Sales of Tesla, Inc.’s (NASDAQ: TSLA) China-manufactured vehicles grew 142% month-on-month and 135% year-on-year to almost 78,000 units in June, Reuters said, citing preliminary estimates published by the China Passenger Car Association (CPCA).

In May, the EV giant sold 32,165 vehicles made in China.

Earlier this week, the company reported its second-quarter production and delivery figures. Tesla manufactured a record 258,580 vehicles during the quarter, beating the consensus estimate of 247,382 vehicles.

However, its deliveries missed expectations and stood at 254,695 vehicles. The figure was also lower than the first-quarter deliveries of 310,048 vehicles. The quarter-over-quarter decline was the result of production suspension at Tesla’s Shanghai plant for 22 days, due to the COVID-19 lockdown.

The factory, which was closed towards the end of March, reopened on April 19 and resumed exports on May 11. However, it failed to reach pre-pandemic production levels, which impacted the company’s second-quarter deliveries significantly.

Tesla eventually aims to manufacture 22,000 cars per week at the plant. In order to reach this target, the company is upgrading the plant.

Wall Street Weighs In

Following the release of the second-quarter production and delivery numbers, Deutsche Bank analyst Emmanuel Rosner maintained a Buy rating on Tesla with a price target of $1,125 (61.8% upside potential).

The analyst has raised his guidance for the second quarter of 2022. He now expects the company’s revenue to total $16.1 billion, up from $15.5 billion projected earlier. The gross margin is expected to come in at 26.8%, up 80 basis points from the previous guidance. Finally, the EPS estimate has been raised to $1.87 from the $1.66 anticipated earlier.

Additionally, John Murphy of Bank of America Securities reiterated a Hold rating on the stock with a $925 price target (33.1% upside potential).

Murphy said, “While Tesla is a trailblazer in the EV market, the competitive environment is heating up and it remains unclear whether the company will be dominant over the longer term.”

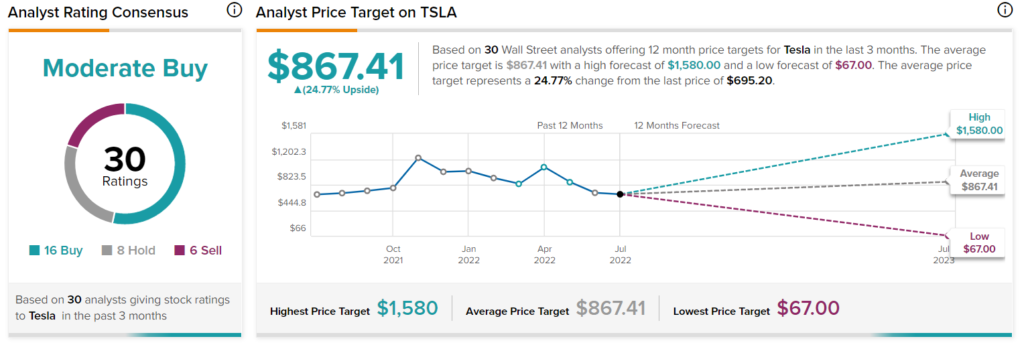

Overall, the stock has a Moderate Buy consensus rating based on 16 Buys, eight Holds and six Sells. Tesla’s average price forecast of $867.41 implies 24.8% upside potential from current levels.

All Eyes Are Now on Tesla’s Second-Quarter Results

Even though Tesla delivered lower-than-expected vehicles during the second quarter, investors have not lost hope. They are waiting for the company’s second-quarter results, which are scheduled to be announced on July 20.

However, analysts are concerned about how fast will the EV maker be able to ramp up production to make up for the lost time. They believe that Tesla needs to make it big in the second half of the year to meet its annual vehicle deliveries growth target of 50%.

Read full Disclosure