Ziopharm Oncology (ZIOP) is an American clinical-stage biopharmaceutical company focused on developing cancer therapies. The company is working on several product candidates at various stages of development. (See Insiders’ Hot Stocks on TipRanks)

Let’s take a look at the company’s latest financial metrics, corporate updates, and changes in risk factors.

Q2 Financial Metrics

Since Ziopharm has yet to launch a product to the market, it did not report any revenue for Q2 2021. Instead, the company reported its cash position, saying it ended Q2 with $76.7 million in cash. (See Ziopharm Oncology stock charts on TipRanks).

Corporate Updates

Ziopharm has secured $50 million in venture debt financing from the Silicon Valley Bank. The agreement is that Ziopharm can draw $25 million from the facility immediately, but the remaining $25 million will be released to Ziopharm upon achievement of certain conditions, including clinical milestones.

Ziopharm has cut some jobs to reduce expenses so that its cash can last longer. As a result, the company now expects to have sufficient cash to fund its operations and clinical programs into the first half of 2023.

In August 2021, Ziopharm appointed Kevin Boyle as its new CEO. Boyle was the CEO of Kuur Therapeutics until its acquisition by Athenex in May 2021. The company said Boyle has a strong track record when it comes to delivering shareholder value.

Ziopharm is gearing up to start its TCR-T Library Phase I/II clinical study. It plans to begin dosing patients in the first half of 2022. It previously aimed to start dosing patients in Q4 2021, but its contract manufacturer experienced challenges that caused delays. The company is now investing in building internal manufacturing capabilities.

While Ziopharm has pushed back the launch of the TCR-T Library Phase I/II clinical program, clinical trials of its CD19 RPM CAR-T cell therapy have begun in Taiwan. Eden BioCell, a joint venture of Ziopharm and TriArm Therapeutics, is undertaking the Taiwan clinical trial.

Risk Factors

The new TipRanks Risk Factors tool shows 54 risk factors for Ziopharm. Since Q4 2020, the company has updated its risk profile to introduce four new risk factors and remove two old ones.

In a newly added risk factor, Ziopharm tells investors that it had to go into debt to increase its liquidity. But the problem is that it may not have enough cash flow from its operations to service the debt. It warns that a default of its debt obligations could put its assets securing the debts at risk.

Ziopharm also tells investors that it could fail to meet the conditions necessary for the release of the $25 million remaining in the Silicon Valley Bank debt facility agreement. It cautions that failure to access the additional funds would reduce its liquidity. Moreover, it would be required to start repaying the portion of the facility it has already drawn, earlier than it would have if it qualified for the second portion.

Ziopharm says in another newly added risk factor that it relies on third parties to help with trial programs for its drug candidates. However, since it does not control the parties, they may not be fully committed to the programs or could assist its competitors. Therefore, the involvement of third parties could lead to delays in drug approvals by the FDA or reduce Ziopharm’s competitive advantage in the market.

Ziopharm has dropped the risk factor that cautioned about its reliance on the National Cancer Institute for research and clinical trials of some of its product candidates. It also removed the risk factors warning that inability to increase the authorized share count could hamper its ability to raise additional capital through stock sales.

The majority of Ziopharm’s risk factors fall under the Tech and Innovation category, with 35% of the total risks. That is above the sector average of 26%. Ziopharm’s stock price has declined about 30% since the beginning of 2021.

Analysts’ Take

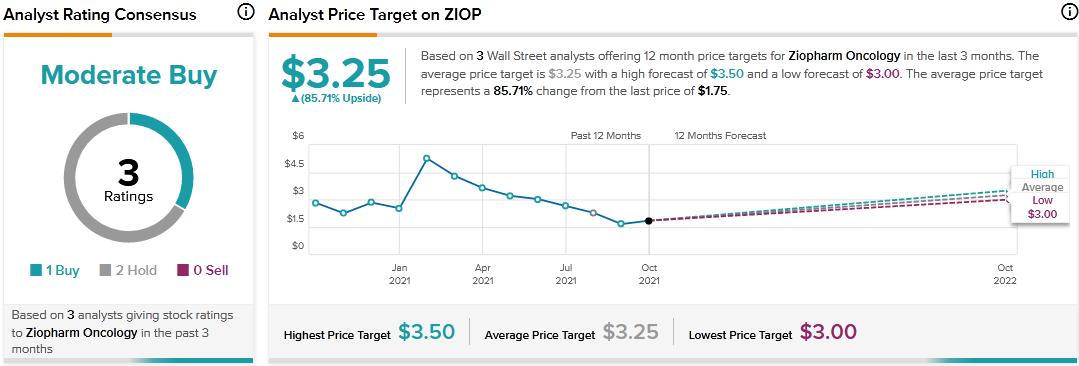

In August, Lake Street analyst Thomas Flaten reiterated a Buy rating on Ziopharm stock but cut the price target to $3.50 from $7. Flaten’s new price target suggests 100% upside potential. The analyst lowered the price target on Ziopharm stock after the company announced delays to its CAR-T study.

Consensus among analysts is a Moderate Buy based on 1 Buy and 2 Holds. The average Ziopharm Oncology price target of $3.25 implies 85.71% upside potential to current levels.

Related News:

Newtek Highlights New Risk Factors Amid Transformation

E2open Delivers Mixed Q2 Results; Shares Drop

Poshmark Buys Suede One to Authenticate Sneakers; Shares Jump 6.7%