Yext (YEXT) is gearing up to report its FQ2 results on Thursday, September 3.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

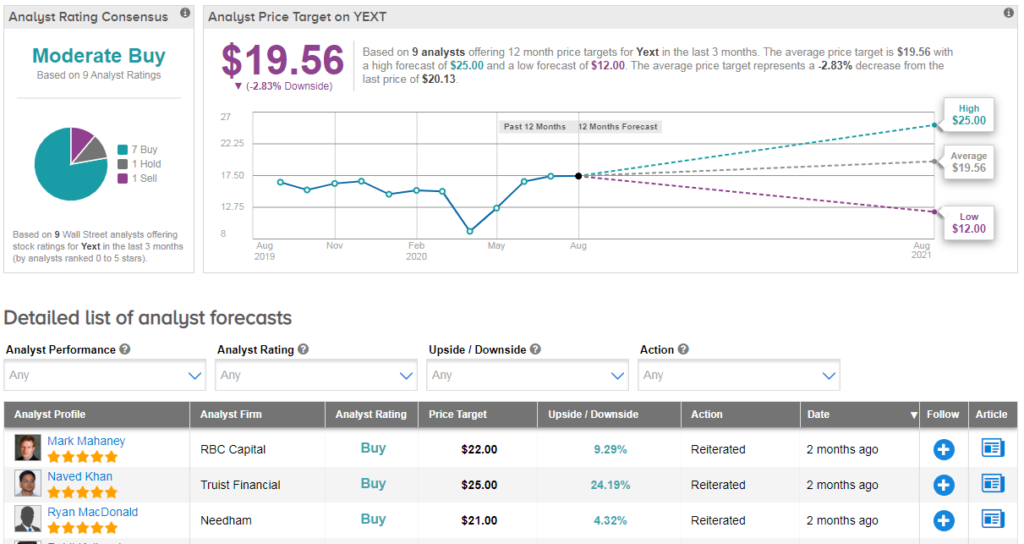

And ahead of this key date, five-star RBC Capital analyst Mark Mahaney has reiterated his buy rating on the digital data manager with a $22 price target (9% upside potential).

“We believe FQ2 estimates are reasonable, with an equal likelihood of upside vs. downside variance. We also view Street assumptions for FQ3 as reasonable/ bracketable (16% Y/Y revenue growth, and $0.13 Non-GAAP EPS loss)” Mahaney wrote on August 28.

Specifically, the analyst is forecasting FQ2 revenue of $86.2MM, above the Street at $85.1MM and at the high end of guidance ($85-$86M).

Meanwhile his Adjusted EBITDA loss estimate of ($11MM) is also slightly above the Street at ($12MM) with a Non- GAAP EPS loss estimate of ($0.11) vs the company’s FQ2 guidance of ($0.13) – ($0.11).

According to the analyst “top-line growth along with clear messaging around the continued execution around Yext Answers will be of heightened importance.” He is also looking for ~3 pts of Y/Y deleverage in EBITDA margins, reflecting investments in International expansion and headcount.

Taking a step back from earnings, although growth has slowed recently, Mahaney believes YEXT is capable of sustaining +20% growth over the next several years. In particular, Yext Answers could be a strong new product for the company as it nearly doubles the company’s TAM and as Yext continues to strengthen its mid-market and enterprise salesforce capabilities.

Net-net Yext faces a very large TAM with a high visibility, recurring revenue model, says Mahaney. “It is still an open question whether/when Yext’s investments in International expansion and salesforce ramp will translate to growth, but we remain optimistic and expect that these investments will start to pay dividends later in FY21” he concludes. (See YEXT stock analysis on TipRanks)

Shares in Yext are trading up 40% year-to-date, and the Street has a cautiously optimistic Moderate Buy consensus on the stock’s outlook. That’s with a $20 average analyst price target, indicating a small pullback from current levels.

Related News:

Amazon Scores FAA Green-Light For Prime Air Drone Delivery

Zoom Video Pops 23% On Blowout Quarter With Sales Soaring 355%

Facebook Will Scrap News Sharing In Australia If New Law Passed