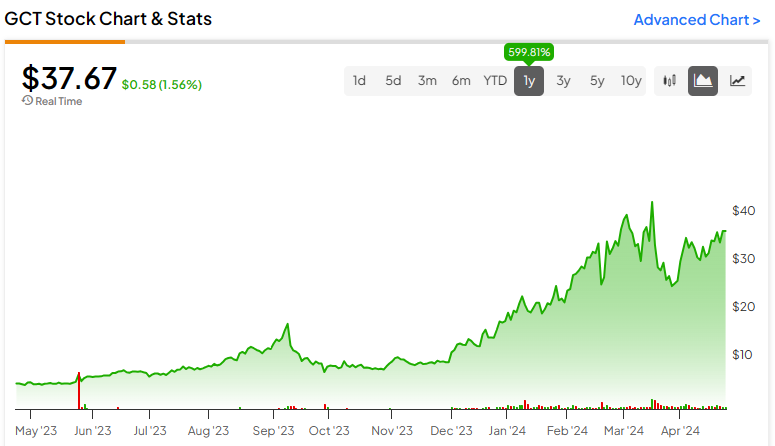

GigaCloud Technology (NASDAQ:GCT) is one of the best-performing growth stocks I’ve encountered recently. Currently, GigaCloud Technology stock is up 600% over 12 months, putting it ahead of the Magnificent Seven and a host of artificial intelligence (AI) stocks. Nonetheless, it continues to trade with some very attractive metrics. In fact, it’s trading at just 12.7x forward earnings. With a strong forecast throughout the medium term, I remain bullish on GigaCloud Technology stock.

Is This Growth Stock for Real?

While the name might suggest this is an IT or server stock, it’s not. The company is in the furniture and large parcel business and used to be called Oriental Standard Human Resources. According to a recent interview with CEO Lei Wu, the name was chosen as giga means ‘giant’ in Greek, and cloud as a reference to the large packages it deals with. However, some people have suggested the name was chosen to lure in investors looking for the next big tech gainer.

Having followed the analysis and discourse concerning this stock for around a year, I’d suggest that the name actually heightened investors’ concerns about the stock. Several analysts have questioned whether GigaCloud is the real deal, noting the name, the late 10-K filing, and the short report that surfaced in March suggesting the company’s operational success was exaggerated.

Some investors are also wary of the firm’s Chinese links and its efforts to appear American (its corporate headquarters are in El Monte, California). One review also questioned Chinese auditing and whether the company’s finances were in check and asked why the founder would be selling off shares if the company was so undervalued.

However, from a personal perspective, the recent interview with the CEO, Larry Wu, has allayed any fears. The company’s operations had been a mystery to many investors, and Wu explained that it followed a very different model compared to traditional ‘pick and pack’ operators. The CEO claimed that it wasn’t prioritizing its website either, reiterating that the B2B model didn’t need a flashy platform. It was also noted by the CEO that the 10-K was actually delivered within a 15-day extension period.

What Does GigaCloud Technology Do?

GigaCloud Technology offers a B2B platform that essentially connects furniture manufacturers—predominantly in China—with resellers and retailers in North America and Europe. As noted during the last earnings call, the company’s main market is the U.S. The company also provides logistics solutions, taking the furniture from the factory to the buyer.

This might not sound revolutionary, but clearly, the company has found a receptive audience. It works on the basis that transporting unsold furniture—or large parcel items—to the end market requires huge warehouses, showrooms, and storage costs. However, GigaCloud does operate warehouses in the U.S., including one in New Jersey, but its ‘pick and pack’ model is different from that of B2C companies (as stated above), requiring much fewer employees.

GigaCloud has 33 warehouses globally, totaling 8.2 million square feet, including 24 in the U.S. The majority of its employees, 966, are based in China. It also has 236 employees in the U.S., and the remainder are in Vietnam, Malaysia, Canada, Germany, Japan, and the UK.

Up 512%, This Growth Stock Still Looks Cheap

GigaCloud’s Q4 earnings report highlighted the scale of the company’s growth over the past year. Total revenues were $244.7 million in the fourth quarter of 2023, an increase of 94.8% from $125.6 million in the fourth quarter of 2022. Meanwhile, its gross profit was $69.8 million in the fourth quarter of 2023, an increase of 161.4% from $26.7 million in Q4 of 2022. Additionally, net income was up 161.4% at $69.8 million.

The company has also seen its margins strengthen during the period. Its gross margin increased to 28.5% in the fourth quarter of 2023 from 21.2% in the fourth quarter of 2022. Meanwhile, its net income margin jumped to 14.5% in the fourth quarter of 2023 from 9.9% in the fourth quarter of 2022.

With earnings and margins improving at such an impressive rate, GigaCloud continues to have some strong and attractive valuation metrics. In fact, it looks pretty cheap. The stock is currently trading at 12.7x forward earnings. Given the projected earnings, this price-to-earnings ratio is expected to fall to 10.1x in 2025 and 8.1x in 2026. While I realize that Chinese and Chinese-linked companies tend to trade at discounts to the wider market, I still think this stock presents good value.

Is GigaCloud Technology Stock a Buy, According to Analysts?

GigaCloud Technology is currently rated Moderate Buy based on just one Wall Street analyst offering a 12-month price target in the last three months. GigaCloud Technology stock’s price target is $46.00. The price target represents a 24% change from the last price of $37.09.

The Bottom Line on GCT Stock

GigaCloud Technology trades at remarkably low multiples, given the growth trajectory that it’s on. I understand that there have been several concerns raised about the company, it’s operations, and its finances. However, many of those fears appear to have been checked off after a recent interview with the CEO. Companies linked with China often trade at discounted valuations. However, regardless of the China discount, GigaCloud Technology still looks considerably undervalued.