Metals prices and mining stocks have plummeted in recent weeks, with gold declining steadily from a firm footing above $1,800 an ounce to below $1,700 temporarily. Copper has taken a hit as well. Of course, not all miners are created equally, so in this piece, we used TipRanks’ Comparison Tool to evaluate two mining stocks with solid upside potential.

Analysis reveals reasons to be bullish on both Freeport-McMoRan (FCX) and Barrick Gold (GOLD)(TSE: ABX) right now, although Freeport is looking better than Barrick in the short term.

While inflation has historically been good for gold, traditionally a safe-haven investment, it hasn’t done anything to help the precious metal this year.

The problem is the strength of the U.S. Dollar, which is being driven by the Federal Reserve’s push to raise interest rates before the rest of the world can do so. As a result, some investors might think it’s just crazy to buy gold right now, let alone gold miners.

However, the rising probability of a recession could be setting the gold market up for a healthy rebound, meaning that miners appear to be on sale right now. Additionally, the effects of copper amid the growth in electric vehicles add even more luster to miners of both gold and copper.

Freeport-McMoRan

A quick look at Freeport-McMoRan’s stock performance reveals that the pandemic has been very kind to it. The stock is up over 370% since April 2020, and that includes the current decline that started toward the end of March 2022. Another good sign is that company insiders have been snapping up more shares of the gold miner in the last three months, as have hedge funds.

It’s important to note that Freeport-McMoRan isn’t primarily a gold miner. As the second-largest copper miner in the world, a larger share of its revenue actually comes from copper. Copper prices took a sizable bite out of the company’s second-quarter results, but they should bounce back rather quickly amid the growing adoption of electric vehicles, which rely heavily on copper.

The company boosted its production of copper, gold, and molybdenum during the second quarter. It produced 1.075 million pounds of copper, an 18% year-over-year increase, 476,000 ounces of gold, for a 56% increase, and 23 million pounds of molybdenum, for a 15% increase. Freeport-McMoRan reported a 17% increase in copper sales volumes and a 56% increase in gold sales volumes in the second quarter.

For the first quarter, Freeport-McMoRan recorded a 36% year-over-year increase in revenue to $6.6 billion. The company also more than doubled its net income and diluted earnings per share to $1.53 billion and $1.04 per share, respectively. However, the second quarter brought a reversal, with revenue falling year-over-year from $5.7 billion to $5.4 billion and diluted net earnings per share falling from $0.73 per share to $0.57 per share.

One of the more attractive numbers in FCX’s first-quarter earnings release was the net profit margin of 23.13%, an increase of 56% year-over-year. Unfortunately, the company’s profit margin fell to 15.5% for the second quarter from 18.8% in the year-ago quarter as inflation boosted costs.

Freeport-McMoRan reported $1.6 billion in operating cash flows for the second quarter and $3.3 billion for the first half of 2022.

Freeport-McMoRan: A Shareholder-Friendly Company

The company is quite friendly to shareholders, publicizing its ESG-friendly practices in its 2021 Annual Report on Sustainability. This should provide some support as more investors become concerned about the negative impacts mining has on the environment.

Additionally, Freeport-McMoRan began a $3 billion share repurchase program in November and added a variable dividend. Up to 50% of its cash flows after planned capital spending and distributions to non-controlling interests will be paid out via the variable dividend.

FCX’s recent earnings numbers illustrate a strong company with a robust balance sheet, while the shareholder-friendly initiatives and variable dividends should provide some support during these inflationary times.

Turning to Wall Street, Freeport-McMoRan has a Moderate Buy consensus rating based on six Buys, six Holds, and one Sell rating assigned over the last three months. At $36.50, the average Freeport-McMoRan price target implies upside potential of 29%.

Barrick Gold

Investors looking for a stronger gold play might be more interested in Barrick Gold, although about 20% of its profits still come from copper. However, the company’s stock has performed far worse than that of Freeport-McMoRan, which is why a neutral view might be more appropriate in the short term with a shift to bullish over the long term.

Barrick Gold shares are essentially trading at March 2020 levels and have lost half of their value since August 2020. A look at the company’s financials reveals why its stock isn’t performing as well as Freeport’s.

It won’t report its second-quarter results until August, but its first-quarter results revealed some problems. Barrick Gold’s revenue fell more than 3% year-over-year to $2.85 billion, while its net income fell more than 18% to $438 million. Diluted earnings per share declined to $0.25, while its net profit margin declined to 15.35%. Free cash flow fell from $783 million last year to $393 million this year.

Barrick Gold is working on boosting its gold production to 4.8 million ounces per year by the end of the decade from 4.4 million last year. However, the company reduced its production in the last few years, as it produced 5.5 million ounces in 2019, allowing it to generate $1.1 billion in free cash flow.

A Recession Could Lift Gold Prices, but Barrick’s Production is Low

Some investors may wonder whether Barrick Gold’s best days are behind it. However, when the next recession hits, potentially in the next year or two, gold prices would probably pop, as they often do during a recession, bringing gold miners along for the ride.

Unfortunately, one thing holding the company back right now is its low production. Barrick Gold released preliminary second-quarter production numbers of about 1.04 million ounces of gold and 120 million pounds of copper. It expects its gold production to increase throughout the year.

Like Freeport, Barrick is also making ESG strides with a 2021 Sustainability Report, which should help on the ESG front. It’s also making an effort on its dividend by adding a performance component similar to Freeport’s variable component. Barrick’s dividend yield is now 2.6%, making it somewhat attractive to dividend investors.

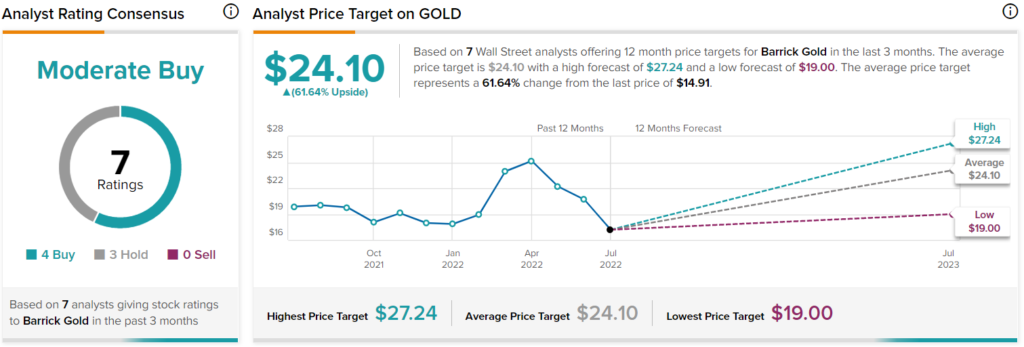

Turning to Wall Street, Barrick Gold has a Moderate Buy consensus rating based on four Buys, three Holds, and zero Sell ratings assigned over the last three months. At $24.10, the average Barrick Gold price target implies upside potential of 61.6%.

Conclusion: Both Companies to Benefit from Gold, Copper Demand

A deep dive into Freeport and Barrick reveals two very different companies, but both should benefit when gold comes roaring back. Additionally, their exposure to copper should provide long-term support due to the growth of electric vehicles.