Boston-based Atea Pharmaceuticals (AVIR) is engaged in developing antiviral therapeutics. It has collaborated with Roche Holding (RHHVF) in some of those efforts. Markedly, Atea’s product candidates include a potential treatment for COVID-19.

Let’s take a look at Atea’s latest financial performance, drug development programs, and risk factors.

Atea’s Q2 Financial Results

Atea does not have a drug on the market yet. However, it managed to generate $60.4 million in collaboration revenue in the second quarter through its license agreement with Roche entered into last year.

The company posted a profit of $1.5 million, compared to a loss of $10 million a year ago. (See Atea stock charts on TipRanks).

Atea’s Drug Development Program

The company has several drug candidates targeting diseases such as COVID-19 and dengue fever. Atea is also developing a treatment for Hepatitis C. Its COVID-19 drug candidate AT-527 has produced encouraging results in early trials.

Atea has partnered with Roche to develop AT-527. In July 2021, Roche paid Atea $50 million after AT-527 achieved a development milestone. If AT-527 makes it to market, Atea will sell it in the U.S., while Roche will have exclusive rights to sell it in markets outside the U.S. Atea’s dengue drug candidate AT-752 has also shown encouraging outcomes in early trials.

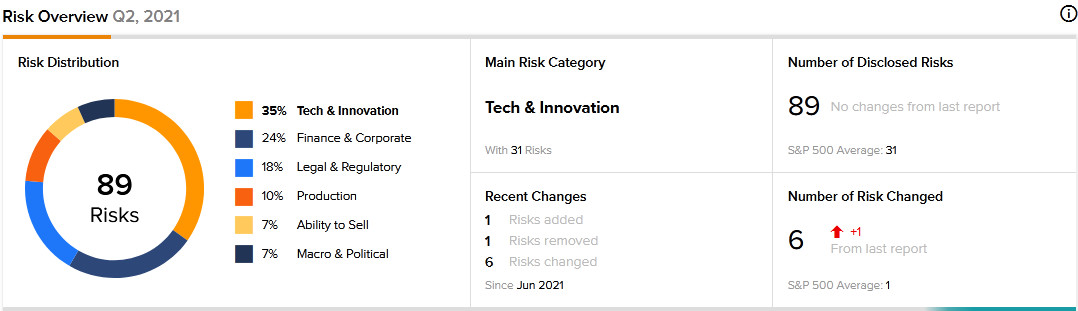

Atea’s Risk Factors

The new TipRanks Risk Factors tool shows 89 risk factors for Atea. Since December 2020, the company has updated its risk profile to introduce one new risk under the Production category.

The company tells investors that it does not have complete control over its manufacturing process. For example, it relies on third parties to manufacture and supply material for its clinical trials. It also expects to rely on contract manufacturers for commercial production of its approved drugs. The risk is that the third parties may not supply materials or products in a timely manner, or the quality that Atea expects. Furthermore, the contract manufacturers may raise their prices.

Tech and Innovation is Atea’s top risk category, accounting for 35% of the total risks. That is above the sector average at 25%. Atea’s shares have declined about 27% since the beginning of 2021.

Analysts’ Take

Morgan Stanley analyst Matthew Harrison recently reiterated a Buy rating on Atea stock and raised the price target to $37 from $35.

Consensus among analysts is a Moderate Buy based on 2 Buys. The average Atea price target of $37 implies 21.11% upside potential to current levels.

Related News:

Medtronic Q1 Results Beat Estimates; Shares Pop 3%

A Look at GrowGeneration’s Earnings and Risk Factors

What Does GCM Grosvenor’s Newly Added Risk Factor Tell Investors?