direct antiviral, host targeting and immune-based approaches, Arbutus Biopharma wants to develop a cure for the condition. Currently going for $1.65 apiece, several members of the Street think now is the time to get on board as multiple catalysts are fast-approaching.

On May 11, the company revealed that it plans to share further results from the week 12 portion of the 60 mg single-dose cohort evaluating its lead candidate, a GalNAc delivered RNAi compound, AB-729, in the second quarter of 2020.

Five-star analyst Mayank Mamtani, of B.Riley FBR, points out that preliminary data from the Phase 1a/1b AB-729 HBV study showed an HBsAg reduction comparable to advanced RNAi peers, even though it enrolled difficult to treat e-antigen negative patients. As HBsAg reduction rose during the study, the analyst argues that this increases the chances of successful follow-up data.

On top of this, ABUS has several ongoing preclinical studies that are progressing right on track, enabling it to advance its next-generation oral capsid inhibitor, AB-836, into the clinic in 2021. This goes hand in hand with the company’s research efforts to develop an oral HBV RNA-destabilizer and an oral anti-PD-L1 inhibitor. Expounding on this, Mamtani commented, “Building on learnings from the previously discontinued AB-506, AB-836 offers increased potency and an enhanced resistance profile with ongoing IND-enabling studies inclusive of a new assay to help better characterize the safety profile.”

It should also be noted that ABUS is going to start working on a therapy for coronaviruses, specifically targeting RNA-dependent polymerase, nsp12, and viral protease, which play key roles in the replication and transcription cycle of COVID-19. Mamtani thinks this approach is promising as Gilead’s experimental COVID-19 treatment, remdesivir, is a nucleotide analog that binds nsp12, which inhibits viral proliferation and produces clinical benefits.

Mamtani added, “Nsp12 has also been implicated in HCV, HIV, and, notably, HBV, areas in which ABUS has extensive antiviral development expertise. In concert with the biotech and pharma COVID-19 consortium, ABUS anticipates pooling resources along with leveraging primary screening and lead optimization capabilities to advance novel candidates against known and unknown targets, which works ideally as a pan coronavirus agent in order to also prepare for future outbreaks.”

Based on all of the above, it’s no wonder Mamtani reiterated his bullish call. Given the $6 price target, shares could soar 253% in the next twelve months. (To watch Mamtani’s track record, click here)

Turning now to the rest of the Street, other analysts are on the same page. With 100% Street support, or 3 Buy ratings to be exact, the consensus is unanimous: ABUS is a Strong Buy. The $5 average price target brings the upside potential to 198.5%. (See Arbutus Biopharma stock analysis on TipRanks)

Geron Corporation (GERN)

Last but not least we have Geron, which is primarily focused on the development of imetelstat, a small molecule telomerase inhibitor active in the treatment of highly transfusion-dependent MDS and r/r myelofibrosis (MF). While it’s very likely that the company will experience some delays as a result of COVID-19, the Street cites its promising technology and bargain $1.36 share price as making it a compelling healthcare play.

Some investors have expressed concern regarding GERN’s announcement that it won’t be able to complete enrollment for the Phase 3 IMerge trial by 2020 due to the impact of COVID-19. BTIG analyst Thomas Shrader acknowledges that the delay will push back imetelstat’s approval and launch, which he now thinks will come in 2024 instead of 2023. However, he argued, “Geron’s patients are as desperate as they come in r/r MDS and AML and we expect data to date leave physicians and patients highly motivated to find something to try.”

Further explaining the MDS opportunity, Shrader believes the program demonstrates robust levels of durability. Not only does the five-star analyst call the 24-week RBC-TI rate “highly compelling”, but he also highlights the strong safety profile.

Shrader said, “Greater than 90% of patients with neutropenias and thrombocytopenias had these AEs resolve prior to the next dose. This reversibility is in contrast to both HMAs and Revlimid where these toxicities result in drug interruptions. A KOL recently commented that the high 68% HI-E response suggests most patients receive some benefit – making any subsequent trials very easy to enroll.”

It should be noted that previously, its IMbark trial had a 32% discontinuation rate thanks to lack of efficacy, but Shrader thinks “these discontinuations may have been premature due to the drug’s slow onset of action and its ‘black box nature’ during the trial.” He added, “Based on increased understanding of how imetelstat works and its promise as a therapeutic, this discontinuation rate is likely to be low in subsequent trials. Imetelstat seems likely to be used after luspatercept in RS+ MDS but could be the only drug after ESAs in other forms of the disease (including RS-).”

With GERN working out the MF trial design and hoping to discuss the regulatory path forward with the FDA in Q2, the deal is sealed for Shrader. Along with a Buy rating, he did trim the price target from $4 to $3, but this still leaves room for 114% upside potential. (To watch Shrader’s track record, click here)

All in all, other analysts echo Shrader’s sentiment. 3 Buys and no Holds or Sells add up to a Strong Buy consensus rating. Based on the $3.50 average price target, the upside potential comes in at 149%. (See Geron stock analysis on TipRanks)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.