We’re in unsettled market times. 2022 saw sharp drops that brought a sudden end to last year’s bullish trends. While the past few trading days have been mostly bullish, it’s very difficult to predict what’s coming next.

Investors need some signal to make sense of the volatile trading. There are simply too many currents and counter-currents for the average retail investor to chart a clear path. This is where the TipRanks Smart Score comes in.

Using a set of proprietary algorithms, the Smart Score collects a range of data for every stock – and sorts it according to 8 factors that are known to influence stock price. The result is a single distilled score, on a 1 to 10 scale, that can tell an investor at a glance the general health of a stock. And a look behind the score is easy to do, and add context to a stock’s performance.

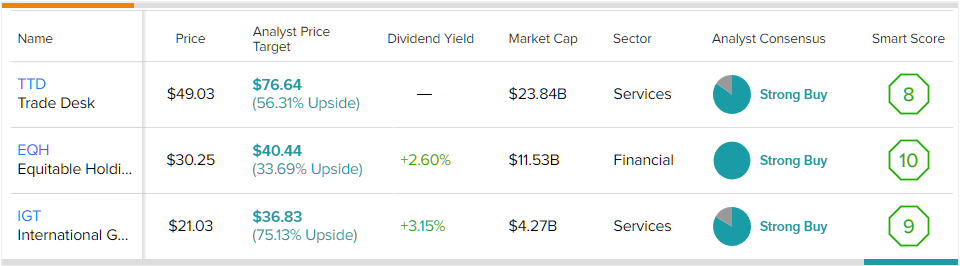

We’ve opened the TipRanks database and pulled up three stocks that have earned top rating from the Smart Score. Let’s take a deep dive in, and also find out just what Wall Street’s analysts think of these.

Trade Desk (TTD)

First up is Trade Desk, a California-based software company in the digital marketing universe. The company’s platform is designed to optimize online and digital advertising and marketing solutions, programs, and data analysis, to drive audience engagement and make data work for the user. Trade Desk is aiming to take a leading position in the $1 trillion total addressable market in global advertising.

For now, Trade Desk has revenues of $315 million, reported for 1Q22. This is up 43% from the year-ago quarter. The non-GAAP diluted EPS was 21 cents, 50% higher than the 1Q21 result. It is important to note that Trade Desk has a pattern of reporting its lowest quarterly revenues in Q1, and seeing them rise through the year to Q4.

Early this month, Trade Desk announced an expansion of its OpenPath product, which gives subscribing advertisers direct access to a premium digital ad inventory. Publishers now include such well-known names as BuzzFeed, the LA Times, and Forbes magazine. This follows a move announced in March to launch a certified service partner program for small- and medium-sized businesses. These are the traditional growth engine of the US economy, and represent a growing client demand.

But the potentially strongest source of client demand is coming from the online streaming services. Both Netflix and Disney+ have announced moves to add advertising to their services, to boost revenues and drive subscriptions. Trade Desk, which operates in exactly this online digital ad universe, is ideally positioned to gain from such a move.

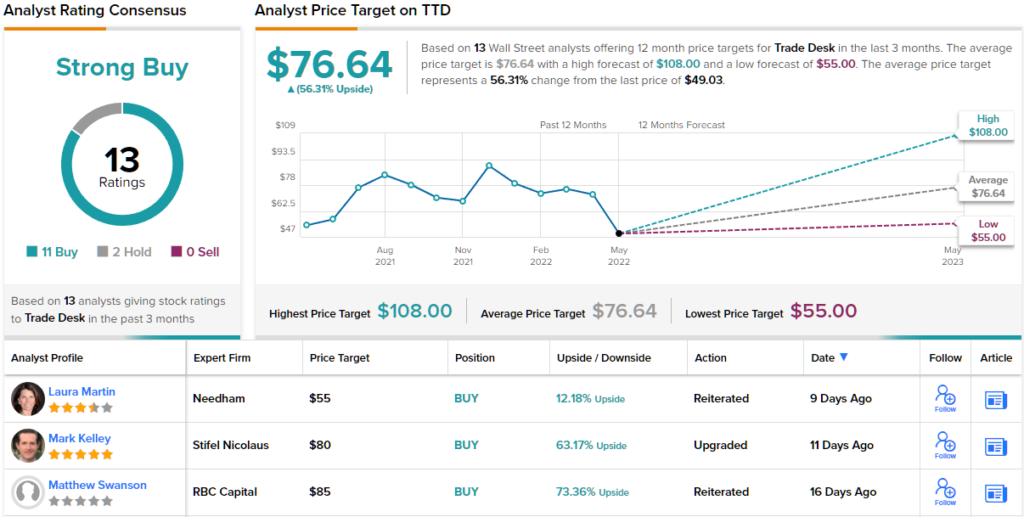

Like the other stocks on this list, Trade Desk boasts an impressive Smart Score. The metric finds support from increased buying by both hedge managers and company insiders.

Covering Trade Desk from Stifel, 5-star analyst Mark Kelley says, “Netflix with ads is a big deal (as is Disney+ with ads), and it changes our view on the state of CTV advertising in the near-to-medium term. Based on our assumptions of what we view as reasonable assumptions for ad spend on Netflix, we estimate The Trade Desk should see an incremental $300mn in 2023 revenue (14% upside to current estimates) with a bull case of an incremental $950mn (45% upside to our estimates).”

This outlook supports Kelley’s Buy rating, and his $80 price target implies a 63% upside by next year. (To watch Kelley’s track record, click here)

Digital tech always attracts Wall Street investors, and 13 analysts have filed reviews of TTD. Their opinions favor Buy over Hold 11 to 2, for a Strong Buy consensus rating, and the average price target of $76.64 suggests ~56% upside from the trading price of $49.03. (See TTD stock forecast on TipRanks)

Equitable Holdings (EQH)

Now we’ll turn to the financial services sector, where Equitable Holdings provides a range of services, including individual and group retirement planning, capital management and protection, investment management and research, and a variety of insurance products. The company has $856 billion in total assets under management, and in 1Q22 EQH reported $3.94 billion in total revenues.

That total included a net income of $537 million, a dramatic turnaround from the net loss of $1.48 billion in 1Q21. Non-GAAP EPS of $1.36 was essentially flat year-over-year. Equitable Holdings is forecasting a 30% increase in cash generation for 2022, predicting $1.6 billion in cash from operations for the year.

Strong cash flows will support the company’s dividend, which was declared this month for a 20 cent per common share payment on June 6. That payment marks a 20% increase, and with an annualized payment of 80 cents, gives a yield of 2.7%. The company has also been maintaining a consistent program of stock buybacks, totaling $279 million in 1Q22.

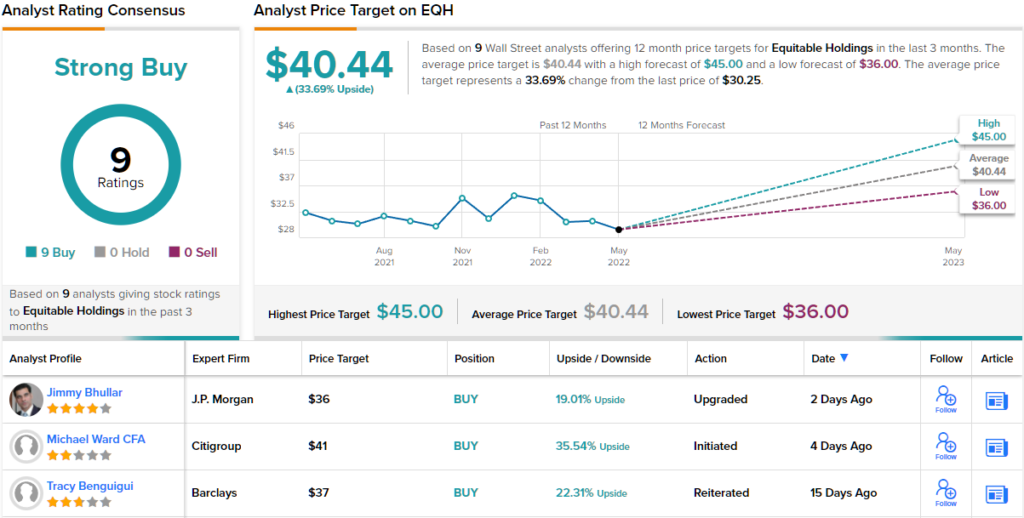

On the Smart Score, EQH’s perfect 10 is supported by bullish blogger sentiment, strong fundamentals, and hedge funds and individual investors are all buying in.

This company’s sound position leads JPMorgan’s Jimmy Bhullar to take a bullish stance. While acknowledging that current market conditions act as a headwind on the stock, the analyst believes it is well-placed for strong growth over the long term.

“In our view, the stock will be pressured if the equity market drops further or if valuation multiples for asset managers (such as AB) stay depressed, but we feel that EQH presents very attractive upside in the long run… We believe that EQH’s business mix will produce better ROE, EPS growth, and cash flow than other life insurers over time. In addition, the company’s capital levels are healthier and its investment portfolio is more defensive than peers’,” Bhullar opined.

It’s not surprising, then, why Bhullar upgraded EQH from Neutral to Overweight (i.e. Buy), while giving the stock a $36 price target. (To watch Bhullar’s track record, click here)

It’s clear from the analyst reviews that the Street is bullish on this stock. EQH has 9 reviews on record and all are positive, for a unanimous Strong Buy consensus rating. The shares are priced at $30.25 and have an average price target of $40.44, implying an upside potential of ~34% for the coming year. (See EQH stock analysis on TipRanks)

International Game Technology (IGT)

Last up is International Game Technology, a major designer and producer in the world of electronic casino slot games, electronic lotteries, and digital and social gaming. IGT provides video slots for casinos, video games for bars and other entertainment venues, and operates with governments and private lotteries around the world, offering online and brick-and-mortar lotto, sports betting, and digital gaming.

Gaming is big business, and IGT has been bringing in at or near $1 billion quarterly for the past five quarters. In the most recent, 1Q22, the company reported $1.05 billion in total revenue, with 64% of that coming from global lottery gaming. Diluted EPS, at 39 cents per share, was positive for the third quarter in a row.

The company’s cash flow slipped in Q1 compared to last year. Cash from operations went from $251 million to $189 million, and cash on hand fell from $748 million to $600 million. Nevertheless, the company maintained its 20-cent per common share dividend payment, with the next payout declared for June 7. The 80-cent annualized payment gives a yield of 3.9%, about double the average dividend yield found among the broader market’s dividend payers.

IGT has been moving to expand its operations and keep up with the industry, and made several relevant announcements in May. On May 11, the company announced an agreement with the NUSTAR resort and casino in Cebu Philippines. On opening, NUSTAR will use IGT’s ADVANTAGE casino management system in its operation. IGT also announced in May that it will be expanding the use of its Money Mania Wide Area Progressive slot games from tribal jurisdictions into commercial casinos. And finally, on May 25, IGT announced a multi-year contract with Harrington Raceway and Casino in the UK, to optimize the gaming floor and player rewards.

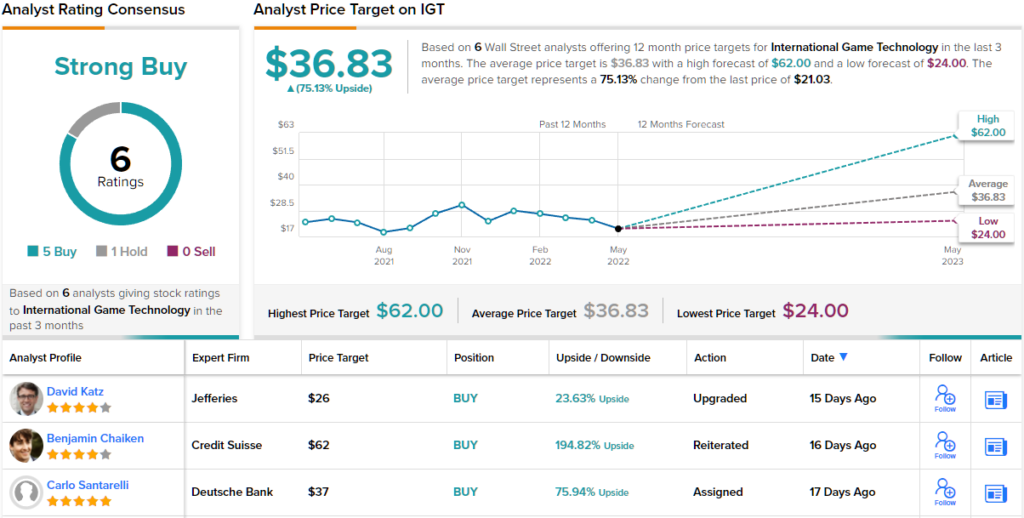

IGT’s high Smart Score is buttressed by the solid analyst forecast, the 100% bullish sentiment from the bloggers, and a large increase in hedge fund trading in the last quarter.

Jefferies analyst David Katz is blunt about this upbeat outlook here. In his report on the stock he writes: “Our… Buy on IGT is based the current trough levels for the shares coupled with the stability inherent in the business. We also note strength and progress within the gaming machine business, which we believe has an outsized impact on the shares, coupled with the economically resilient lottery business globally. IGT presents solid growth and capital setup relative to peers, which we believe warrants upside in a wide range of market conditions.”

Katz’s Buy rating is backed up by his $26 price target, which indicates potential for ~24% upside to the stock over the next 12 months. (To watch Katz’s track record, click here)

Overall, Wall Street would tend to agree with this bullish outlook – as shown by the 5 to 1 breakdown in recent reviews, favoring Buys over Holds and supporting a Strong Buy consensus view. The stock is trading for $21.03 and its $36.83 average price target implies a potential upside of ~75% in the next 12 months. (See IGT stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.