Shares of Walmart Inc. (NYSE: WMT) dropped nearly 10% during after-hours trading yesterday after America’s largest retailer cut its profit outlook for the second quarter and full fiscal 2023. Walmart warned about shifting consumer preferences toward necessities, propelled by record high inflation levels with no relief in sight. Following the news, several major retailers like Costco and Target also saw their shares dip.

Consumers are stocking up on more groceries and daily necessities from Walmart and Sam’s Club stores as they fear the prices of these goods will go up further. Meanwhile, consumers are also cutting down on their spending on discretionary items as they are spending more each time they visit the pump and shop for groceries. Walmart noted that food inflation is in double digits and higher than it was at the end of Q1.

This shift has led to a stock load of other items such as home goods and apparel on the racks. Walmart said it is going to declare huge discounts on these products, a necessary move to get them off the shelves. Although the step will boost the sale of the not-so-necessary products, it will, however, suppress the margins on these items, which are generally higher than food and groceries.

Commenting on the issues, President and CEO of Walmart, Doug McMillon, said, “The increasing levels of food and fuel inflation are affecting how customers spend, and while we’ve made good progress clearing hardline categories, apparel in Walmart U.S. is requiring more markdown dollars. We’re now anticipating more pressure on general merchandise in the back half; however, we’re encouraged by the start we’re seeing on school supplies in Walmart U.S.”

Walmart Cuts Profit Outlook

After issuing a warning regarding weakening consumer demand, Walmart said it expects Q2 and FY23 adjusted earnings per share (excluding divestitures) to fall by 8% to 9% and 10% to 12%, respectively. Previously, the retailer had expected them to remain flat or up slightly in Q2 and to fall by 1% for FY23.

Nonetheless, Walmart expects consolidated net sales growth of about 7.5% for Q2 and about 5.5% for FY23 (excluding divestitures). Moreover, Q2 comparative sales for Walmart U.S. (excluding fuel) are expected to be around 6%. These figures are higher than its previous guidance as the retailer witnesses a heavy outflow of groceries from its stores. However, since the necessities carry lower margins, higher sales from these do not bolster the bottom lines.

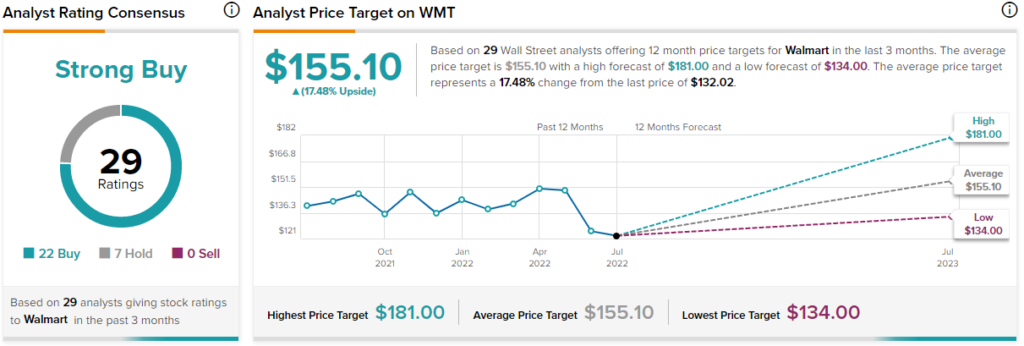

Analysts Are Bullish on WMT

Following the news, Guggenheim analyst Robert Drbul slashed the price target on WMT stock to $155 (17.4% upside potential) from $175 while maintaining a Buy rating. Keeping Walmart’s bleak outlook in mind, the analyst even cut down his model estimates for all quarters of 2022 as well as for fiscals 2022 and 2023.

Drbul is encouraged that Walmart is gaining market share from the increased shopping of grocery and food items at its stores. However, he does acknowledge the impact on gross margins and profits from the markdowns and mix. At the same time, he also appreciates the retailer’s conservative outlook for the rest of the year.

“We believe the company is making progress on its inventory levels but has more work to do, given a glut of inventory throughout U.S. retail, especially general merchandise and notably apparel. We believe inflation and stimulus spending from last year are impacting mix at a greater level than we previously expected,” Drbul added.

Similarly, MKM Partners analyst William Kirk also cut the price target on WMT stock to $152 (15.1% upside potential) from $159 and maintained a Buy rating.

Kirk’s optimism stems from the belief that “a bad Apparel cycle does not impact the long-term investment case for Walmart.” The analyst has full faith in Walmart’s rapidly growing advertising business. Moreover, Kirk is also encouraged by the growing market share of groceries against peers and increasing e-commerce adoption, which bode well with Walmart’s supply chain leadership.

“We estimate Walmart’s run-rate is >700mn online transactions a year ($50bn in sales). That captive audience can be more heavily monetized and provide earnings support independent of growth in physical stores. What is currently a $2bn ad business could become a $30bn ad business over time,” Kirk concluded.

Despite all the near-term noise, analysts are highly optimistic about WMT stock with a Strong Buy consensus rating based on 22 Buys and seven Holds. The average Walmart price target of $155.10 implies 17.5% upside potential to current levels. Meanwhile, WMT stock has lost 8% so far this year.

Ending Thoughts

Being America’s largest retailer, Walmart’s warnings cast a shadow on some of the other retail stocks dragging their shares down during after-hours trading. Shares of Target (TGT), which had earlier slashed its guidance due to excess inventory issues fell 5.1%. Meanwhile, Costco (COST) dropped 3.1%, and e-eommerce giant Amazon.com (AMZN) sank 4%. Similarly, other apparel retailers slipped more than 3% on the news.

Walmart has cautioned the masses on the bleak outlook for the rest of 2022. Inflation is making a hole in consumers’ pockets, which is going to take time to recover. Nonetheless, the Street appreciates Walmart’s caution ahead of its final release of Q2FY23 results, scheduled for August 16.